Understanding the IRS Statute of Limitations on Tax Debt

What is the IRS Statute of Limitations (CSED)?

Actions That Pause the CSED Clock

Understanding these events is vital for anyone dealing with tax debt.| Action | Impact on Tax Debt |

| Filing an Offer in Compromise (OIC) | The clock is suspended while the offer is pending with the IRS. |

| Requesting a Collection Due Process (CDP) hearing | The clock is suspended during the entire appeal process. |

| Filing for Bankruptcy | The clock is suspended for the duration of the bankruptcy case, plus an additional six months after it ends. |

| Leaving the country for at least six months | The clock is suspended for the period you are outside the U.S. |

| IRS initiating an installment agreement | The clock is suspended while the agreement is being reviewed and set up. |

The 10-Year Rule: When Does the Clock Start and Stop?

The 10-year Collection Statute Expiration Date (CSED) is a critical concept, but its calculation isn't always straightforward. The clock doesn't start on the date you filed your tax return for a given tax year. Instead, the 10-year period for collection begins on the date the IRS assesses the tax liability. This assessment date is the official recording of your tax debt and is what the IRS uses to begin its countdown. Each tax assessment has its own CSED, which means if you have multiple years of back taxes, each one will have a different expiration date. For example, if you filed your 2024 tax return in April 2025 and owed the IRS, the assessment date is usually soon after you file. The 10-year clock would begin ticking from that specific date in 2025. You can find this date on your official IRS transcript, which can be obtained by contacting the IRS or a tax professional. However, the clock can stop. This is known as tolling, and it's a crucial detail for anyone managing tax debt. Tolling events pause the 10-year countdown, extending the time the IRS has to collect. Common tolling events include- Filing for Bankruptcy: The clock stops for the duration of the bankruptcy case, plus an additional six months after it concludes.

- Submitting an Offer in Compromise (OIC): The countdown is suspended while the IRS reviews your offer, and for an additional 30 days after a rejection, plus any time you spend in the appeals process.

- Requesting a Collection Due Process (CDP) hearing: This action, typically used to appeal a tax lien or levy, pauses the clock until the hearing and any related appeals are resolved.

Why Understanding the Statute of Limitations is Critical for You?

For many, especially within the South Asian community, financial matters are handled with a deep sense of personal responsibility and a strong desire for a discreet resolution. Learning about the IRS Statute of Limitations is not just about knowing a legal rule; it’s about giving yourself the power to take control of your financial situation. This knowledge empowers you to understand your fundamental rights as a taxpayer and evaluate your potential options. Instead of feeling helpless or fearful, you can make informed decisions based on accurate information. Knowing the ins and outs of the CSED allows you to engage with the IRS from a position of strength, not confusion, ultimately helping you achieve the peace of mind and financial freedom you seek for yourself and your family.What Happens When the Statute of Limitations Expires?

When the IRS's Collection Statute Expiration Date (CSED) finally arrives and the 10-year period runs out without any "tolling" events, the outcome is clear: the IRS can no longer legally collect the tax debt. Any remaining balance is considered uncollectible and is essentially written off. The IRS can no longer pursue enforced collection actions like wage garnishments, bank levies, or seizing property. However, it's crucial to understand this is a rare occurrence. The IRS actively works to collect debts before the CSED, and many common taxpayer actions—such as filing for an Offer in Compromise or bankruptcy—will pause the clock. Therefore, relying on the CSED to expire is not a reliable strategy. It is far more responsible and effective to proactively explore all available debt relief options with a qualified professional.Beyond the 10-Year Rule: Other Debt Relief Options

While the Statute of Limitations provides a technical deadline, it's not a practical solution for most people. A more proactive and effective approach involves exploring the various legitimate tax relief programs offered by the IRS. A successful financial strategy is holistic, taking into account all available options to find the one that best fits your unique circumstances. Three of the most common and powerful options include:- Offer in Compromise (OIC): This program allows you to settle your tax debt for a lower amount than what you originally owed. The IRS will consider your ability to pay, taking into account your income, expenses, and asset equity. An OIC is typically for individuals experiencing significant financial hardship where paying the full amount would be impossible. The application is complex and requires extensive documentation, so it's a step-by-step process that demands accuracy.

- Installment Agreement: If you can't pay your tax bill in a single lump sum, an installment agreement lets you make monthly payments over a period of up to 72 months. This is a straightforward and accessible option that provides a structured way to pay off your debt. While interest and penalties continue to accrue, this plan prevents the IRS from taking more aggressive collection actions like a bank levy or wage garnishment.

- Currently Not Collectible (CNC) Status: If you're facing severe financial hardship and can prove you're unable to meet your basic living expenses while paying your tax debt, the IRS may temporarily place your account in CNC status. This stops all collection efforts, providing you with a much-needed period of breathing room. The status is not permanent, and the IRS will review your financial situation periodically.

You can learn more about how to settle your debt with the IRS on your own by watching this video:

Your Path to Financial Peace

Navigating tax debt is a significant challenge, but understanding the IRS Statute of Limitations is a powerful tool on your path to a solution. While the 10-year rule offers a deadline for the IRS, it's not a reliable solution in itself due to various "tolling" events. The most effective way to address your tax burden is through proactive and proven strategies like an Offer in Compromise, an Installment Agreement, or exploring Currently Not Collectible status. Remember, you don't have to face this alone. Taking the first step towards a secure future is the most important one. By seeking a professional consultation, you can gain clarity, explore your best options, and move closer to achieving true financial freedom.Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Related Articles

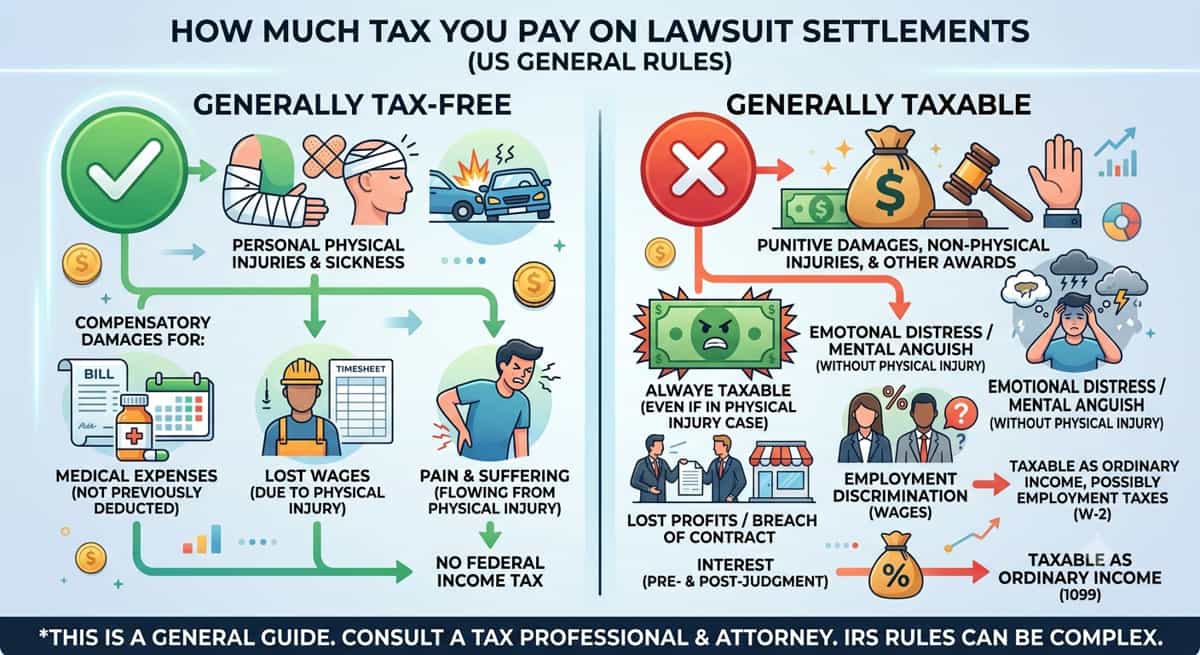

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read