What Is The IRS Fresh Start Program? What You Need To Know

Falling behind on your taxes can happen faster than you think. Maybe a contract job didn’t withhold enough, or an unexpected family emergency back home drained your savings. When the Internal Revenue Service (IRS) starts sending letters, it feels incredibly overwhelming.

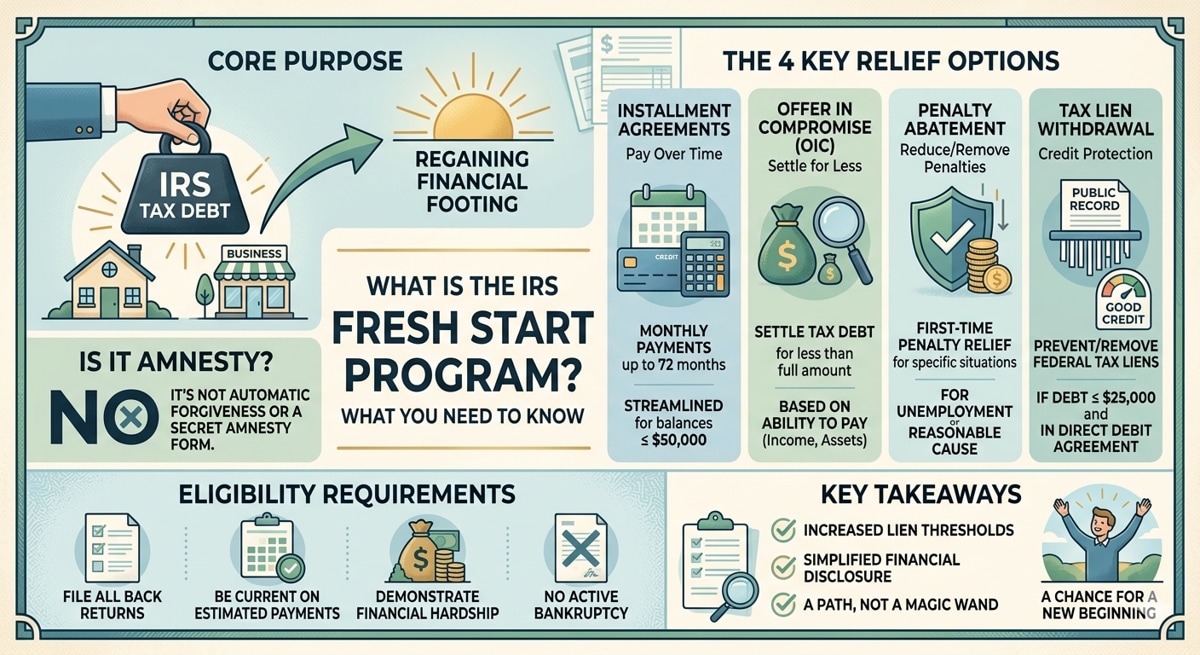

The IRS Fresh Start Program is a tax relief initiative designed by the Internal Revenue Service to help individuals catch up on back taxes without facing extreme financial ruin. Think of it as a bridge back to total tax compliance. Instead of immediately hit you with aggressive collection actions like placing a lien on your property or a levy on your bank account the IRS uses this program to give you a flexible, realistic way to clear your debt. It’s an official safety net meant to break down massive tax burdens into manageable, structured options so you can breathe easier and protect your hard-earned assets.

What Is the IRS Fresh Start Program?

The IRS Fresh Start Program is a set of relief options launched in 2011 that allows qualifying taxpayers to resolve tax debt in more manageable ways including lower thresholds for tax lien filings, longer payment plans, and easier access to debt settlement through the Offer in Compromise.

The IRS didn't create this program out of generosity alone. After the 2008 financial crisis, millions of Americans fell behind on taxes through no fault of their own. The IRS recognized that aggressive enforcement on people who genuinely couldn't pay wasn't working for taxpayers or for the government. Fresh Start was the response.

One important thing to understand: Fresh Start is not one single program with one application. It's an umbrella of expanded policies that work together. Depending on your situation, you might use one component, or a combination of several.

And for anyone in the South Asian community who grew up hearing that you never deal with the government unless you absolutely have to, this is an official IRS program. It's not a loophole, not a scam, and not something that puts you at risk. It was designed specifically to help people get back on track.

What Does the IRS Fresh Start Program Actually Cover?

Fresh Start expanded four major areas of IRS relief. Here's what each one means in plain terms.

1. Tax Lien Withdrawal

A federal tax lien is the government's legal claim against your property when you owe unpaid taxes. It shows up on your credit report, can block you from selling your home, and can make it nearly impossible to get a business loan.

Before Fresh Start, the IRS could file a tax lien once you owed as little as $5,000. Fresh Start raised that threshold to $10,000, which kept a significant number of taxpayers off the lien list entirely.

Even better: if you already have a tax lien and you enter into a Direct Debit Installment Agreement where payments are automatically pulled from your bank account the IRS will now consider withdrawing that lien. That can mean real relief for your credit and your financial reputation.

2. Installment Agreements (Payment Plans)

Before Fresh Start, if you owed more than $25,000, getting a payment plan required a full financial review disclosing assets, income, expenses, everything. That process was intimidating and time-consuming.

Fresh Start changed that. Now, if you owe $50,000 or less, you can set up a streamlined installment agreement online without a detailed financial disclosure. You get up to 72 months six years to pay it off.

3. Offer in Compromise (OIC)

An Offer in Compromise lets you settle your tax debt for less than the full amount owed but only if paying the full amount would create a genuine financial hardship.

Fresh Start made the OIC process more accessible by relaxing some of the financial calculations the IRS uses to evaluate your ability to pay. The IRS now looks at a shorter window of future income when deciding what you can realistically afford.

That said, an OIC is not a sure thing. The IRS reviews your income, monthly expenses, the value of your assets, and what you're likely to earn going forward. Acceptance rates have historically hovered around 40%, which means preparation matters enormously. More on that shortly.

4. Penalty Abatement

When you fall behind on taxes, the penalties can sometimes grow faster than the actual debt failure-to-file penalties, failure-to-pay penalties, and interest that compounds daily.

Fresh Start made it easier to request penalty removal in two ways: First-Time Penalty Abatement, which removes penalties if you have a clean compliance history for the prior three years; and Reasonable Cause Abatement, which applies when life circumstances a medical emergency, a divorce, a serious family crisis genuinely prevented you from filing or paying on time.

Think of someone like Priya, a software consultant who went from a full-time job to her first 1099 contract and didn't realize she was supposed to make estimated quarterly payments. By year-end, she owed both the original tax and a stack of penalties. Under first-time abatement, those penalties were removed bringing her actual balance down to something manageable.

Who Qualifies for the IRS Fresh Start Program?

To qualify for the IRS Fresh Start Program, you generally need to be current on all required tax filings, not be in active bankruptcy proceedings, and meet the specific income or debt thresholds for whichever component you're applying for.

Here's a quick reference by component:

Fresh Start Component | Basic Eligibility Threshold |

Streamlined Installment Agreement | Owe $50,000 or less; can pay within 72 months |

Offer in Compromise | Demonstrable financial hardship; all returns filed |

Tax Lien Withdrawal | Must enter Direct Debit Installment Agreement |

Penalty Abatement (First-Time) | Clean compliance history for prior 3 years |

Fresh Start is open to W-2 employees, self-employed individuals, gig workers, freelancers, and small business owners. The type of income doesn't disqualify you.

A question that comes up often in South Asian communities: Does my immigration status affect whether I can apply? The short answer is no IRS eligibility is based on your tax liability, not your immigration status. However, because financial records can sometimes intersect with immigration matters in complex ways, it's worth speaking with an advisor if you have specific concerns.

IRS thresholds and program rules do get updated. Always verify current requirements directly at IRS.gov or with a licensed tax professional before you apply.

How to Apply for the IRS Fresh Start Program - Step by Step

The process is more straightforward than most people expect. Here's how to approach it:

File all missing tax returns first. You cannot enter any Fresh Start program if you have unfiled returns. Even if you can't pay yet, file. This is the single most important step.

Get your tax transcript. Log in to IRS and request your tax transcript. This tells you exactly what you owe, which years are affected, and whether you have any existing liens or penalties.

Identify which Fresh Start option fits your situation. Use the table above as a starting guide. If your debt is under $50,000 and you can make monthly payments, a streamlined installment agreement is likely your fastest path. If full repayment would cause real hardship, explore OIC.

Apply through the right channel.

Installment agreements under $50,000: Apply online at IRS.gov through the Online Payment Agreement tool.

Offer in Compromise: Complete and submit IRS Form 656, along with Form 433-A or 433-B .

Consider professional help for complex cases. For straightforward installment agreements, you can handle this yourself. For OIC applications or cases involving multiple years and penalties, a licensed tax professional, an enrolled agent, CPA, or tax attorney is worth the investment.

One thing many people don't realize: once you've submitted an application and it's under review, the IRS generally pauses active collection efforts. So even if you've received levy notices or threatening letters, starting the process changes your situation immediately.

OIC reviews can take six months to a year. Stay patient, respond promptly to any IRS correspondence, and don't miss a single payment if you're already on a plan.

Common Mistakes That Hurt Your Fresh Start Application

Even when people do the right thing by applying, avoidable errors can derail the process entirely.

Not filing all prior-year returns. This is the most common reason applications are rejected before they're even reviewed. Every return must be filed even if you owe money on all of them.

Underreporting income on an OIC application. The IRS cross-references your submission against your filed returns, W-2s, and 1099s. Any inconsistency, even unintentional triggers rejection and can raise questions about your credibility as an applicant.

Missing a payment after your plan is approved. An installment agreement is a legal agreement. Miss a payment without notifying the IRS, and the agreement is automatically voided. That means the full balance becomes due again, and enforcement can resume immediately.

Assuming one application resolves everything. Fresh Start agreements apply to specific tax years and liability types. If you have multiple years of debt or both personal and business liabilities, each may need to be addressed separately.

Waiting too long. The IRS has a 10-year window to collect unpaid taxes. That sounds like a lot of time, but enforcement levies, garnishments, asset seizures typically escalate years before that deadline. Waiting rarely helps.

Here's a scenario that plays out more than you'd think: Nasreen runs a restaurant in Queens with her husband. They apply for an OIC and disclose her income carefully but forget to include her husband's salary from a separate part-time job. The offer is rejected. They have to start over, losing months and the $205 application fee. The lesson is simple: full disclosure, every time.

Is the IRS Fresh Start Program Right for You?

Not everyone needs the same solution, and Fresh Start offers enough flexibility to meet people where they are.

If you owe under $50,000 and can realistically make monthly payments, a streamlined installment agreement is almost always the fastest, easiest path. No lengthy financial review, no face-to-face meetings, just a plan and a commitment to pay.

If paying the full balance would genuinely leave you unable to cover basic living expenses rent, food, utilities, medical care then the Offer in Compromise is worth exploring seriously. It takes more documentation and more time, but settling for less than you owe is a real outcome for people who qualify.

If your balance is mostly penalties and interest rather than actual tax owed, tackle penalty abatement first. Removing those penalties can bring your real balance down significantly before you decide on a payment approach.

Whatever your situation, Fresh Start works best when you approach it honestly, gather the right documents, and follow through. This isn't a program that rewards shortcuts but it genuinely rewards people who show up and do the work.

You Have Options. Use Them.

If there's one thing to take away from this article, it's this: having IRS tax debt doesn't mean you're out of options. It means you're in a situation the IRS has specifically built tools to address.

The Fresh Start Program exists because the IRS learned that pushing people with no real ability to pay into aggressive enforcement didn't solve anything. These relief options are legitimate, they're legal, and they work when used correctly.

In many South Asian families, there's a deep cultural weight around debt, especially debt owed to the government. It can feel like failure, like something to hide. But using an official IRS program isn't a sign of weakness. It's exactly what financial management looks like in a difficult moment. It's knowing your rights and using them.

If you have questions about your specific situation, speaking with a licensed tax professional, an enrolled agent, a CPA, or a tax attorney is always the safest first step. Many offer free initial consultations, and the clarity you'll get in one conversation is worth more than weeks of worry.

Frequently Asked Questions

Does the IRS Fresh Start Program really work?

Yes when applied correctly. The program has helped millions of taxpayers resolve debt through payment plans and settlements. Success depends on meeting eligibility requirements, submitting accurate documentation, and staying compliant after your plan is approved. It's not a magic fix, but it's a real one.

Will the IRS Fresh Start Program hurt my credit?

The program itself doesn't affect your credit score directly. However, any existing tax liens on your record may already be doing damage. Getting a lien withdrawn after entering a payment plan one of Fresh Start's key features can actually help improve your credit profile over time.

Can I apply for the IRS Fresh Start Program on my own?

Yes. For installment agreements under $50,000, the entire process can be completed at IRS.gov in under an hour. For Offer in Compromise cases, or if you have multiple years of debt and penalties, working with a licensed enrolled agent or CPA significantly improves your odds of acceptance.

What if I genuinely can't afford any payment plan?

If your financial situation makes even a minimal payment impossible, the IRS has a separate status called "Currently Not Collectible." While it doesn't eliminate what you owe, it temporarily suspends all collection activity. A tax professional can help you apply. It's worth knowing this option exists.

Is the Fresh Start Program available for small business owners?

Absolutely. Sole proprietors and small business owners are among the most frequent users of Fresh Start provisions. Both installment agreements and the Offer in Compromise are available for business-related tax liabilities, including payroll taxes in some circumstances.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

Tax Evasion Vs Tax Fraud And The Statute Of Limitations

9 min read

What Is An IRS Substitute For Return(SFR)?

12 min read

IRS Currently Not Collectible Status: What Are The Pros And Cons?

12 min read

What Are The Dangers Of Filing Your Own Taxes?

11 min read

Tax Relief And Resolution: 5 Ways To Deal With Tax Debt

11 min read

What Happens If A Form 8300 Is Filed On You?

10 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation