Gross Or Net Income: What Is The Difference?

Moving to the United States offers incredible professional opportunities, yet it often comes with a steep learning curve—especially when navigating the complex world of American personal finance. For many South Asians in the US, this challenge is compounded by the responsibility of managing financial obligations here while also supporting family and remitting funds back home. You are juggling US rent, student loans, or credit card bills alongside the commitment to your loved ones overseas.

In this high-stakes financial environment, the single most critical distinction you must master is the difference between Gross Income and Net Income.

It may seem like a simple concept, but misunderstanding these two figures is the source of many financial struggles—including high debt, insufficient savings, and budgeting errors. When you accept a job offer, the impressive salary number you see is almost always your Gross Income. However, the money that actually hits your bank account—your Net Income—can be significantly less.

This gap, filled by taxes, healthcare premiums, and retirement contributions, is the crucial factor that determines your actual ability to pay bills, manage debt, and save for the future. Relying on your Gross Income for budgeting is a recipe for overspending and financial stress.

The clear goal of this guide is to put you firmly in control: By gaining a precise, expert understanding of how your US paychecks are calculated, you establish the absolute foundation for effective financial management and debt relief. Knowing your true take-home pay is not just a detail; it is your first and most powerful step toward achieving lasting financial freedom in America.

Decoding Gross Income: Your Total Earnings Before the Cuts

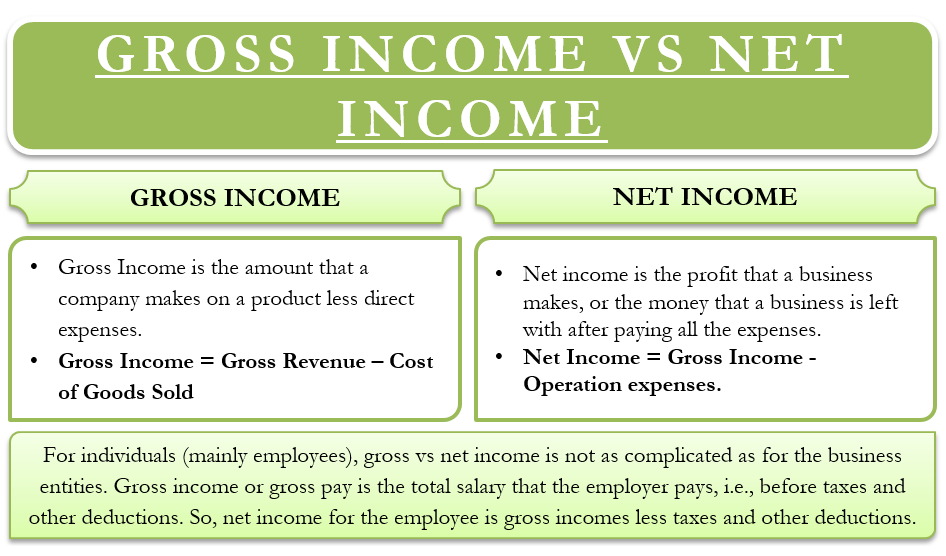

In the United States financial landscape, Gross Income is the starting point for all calculations. Simply put, it is the total amount of money you earn from all sources before any taxes, deductions, or withholdings are taken out. Think of it as the maximum number you could possibly take home if the government and other entities didn't require their share.

This figure is the big, exciting number you see on your initial job offer letter—the annual salary, the hourly rate multiplied by the expected working hours, or the total revenue generated by your business. For those working for an employer, this is the figure reported in Box 1 of your W-2 Form at the end of the year.

Sources of Gross Income

Gross Income is comprehensive and includes virtually all forms of payment you receive. It is important to know that it is not limited to just your primary job's wages. It typically includes:

Wages and Salaries: This is the most common form, calculated annually, monthly, or hourly.

Bonuses and Commissions: Any extra payments received for performance or sales.

Self-Employment/Contractor Income (1099 Income): The total revenue generated before business expenses or self-employment taxes are paid.

Investment Earnings: Dividends, interest, and capital gains from selling assets.

Rental Income: The total rent received before accounting for mortgage, property taxes, or maintenance costs.

Whether you are paid a fixed salary or paid an hourly wage, your Gross Income is the total earning before deductions.

Understanding your Gross Income is crucial because it is the baseline figure used by the Internal Revenue Service (IRS) to determine your overall tax liability. It is the number that defines your income tier and, therefore, what percentage of your earnings is owed to federal and state governments.

For many South Asian professionals navigating the US system, it's particularly important to note the difference between W-2 Gross Income and 1099 Gross Income. If you are a contractor (receiving a 1099 Form), your Gross Income does not have any mandatory taxes pre-withheld, meaning a much larger financial responsibility awaits you at tax time—a factor that can drastically impact your financial planning and debt capacity.

Gross Income and Loan Qualification: What Lenders See

When you apply for a major line of credit, such as a home mortgage, a car loan, or certain large personal loans, lenders almost always ask for documentation of your Gross Income. They use this figure to calculate your Debt-to-Income (DTI) ratio, a key metric for determining how much risk they are taking on. A high Gross Income suggests you have a greater capacity to service the debt.

While a high Gross Income can certainly help you qualify for a larger loan, this reliance can be extremely misleading for your actual repayment capacity. Lenders are looking at a hypothetical number, not the actual cash flow in your bank account. If your deductions for taxes, healthcare, and 401(k) contributions are high, the loan amount you are approved for based on your Gross Income may be completely unaffordable when measured against your true take-home pay (Net Income). This discrepancy is a leading cause of financial stress and debt issues.

What is Net Income? Understanding Your "Take-Home" Pay

If you've ever looked at your salary offer versus the money that actually lands in your bank account, you know there’s a significant difference. The advertised figure is your Gross Income, which represents your total earnings before any adjustments. The amount you actually receive is your Net Income, often called your "take-home pay."

Understanding the process of how your gross income is reduced to your net income is crucial for accurate personal financial planning, budgeting, and tax preparation. Simply put, Net Income is the remaining amount of an individual’s earnings after all mandatory and voluntary deductions have been subtracted from their Gross Income.

The calculation of an individual's net income can be summarized by the following formula:

{Net Income} = {Gross Income} - {Total Deductions}

These deductions fall into two primary categories: mandatory withholdings required by law, and voluntary deductions chosen by the employee for benefits or savings.

Essential Deductions: A Closer Look at the US Payroll System

The United States employs a rigorous payroll system designed to fund public services and social welfare programs through various mandatory withholdings. These are the amounts an employer is legally required to deduct from your paycheck and remit to the appropriate government agencies.

Mandatory Deductions

Federal Income Tax: This is a progressive tax withheld based on your total wages and the information you provide on your IRS Form W-4. The amount deducted anticipates your annual federal tax liability.

State and Local Income Tax: Similar to the federal tax, many states and some local jurisdictions (cities or counties) require income tax withholding. This varies significantly; some states have a flat tax, while others have a progressive system, and a few have no state income tax at all.

Federal Insurance Contributions Act (FICA) Taxes: These funds support the nation's key social safety net programs and are split into two components:

Social Security Tax: Also known as Old-Age, Survivors, and Disability Insurance (OASDI), this is a tax of 6.2% on your wages, up to an annual wage limit set by the IRS (this limit changes each year).

Medicare Tax: This is a tax of 1.45% on all your wages, with no limit. High-income earners may be subject to an Additional Medicare Tax (0.9%) on wages above a certain threshold.

Voluntary and Other Deductions

These deductions are typically elected by the employee, although some, like wage garnishments, are involuntary deductions mandated by a court order.

Health and Welfare Premiums: Deductions for employer-sponsored benefits, such as Health, Dental, and Vision insurance. These are often the largest non-tax deductions.

Retirement Contributions: Contributions to employer-sponsored retirement plans, most commonly a 401(k) or 403(b).

Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA) Contributions: These accounts allow you to save money for qualified medical expenses.

Union Dues: Regular membership fees for employees belonging to a labor union.

Wage Garnishments: Court-ordered involuntary deductions to repay a debt, such as delinquent child support, back taxes, or defaulted student loans. These are usually taken from your post-tax earnings.

Pre-Tax vs. Post-Tax Deductions: The Taxable Income Impact

The timing of a deduction is a critical factor that affects your overall tax burden. Deductions are processed in one of two ways:

Deduction Type | Timing | Impact on Taxable Income | Common Examples |

Pre-Tax | Taken before federal, state, and in most cases, FICA taxes are calculated. | Reduces your taxable income, lowering your overall tax liability for the current year. | Traditional 401(k) contributions, Health/Dental/Vision premiums (under a Section 125 Cafeteria Plan), HSA/FSA contributions. |

Post-Tax | Taken after all taxes (Federal, State, and FICA) are calculated and withheld. | Does not reduce your taxable income for the current year. | Roth 401(k) contributions, Union Dues, Wage Garnishments, supplemental life insurance. |

For example, a Traditional 401(k) contribution is pre-tax, reducing the amount of income subject to taxation today. However, you will pay taxes on the money when you withdraw it in retirement. Conversely, a Roth 401(k) contribution is post-tax, meaning you pay taxes on it now, but your qualified withdrawals in retirement are tax-free.

In summary, your net income is the most accurate reflection of the resources you have available for monthly expenses, savings, and discretionary spending. It is the number you should always use as the foundation for your personal budget, recognizing that your gross income is merely the starting point.

The Critical Difference: Why Net Income is Your Debt Management Starting Point

For most individuals, the most exciting number associated with their job is the Gross Income—the large, pre-tax annual salary figure. However, for serious financial planning, budgeting, and, most importantly, debt management, that number is irrelevant. The only figure that truly matters is your Net Income.

The difference between gross and net income is the difference between a theoretical expectation and a tangible reality. Gross income represents a commitment before obligations are met; net income is the usable resource after those non-negotiable obligations (taxes, mandatory insurance, etc.) have been fulfilled. Basing any financial decision—especially a debt repayment plan—on your gross income is a fundamental error that can lead to significant financial strain, over-leveraging, and budgeting failure.

Net Income is the sole accurate measure of your liquid, available cash flow. It dictates your capacity to pay for necessities, service existing debts, save for the future, and, for many, support family overseas. It is the reliable baseline from which all sustainable financial strategies must be built. Attempting to allocate funds for debt repayment or discretionary spending out of gross income is equivalent to spending money that has already been legally earmarked for the government or mandatory benefits.

Using your net income ensures that your debt repayment plan is sustainable and realistic. When you budget based on net income, you guarantee that essential living expenses and required financial contributions (like taxes and health premiums) are covered first, preventing a shortfall that could force you to borrow money or rely on credit cards, thus exacerbating the debt cycle.

Budgeting with Remittance: Balancing US Expenses and Family Support in South Asia

A significant challenge for many individuals working in the US, particularly those supporting family in South Asia, is balancing domestic American expenses with substantial international financial support, or remittance. For this demographic, your Net Income takes on an even more critical role: it becomes the Total Available Pool for both US living costs and overseas support.

To effectively manage debt while maintaining family remittance, a structured budgeting method is essential, with Net Income as the starting point:

Determine Your True Net Income: Start with your official take-home pay after all mandatory and pre-tax deductions are withheld.

Cover US Fixed Expenses: Allocate funds for non-negotiable, recurring costs in the US. These must be paid first and include rent/mortgage, minimum debt payments (credit cards, loans), insurance, and utilities.

Allocate Remittance Funds: After the US fixed expenses are covered, the next priority is the predetermined amount for family support. This must be treated as a fixed, non-negotiable expense in your budget, just like rent. This approach prevents US discretionary spending from encroaching on funds meant for family.

Manage US Discretionary Spending: The remaining balance after US fixed costs and remittance is your budget for variable and discretionary spending in the US (groceries, transportation, entertainment, savings contributions).

By adhering to this hierarchy, you use your Net Income to establish financial boundaries, ensuring that your vital family commitment (remittance) is secure before you allocate funds to non-essential expenses in the US. This prevents financial stress and ensures consistency in your support while maintaining stability in the US.

Calculating Your Real Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio is a crucial metric used by lenders to assess your borrowing risk. It measures the percentage of your monthly income that goes toward servicing debt payments. The standard DTI formula used by banks and credit scoring models is:

{Gross DTI Ratio} ={Total Monthly Debt Payments}/{Gross Monthly Income}

While this Gross DTI is the industry standard for loan qualification, relying on it for your personal financial assessment can lead to over-leveraging—taking on too much debt relative to your actual usable income.

Here is why a Net DTI is essential for proactive debt management:

Gross DTI Overstates Capacity: Gross income includes the portion already allocated to taxes and mandatory benefits, which can easily consume 20%–35% of your earnings. The standard Gross DTI of 43% (the maximum often allowed for Qualified Mortgages) severely misrepresents your true capacity for repayment once mandatory deductions are taken out.

Net DTI Reflects Usable Cash Flow: Savvy financial planning requires calculating a Net DTI Ratio. This ratio measures debt payments against the income you actually receive, providing a much more conservative and accurate picture of your ability to service debt after covering essential living costs.

{Net DTI Ratio} ={Total Monthly Debt Payments}}/{{Net Monthly Income}}

For example, if your Gross DTI is 40%, your Net DTI could easily jump to 55% or higher, indicating a much riskier financial position. If your Net DTI exceeds 40%, you may be using too much of your available cash flow for debt, leaving little margin for savings, emergencies, or unexpected costs (like a sudden need to increase remittance). Prioritizing a reduction in your Net DTI is the most effective way to secure a sustainable path to debt relief and financial stability.

Avoiding Common Financial Pitfalls: Income Traps for Immigrants

Navigating the US financial system can be complex, and many immigrants, particularly those focusing on optimizing remittances and managing debt, often fall into preventable income traps. These mistakes frequently stem from a misunderstanding of how the US tax and employment structure affects their true take-home pay (Net Income). Understanding these pitfalls is a crucial first step for anyone looking for advice on how to save tax in the US or manage finances effectively.

Pitfall 1: Confusing 1099 (Contractor) Gross Income with W-2 (Employee) Gross Income

One of the most dangerous traps is for professionals who transition from a standard W-2 employment arrangement to an independent contractor (1099) role, or who take on side gigs.

W-2 Employee: Your employer withholds Federal Income Tax, State Income Tax, Social Security, and Medicare taxes from every paycheck. Your Gross Income is automatically reduced, and your Net Income is relatively predictable.

1099 Contractor: The business that hires you pays you the full gross amount. No taxes are withheld. As a result, your 1099 Gross Income appears significantly higher than your W-2 Gross Income, but you are solely responsible for remitting estimated quarterly taxes to the IRS.

Crucially, 1099 workers must pay the Self-Employment Tax, which covers both the employee and the employer portions of Social Security and Medicare (totaling 15.3% in most cases). Failing to set aside a significant portion (often 25% to 35%) of every 1099 payment for taxes will lead to a massive tax bill and penalties at year-end, wiping out savings and potentially creating severe debt. Always budget for 1099 income using an estimated Net Income after setting aside quarterly taxes.

Pitfall 2: Underestimating State Income Tax Variations

When relocating for a new job or planning to live in a specific area, many people focus solely on the federal tax burden. However, state income tax variations drastically alter your final Net Income.

Tax-Free States: States like Texas, Florida, Washington, and Nevada have no state income tax, resulting in a higher take-home pay compared to a state with an identical Gross Income.

High-Tax States: States like California, New York, and Massachusetts have high progressive state income taxes. A seemingly identical salary offer in New York versus Texas will yield a vastly different Net Income.

It is critical to use state-specific payroll calculators before accepting a job offer and calculating your budget or remittance potential. Focusing only on the salary number without accounting for this regional variation leads to inaccurate budgeting and over-commitment to debt or family support.

Pitfall 3: Failing to Leverage Pre-Tax Savings

Many in the immigrant community, eager to maximize the cash available for remittance, often avoid pre-tax savings like the Traditional 401(k), HSA, or FSA. While this keeps the gross amount higher, it results in a higher overall tax bill.

Contributing to pre-tax accounts immediately reduces your taxable income, providing a powerful, immediate tax saving that often outweighs the short-term benefit of taking the cash now. For anyone searching for remittance rules or US financial system advice, leveraging these pre-tax tools is a legal and effective way to reduce taxes and indirectly increase their disposable income pool for both savings and remittance over the long term.

Simple Tools for Tracking Net Income and Budgeting

The complexity of US deductions necessitates a reliable system for tracking your true Net Income and budgeting. You don't need expensive software; simplicity and consistency are key.

Spreadsheet (Google Sheets/Excel): Create a simple tab called "Net Income Tracker." Enter your monthly net pay, date received, and split it immediately into the three key categories: US Fixed Expenses, Remittance, and US Discretionary Spending.

Free Budgeting Apps: US apps like Mint, Personal Capital (Empower), or YNAB (You Need a Budget) can link directly to your bank account, automatically categorizing expenses based on the Net Income that arrives.

The Envelope Method (Digital or Physical): Once your Net Income is determined, allocate that exact amount into "virtual envelopes" for each expense category (Rent, Debt Payment, Remittance, etc.). Once an envelope is empty, spending in that category must stop.

Case Study Example: A Tech Professional’s Income Transformation

The Problem: Ravi, a software engineer from India working in Seattle (a no-state-income-tax state), was earning a $120,000 W-2 Gross Salary. He used the $10,000 monthly gross figure to budget and committed a fixed $2,500 to family remittance. After federal taxes, FICA, and health insurance, his Net Income was closer to $7,300. His required US expenses (rent, utilities, minimum debt payments) totaled $5,000. He was left with only $2,300 for remittance and discretionary spending. He had committed $2,500, leading to a -$200 monthly deficit, which he covered with credit cards.

The Solution (Net Income Focus): Ravi stopped using his gross salary and started budgeting strictly on his $7,300 Net Income.

He reduced his high-interest US debt payments using the debt avalanche method.

He re-prioritized his budget to allocate $2,000 to remittance (a slight reduction to achieve stability).

He committed $500 monthly to an emergency fund and $4,800 to US fixed costs.

By accepting a slightly lower remittance commitment and prioritizing his true Net Income, Ravi eliminated the deficit, started building an emergency fund, and began steadily reducing his debt—all within a sustainable, realistic framework.

Conclusion: Your Next Step Towards Financial Clarity

The journey to financial security begins with a single, non-negotiable truth: Gross Income is an aspiration; Net Income is your reality.

If you are committed to financial stability—whether your goal is aggressive debt repayment, increasing remittance to family in South Asia, or simply building a healthy savings buffer—you must anchor all your decisions to your actual take-home pay. Ignoring mandatory taxes and deductions by budgeting off your gross salary is the quickest way to create a perpetual cycle of deficits, stress, and debt reliance.

Your Net Income represents the precise measure of your available cash flow. By understanding how pre-tax and post-tax deductions shrink your gross earnings, you gain the power to calculate your accurate Net Debt-to-Income (DTI) ratio and implement a realistic, sustainable budget. This foundation prevents over-leveraging and ensures you meet all essential obligations—both in the US and abroad—before allocating funds to discretionary spending.

Your Net Income calculation is not the end of the process; it is the essential first step.

Your Next Step: Seek Professional Consultation

Applying the difference between gross and net income to a complex situation, especially one involving debt and international remittance, requires expert precision.

To move from knowledge to action, the most powerful step you can take is to seek a professional Credit Counselor or Financial Planner . A qualified professionals can use your newly calculated Net Income to:

Audit Your Cash Flow: Precisely determine where every dollar of your take-home pay is going.

Structure Debt Relief: Recommend the best strategy (e.g., debt consolidation, debt management plan, or settlement) based on your actual repayment capacity.

Optimize Tax Benefits: Ensure you are maximizing all pre-tax deductions to legally increase your Net Income and lower your tax burden.

Do not allow the complexity of the US financial system to keep you from achieving peace of mind. Consult a reputable, certified financial professional today to transform your Net Income into a clear and powerful roadmap out of debt.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation