Credit Card Debt Settlement vs Debt Consolidation: Pros & Cons

Understanding Debt Consolidation

Debt consolidation is a financial strategy designed to simplify your debt repayment process by combining multiple unsecured debts—such as credit card balances, medical bills, and personal loans—into a single, new loan. Instead of juggling several payments to different creditors each month, you make one convenient payment to a single lender. This streamlined approach can make your financial life more manageable and predictable. There are a few primary ways to consolidate your debt, each with its own set of requirements and benefits:- Personal Loan: You take out a new, unsecured loan from a bank or credit union and use the funds to pay off your existing debts. This provides a single, fixed monthly payment over a set term.

- Balance Transfer Credit Card: This option involves moving all your existing credit card balances to a new card, often one that offers a promotional 0% or low-interest introductory period.

- Home Equity Loan or Line of Credit (HELOC): If you own a home, you can borrow against its equity to pay off your debts. This is a secured loan, meaning your home serves as collateral.

- Simplified Payments: You make just one monthly payment instead of several, reducing the complexity of managing your finances.

- Potentially Lower Interest Rates: If you have a good credit score, you may qualify for a new loan with a lower interest rate, which can save you a significant amount of money over the long term.

- Fixed Repayment Schedule: A consolidation loan typically has a fixed term (e.g., 3-5 years), providing a clear and predictable timeline for becoming debt-free.

- Credit Score Dependency: Qualifying for the most favorable terms often requires a good to excellent credit score. If your credit is poor, you may not be approved or could be offered a high interest rate.

- Risk of Further Debt: If you consolidate your debt and then continue to use your old credit cards, you could end up with even more debt than before.

- Secured Loan Risk: While home equity loans can offer low interest rates, they are secured by your home. Failing to make payments on time could put your property at risk of foreclosure.

Understanding Debt Settlement

In contrast to consolidation, debt settlement is a more aggressive strategy aimed at reducing the total amount of unsecured debt you owe. It is a process in which a professional debt relief company, acting on your behalf, negotiates with your creditors to accept a lump sum payment that is less than the full amount you originally owed. This method is often considered when a person's debt has become so unmanageable that they have very limited ability to make even minimum payments. The process typically works as follows:- Cease Payments to Creditors: You stop making direct payments to your credit card companies and other creditors. This causes the accounts to go into default, signaling to creditors that you are in financial distress and making them more willing to negotiate.

- Build a Settlement Fund: Instead of paying creditors, you make regular monthly payments into a dedicated, third-party savings account. This fund is managed by the debt relief company and will be used to pay off the settled debts.

- Negotiation: The debt settlement company's negotiators contact your creditors to bargain for a lower payoff amount. The goal is to settle the debt for a fraction of what is owed, often between 40% and 60% of the original balance.

- Final Payment: Once a settlement agreement is reached, the funds from your savings account are used to pay the creditor, and the debt is considered resolved.

- Significant Debt Reduction: The primary advantage is the potential to resolve your debt for a fraction of the original amount, providing substantial financial relief.

- Avoids Bankruptcy: For many, debt settlement offers a viable alternative to filing for bankruptcy, which can have an even more severe and long-lasting impact on your credit.

- Solution for High Debt: It is a strong option for those with overwhelming unsecured debt who are unable to keep up with minimum payments.

- Negative Credit Impact: The process involves intentionally defaulting on your payments, which will severely damage your credit score for a prolonged period, typically seven years.

- Creditor Actions: While the process is ongoing, you may receive frequent and aggressive collection calls from creditors. In some cases, creditors may even file lawsuits against you.

- Potential Tax Liability: The amount of debt that is forgiven (the difference between what you owed and what you paid) may be considered taxable income by the IRS.

- Service Fees: Debt settlement companies charge fees for their services, which are typically a percentage of the enrolled debt.

Which Is Right for You? Making an Informed Decision

Choosing between debt consolidation and debt settlement is not a matter of which option is inherently "better," but rather which one is the most appropriate for your unique financial situation. As a professional, I can tell you that the right path hinges on several key factors, most importantly your credit health, the amount of debt you carry, and your ability to make consistent payments. Choose Debt Consolidation If:- You have a good to excellent credit score. This is crucial for qualifying for a low-interest loan or a 0% APR balance transfer card.

- Your debt is manageable. You can comfortably afford a single monthly payment that covers your principal and interest, and you are confident you can maintain this payment schedule.

- You prioritize your credit score. You want a solution that helps you get out of debt without causing significant, long-term damage to your credit profile.

- Your debt is overwhelming. You are struggling to make minimum payments on your unsecured debts and feel like you have no other options.

- Your credit score is already suffering. Since debt settlement will negatively impact your credit, it may be a suitable choice if your score is already low.

- You need a path to avoid bankruptcy. Debt settlement can be a last resort for individuals who are facing extreme financial hardship but want to avoid the legal and financial consequences of filing for bankruptcy.

Taking Your Next Step Forward

In summary, debt consolidation is a strategic method for simplifying and potentially lowering the cost of your debt by combining it into a single loan, best suited for those with good credit. Debt settlement, on the other hand, is a more aggressive approach to reducing the total amount owed, making it a viable option for those facing overwhelming debt and a poor credit situation. Navigating the complexities of debt is a difficult journey, but it's one you don't have to face alone. The most important step you can take today is to move from confusion to clarity. To get a comprehensive understanding of your personal financial situation and to explore a tailored debt relief plan that aligns with your specific needs, contact a professional financial expert for a free, no-obligation consultation today.Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Related Articles

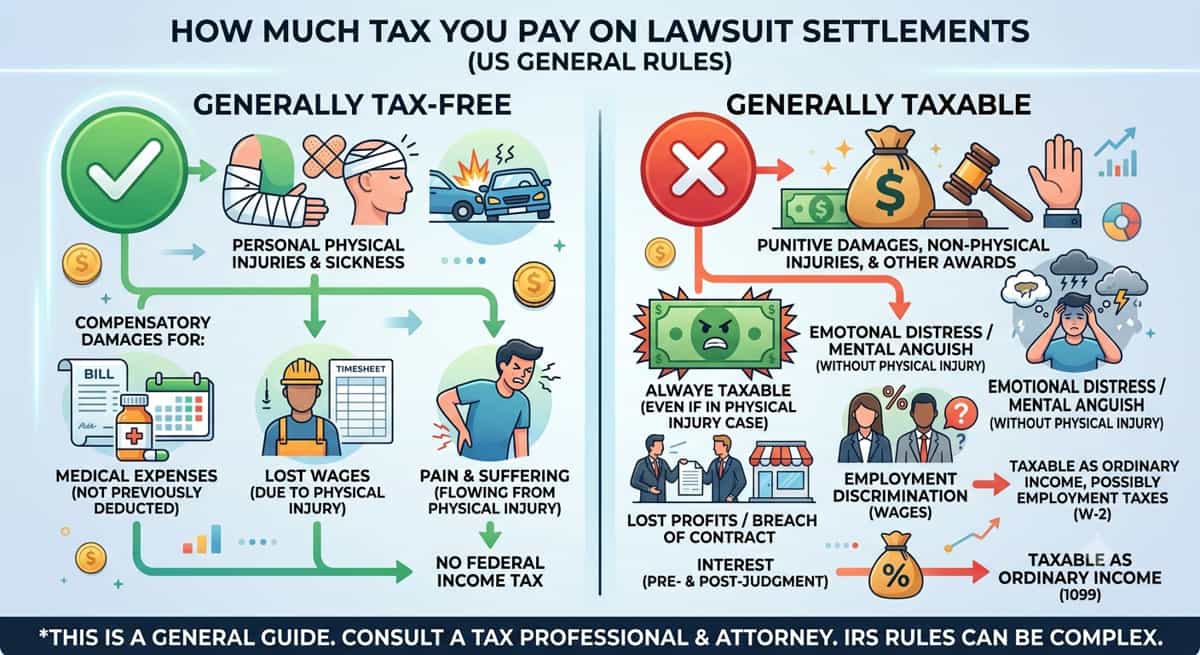

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read