Financial Tips, Guides & Insights Blog

Page 2 of 29

Is Credit Card Debt Forgiveness Possible?

Credit card debt forgiveness is real but rarely wipes balances clean. South Asian immigrants facing financial hardship or remittance pressures can explore internal hardship programs, nonprofit debt management, or settlement. Watch out for predatory upfront-fee scams and potential IRS tax bills on forgiven amounts. Take control by consulting certified counselors today.

Debt Management- The Right Program

Managing credit card debt while supporting family abroad is challenging, but a Debt Management Program (DMP) can help. Offered by nonprofit agencies, DMPs consolidate your unsecured debts into one manageable monthly payment with lower interest rates over 3–5 years. Avoid predatory scams by verifying NFCC accreditation and choosing a structured path toward financial freedom.

How To Protect Your Business And Personal Assets From Debt Collectors

Facing aggressive debt collection can feel crushing for South Asian small business owners, but US civil law protects you regardless of your immigration status. The FDCPA bans collector harassment, while homestead exemptions and ERISA laws legally shield personal assets like homes and retirement funds. Explore debt negotiation or credit counseling to regain control.

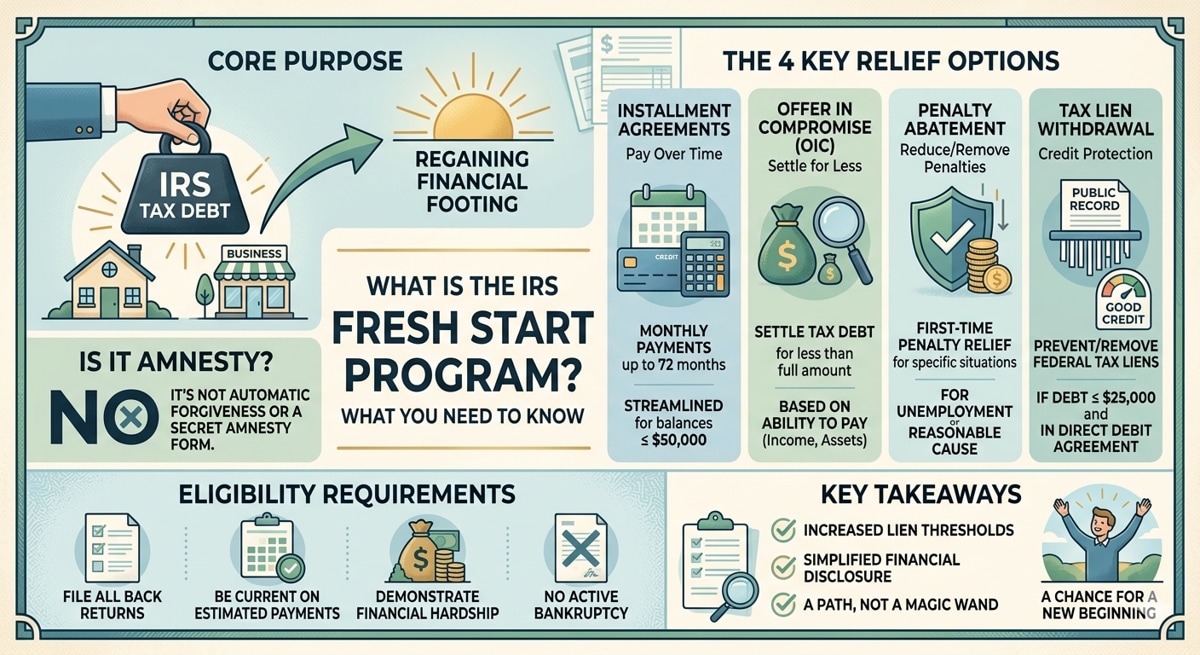

What Is The IRS Fresh Start Program? What You Need To Know

The IRS Fresh Start Program helps taxpayers clear back taxes and avoid aggressive collection actions. It offers streamlined payment plans for debts under $50,000, easier debt settlements, tax lien withdrawals, and penalty relief. To qualify, you must file all missing returns. It is an official safety net for financial recovery.

How To Request A Debt Verification Letter

Receiving a US debt collection notice can be stressful, especially for South Asian immigrants unfamiliar with the financial system. Under the Fair Debt Collection Practices Act (FDCPA), you have the legal right to send a written Debt Verification Letter within 30 days to halt collection activity and force agencies to prove the debt is legitimate before paying.

Does IRS Debt Show On Your Credit Report?

The IRS doesn't report debt to credit bureaus, but ignoring it can trigger a public federal tax lien, freezing home sales, refinancing, and loans. Additionally, sudden bank levies or wage garnishments can cause missed bill payments, indirectly wrecking your credit.

What Is An IRS Partial Payment Plan?

An IRS Partial Payment Installment Agreement (PPIA) offers tax relief by letting you make affordable monthly payments based on your income and living expenses. Once the IRS’s 10-year collection window expires, any remaining debt is permanently discharged. It provides a structured, legally backed path to financial freedom and peace of mind.

Understanding Healthy Business Debt: How Much Is Acceptable?

Strategic debt drives growth when returns exceed interest costs. For South Asian entrepreneurs, monitoring key financial metrics like a Debt-to-Equity ratio under 2:1 and a Debt Service Coverage Ratio above 1.25 is essential. Recognizing early warning signs and leveraging SBA or professional resources protects both your business and family.

Understanding Tax Settlement: The Offer In Compromise

Dealing with tax debt can feel overwhelming and carry a quiet shame. However, the IRS Offer in Compromise (OIC) program allows qualified individuals to settle their debt for less than they owe based on what they can realistically pay. Ensure you are current on filings before applying, and always consult licensed professionals.

Should You Choose Debt Settlement Or Credit Counseling?

Managing debt in the U.S. can feel overwhelming and shameful, but options exist. Debt settlement reduces your balance but severely damages credit and risks tax penalties. Credit counseling creates a structured plan to repay everything at lower interest rates, protecting your score. Assess your hardship, avoid predatory scams, and consult a certified nonprofit counselor.