How To Protect Your Business And Personal Assets From Debt Collectors

You came to the United States with a dream. Maybe you opened a small grocery store, a restaurant, or a trucking company. You worked long hours, supported your family back home, and built something real. Then one day, the phone starts ringing debt collectors. Letters pile up. A notice arrives that a creditor may take legal action against you.

For many South Asian families in the USA whether from India, Pakistan, Bangladesh, Nepal, or Sri Lanka this moment feels crushing. And because debt carries deep shame in our communities, most people stay silent instead of getting help. They don't know their rights. They don't know what collectors can and cannot legally do. And that silence can cost them everything.

The truth is: the US law offers real, powerful protections for both your personal and business assets but only if you know how to use them.

Why South Asians in the USA Are Especially Vulnerable to Aggressive Debt Collection

South Asians are one of the fastest-growing entrepreneurial communities in the United States. According to the U.S. Small Business Administration, South Asian Americans own hundreds of thousands of small businesses across the country from convenience stores and motels to medical practices and tech startups.

But that drive to build also comes with unique financial risks.

Many South Asian families borrow informally from relatives, community members, or religious networks without written agreements. When things go wrong, these arrangements can turn into complicated, emotionally charged debt situations with no legal clarity.

Then there's the business side. A lot of South Asian small business owners personally guarantee their business loans. That means if the business struggles, debt collectors can come after your personal savings, your car, and sometimes even your home.

Language barriers make it worse. If English isn't your first language, understanding a legal notice or knowing your rights when a collector calls can feel impossible. Many people simply don't respond and that silence can lead to a default judgment against them in court, which gives collectors even more power.

And perhaps the biggest fear of all: "Will this affect my visa or green card?"

The short answer is no. Debt collection in the USA is a civil matter, not a criminal one. Owing money to a creditor does not trigger deportation, affect your immigration status, or result in arrest. Debt collectors who threaten otherwise are breaking the law.

But because so many people don't know this, they panic and that panic leads to bad decisions like paying debts they don't legally owe, ignoring court summons, or transferring assets in ways that can actually hurt them later.

Understanding Your Legal Rights Against Debt Collectors (FDCPA Basics)

Most people don't realize this but in the United States, there is a federal law specifically designed to protect you from aggressive or abusive debt collectors. It's called the Fair Debt Collection Practices Act (FDCPA), and it applies to everyone living in the USA, regardless of your immigration status, citizenship, or how long you've been here.

Here's what that law means for you in plain terms.

Debt collectors are legally prohibited from:

Calling you before 8 a.m. or after 9 p.m.

Using threatening, abusive, or offensive language

Lying about who they are or how much you owe

Threatening arrest or jail time over a debt (this is illegal)

Calling your workplace repeatedly if you've asked them to stop

Discussing your debt with your family members, neighbors, or employer

You have the right to:

Request debt validation - Within 30 days of first contact, you can ask the collector to prove in writing that the debt is real, the amount is correct, and they have the legal right to collect it

Send a cease communication letter - Once you send this in writing, the collector must stop contacting you (except to notify you of specific legal actions)

Dispute a debt - If you believe you don't owe it, or the amount is wrong, you can formally dispute it

If a debt collector violates any of these rules, you may be able to sue them and recover damages including up to $1,000 in statutory damages plus attorney fees, according to the FDCPA.

State laws can give you even more protection. If you live in California, New York, New Jersey, or Texas states where large South Asian communities are concentrated — your state may offer additional rights beyond the federal law. For example, California's Rosenthal Fair Debt Collection Practices Act extends FDCPA-style protections to original creditors as well, not just third-party collectors.

For official guidance, the Consumer Financial Protection Bureau (CFPB) at cfpb.gov and the Federal Trade Commission (FTC) at ftc.gov both offer free, plain-language resources on your debt collection rights.

Knowing these rights won't make the debt disappear but it puts you back in control of the situation.

How to Protect Your Personal Assets From Debt Collectors

One of the first questions people ask when debt collectors come calling is: "Can they actually take my home? My savings? My retirement money?"

The honest answer is it depends. But the good news is that US law protects more than most people realize. And if you take the right steps early, you can keep the things that matter most to your family safe.

Assets That Are Typically Exempt From Collection

Not everything you own can be taken by a debt collector. Certain assets are legally "exempt," meaning collectors generally cannot touch them even if a court judgment is made against you.

Here's what is typically protected:

Your primary home - Most states have a homestead exemption that protects some or all of your home's value from creditors. In Texas and Florida, this protection is especially strong. In California, New Jersey, and Illinois - states with large South Asian communities the exemption amounts have increased significantly in recent years, so it's worth checking your current state limits.

Retirement accounts Your 401(k), IRA, and most employer-sponsored retirement funds are federally protected under a law called ERISA. In most cases, creditors simply cannot reach this money.

Social Security and government benefits - These are protected both at the federal level and in most states.

A portion of your wages - There are strict legal limits on how much of your paycheck a creditor can garnish. Federal law caps it at 25% of your disposable income and some states set the limit even lower.

Essential household items - Furniture, clothing, and basic personal property are typically exempt up to a certain dollar value that varies by state.

One important note: these exemption amounts and rules vary from state to state. What's fully protected in Texas may only be partially protected in New York. If you're unsure what applies in your state, speaking with a debt relief professional can give you a clear picture specific to your situation.

Proactive Steps to Legally Shield Your Personal Assets

Knowing what's protected is only half the picture. The other half is making sure you don't accidentally expose yourself to more risk than necessary. These steps can make a real difference:

Separate your personal and business money right now. This is one of the most common mistakes South Asian family businesses make. When you mix personal and business funds in the same account, you make it much easier for creditors to come after both. Open separate bank accounts and keep them completely apart.

If you're married, look into tenancy in its entirety. In many states, property held jointly by a married couple under this arrangement is protected from one spouse's individual creditors. So if only one of you has a debt, that jointly owned home may be shielded. Not all states offer this, but California, New York, New Jersey, and Illinois residents should ask a professional whether it applies to them.

Keep contributing to your retirement accounts. Beyond saving for your future, consistent retirement contributions help keep those protected funds growing and out of reach from most creditors.

Do not transfer assets to a family member or friend to "hide" them. This is one of the most important warnings in this guide. If you suddenly transfer property or money to a relative right before or during a debt lawsuit, a court can reverse that transfer and treat it as fraud. It's called a "fraudulent conveyance" and it can make your legal situation significantly worse.

The earlier you take these steps, the stronger your protection will be. Asset protection works best before a creditor comes after you not after.

How to Protect Your Business Assets From Creditors and Debt Collectors

If you own a business, debt trouble can feel like it's coming from two directions at once creditors can potentially go after your business and your personal life. But with the right structure in place, you can build a legal wall between the two.

Here's what every South Asian small business owner in the USA needs to know.

Choose the Right Business Structure

The way your business is legally set up has a massive impact on how protected you are.

If you're currently running your business as a sole proprietor meaning the business is just in your name with no separate legal structure there is no separation between you and the business. If the business owes money, you owe money. Your personal savings, your car, and your home could all be at risk.

Setting up a Limited Liability Company (LLC) creates a legal boundary between you and your business. If the business faces debt or a lawsuit, creditors generally cannot come after your personal assets, your house, your personal bank account, or your family's savings. The liability stays with the business.

For more established businesses, an S-Corporation can offer similar protections along with potential tax advantages.

However and this is critical if you personally guarantee a business loan, that protection disappears for that specific debt. Many South Asian business owners sign personal guarantees when taking out small business loans or opening business credit lines, often without fully realizing what they're agreeing to. If the business can't pay, the lender can come after you personally.

Before changing your business structure or signing any new agreements, speak with a licensed business attorney. A one-hour consultation can save you from years of financial pain.

Maintain Proper Corporate Formalities

Setting up an LLC or corporation is only the first step. You have to run it like a real separate business because if you don't, a court can decide the legal separation doesn't actually exist. This is called "piercing the corporate veil," and it's more common than you might think.

This happens a lot in family-run South Asian businesses, where the lines between personal and business life are naturally blurred. Here's how to make sure your legal protection holds up:

Keep a dedicated business bank account, never deposit personal money into it or use it for personal purchases

Pay yourself a formal salary or owner's draw rather than just pulling cash from the business account whenever you need it

Maintain basic business records keep track of major business decisions, especially if you have partners or co-owners

File all required annual reports and state fees to keep your LLC or corporation in good standing

Think of it this way: if you want the law to treat your business as separate from you, you have to treat it that way yourself every single day.

Business Insurance as an Asset Protection Tool

Even the best business structure has limits. That's where business insurance comes in and many small business owners, especially those just starting out, either skip it entirely or are underinsured.

The right insurance policies can absorb the financial impact of lawsuits, accidents, and claims before they ever turn into debts that threaten your assets:

General Liability Insurance covers bodily injury, property damage, and basic legal claims against your business the most essential policy for any business owner

Professional Liability Insurance (also called Errors & Omissions) is critical if you provide a service it protects you if a client claims your work caused them financial harm

Business Owner's Policy (BOP) bundles general liability and property insurance together, typically at a lower cost a smart, affordable option for small businesses

Think of business insurance as the first line of defense. It handles problems before they become debts. And debts that never happen are the ones that can never threaten your home or savings.

Debt Relief Options Available to South Asians in the USA

Protecting your assets is one side of the equation. But if the debt itself is becoming unmanageable, protection alone isn't enough. You need a path forward. The good news is that there are real, legal options available to you, no matter how overwhelming things feel right now.

Here are the three most common routes people take and what each one actually means for your life.

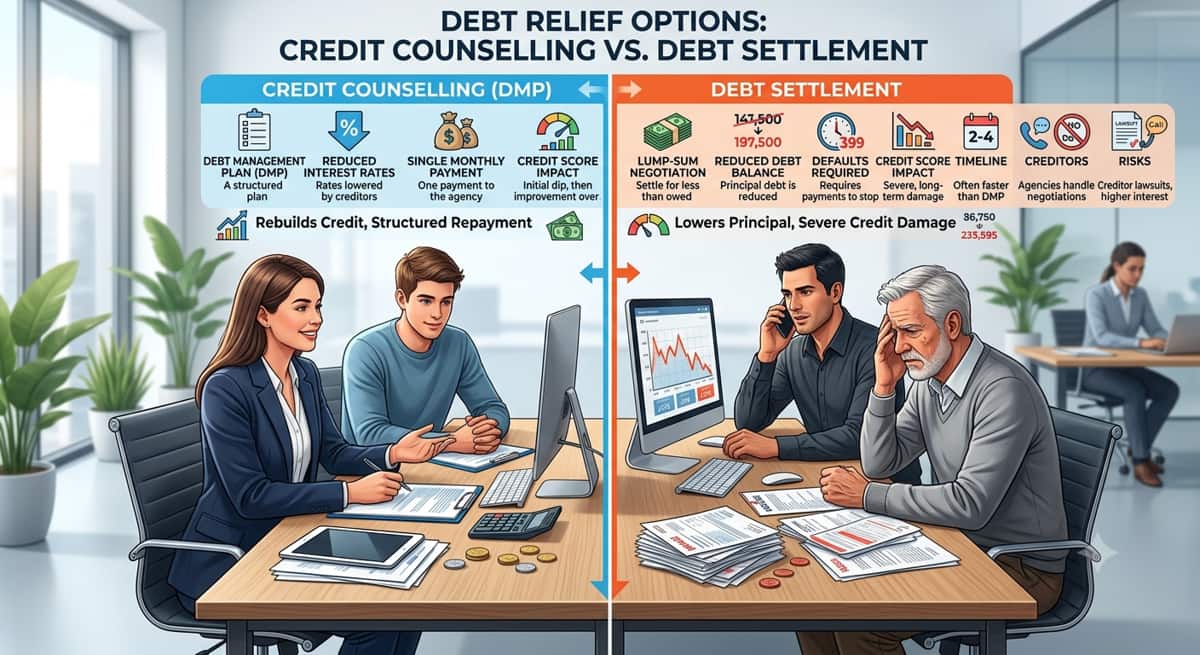

Debt Negotiation and Settlement

Debt settlement is when you or a professional working on your behalf negotiates directly with creditors to accept a lump-sum payment that is less than the full amount you owe. In many cases, creditors agree to settle for 40% to 60% of the original balance, especially when the account has been delinquent for a while. From the creditor's perspective, getting something is better than getting nothing.

This can be a real lifeline if you're drowning in credit card debt, medical bills, or personal loans.

But go in with clear eyes. Debt settlement will affect your credit score typically for several years. It also has tax implications: the IRS may consider the forgiven portion of your debt as taxable income, so you'll want to plan for that.

Most importantly, work only with a licensed, accredited debt relief company. Look for membership in the American Fair Credit Council (AFCC) or accreditation through the International Association of Professional Debt Arbitrators (IAPDA). There are unfortunately many scam operations that prey on immigrant communities — we'll cover those warning signs later in this guide.

Bankruptcy as a Last Resort

In many South Asian households, the word "bankruptcy" feels like the ultimate shame, a sign of failure, something that would dishonor the family. But here's the reality: bankruptcy is a legal tool built into the US system specifically to give people a fresh start. It is not a moral judgment. It is not a crime. And filing for bankruptcy does not affect your immigration status or your path to citizenship.

There are two main types most individuals and small business owners use:

Chapter 7 Bankruptcy wipes out most unsecured debts: credit cards, medical bills, personal loans relatively quickly, usually within 3 to 6 months. You may have to give up certain non-exempt assets, but as we covered earlier, many of your most important assets are protected by exemptions. To qualify, your income must fall below a certain threshold.

Chapter 13 Bankruptcy works differently. Instead of wiping out debt immediately, you enter a 3 to 5 year repayment plan that restructures what you owe into manageable monthly payments. You get to keep your assets while catching up on mortgage arrears, car payments, and other secured debts. This is often the better option for business owners or homeowners who have regular income but need breathing room.

One of the most powerful things about filing for bankruptcy regardless of which chapter is something called the automatic stay. The moment you file, all collection calls stop. All lawsuits pause. All wage garnishments halt. Immediately. It gives you legal breathing room to figure out your next steps without the constant pressure.

If you're seriously considering bankruptcy, speak with a bankruptcy attorney before making any decisions. Many offer free initial consultations, and the right guidance at this stage can make a significant difference in your outcome.

Credit Counseling and Debt Management Plans

If your debt situation is serious but bankruptcy feels like too drastic a step, credit counseling may be the right middle ground and it's an option that doesn't get talked about nearly enough in South Asian communities.

A nonprofit credit counseling agency can review your full financial picture, help you understand your options, and create a realistic plan to get back on track. Many offer services in multiple languages, which can make a meaningful difference if English is not your first language.

One of the most useful tools these agencies offer is a Debt Management Plan (DMP). Here's how it works: the agency negotiates with your creditors to reduce your interest rates and consolidate all your monthly payments into a single, lower payment. You pay the agency once a month, and they distribute it to your creditors. Most DMPs are completed within 3 to 5 years.

A DMP won't reduce the total principal you owe the way settlement does, but it is far less damaging to your credit score and doesn't carry the same legal weight as bankruptcy. For many people especially those with steady income who simply got buried under high interest rates it's the most practical and dignified path forward.

Warning Signs: Debt Collection Scams Targeting Immigrant Communities

Here is something that doesn't get talked about enough: not every person calling you about a debt is a real, legitimate debt collector.

There is a whole industry of scammers who specifically target immigrant communities including South Asians because they know that fear, language barriers, and unfamiliarity with the US legal system can make people more easily pressured into paying money they don't actually owe.

The Most Common Debt Collection Scams to Watch Out For

Phantom debt calls are exactly what they sound like someone calls claiming you owe a debt that simply doesn't exist. They may have some of your personal information, which makes them sound convincing. But the debt is completely fabricated. Remember: you always have the right to ask for written proof of any debt before you pay a single dollar.

Immigration threats are one of the most cruel and effective tactics used against immigrant communities. A caller tells you that if you don't pay immediately, they will report you to immigration authorities, get your visa cancelled, or have you deported. This is completely illegal. No legitimate debt collector has the power to do any of these things. Debt collection is a civil matter it has absolutely no connection to your immigration status. Any collector who says otherwise is breaking federal law and almost certainly running a scam.

Unusual payment demands are a major red flag. If someone pressures you to pay via wire transfer, gift cards, cryptocurrency, or any payment method that can't be traced or reversed — stop the conversation immediately. Real debt collectors accept standard payment methods and provide written documentation. Scammers demand untraceable payments because once the money is gone, it's gone.

Government impersonation is another tactic where callers claim to be from the IRS, Social Security Administration, a court, or even immigration authorities like USCIS. They create panic and urgency to get you to act before you think. Real government agencies almost never make first contact by phone they send official written notices first.

A Note for Our Community

Scammers specifically look for people who may not speak fluent English, who are unfamiliar with US legal processes, or who are afraid to ask questions. If you receive a call that feels threatening or confusing, don't face it alone. Ask a family member, a trusted friend, or a community member to help you understand what's being said and whether it's legitimate.

You are not required to handle these situations by yourself and getting a second opinion before paying anything is always the right move.

How to Report a Debt Collection Scam

If you believe you've been targeted by a scam or that a debt collector has violated your rights, you can report it to:

Consumer Financial Protection Bureau (CFPB)

Federal Trade Commission (FTC)

Your state's Attorney General office most have a consumer protection division that handles these complaints

Reporting these scams doesn't just protect you, it helps protect other members of your community who may be targeted next.

Take Control of Your Financial Future

Dealing with debt collectors is stressful, frightening, and in our communities often deeply isolating. But if there is one thing we hope you take away from this guide, it's this: you are not powerless, and you are not alone.

The US legal system gives you real rights. Your home, your retirement savings, and your family's security are not automatically up for grabs just because a debt collector is calling. You have tools available legal protections, debt relief options, and professionals who can stand in your corner.

And here's something worth saying clearly: seeking help is not weakness. It is not shameful. It is not a failure.

In our culture, we carry financial stress in silence because we don't want to worry the family or bring dishonor. But protecting your family's future by taking action before things get worse is one of the most responsible and courageous things you can do as a parent, a spouse, a business owner, or a provider.

The next step is simple: speak with a licensed debt relief professional who understands your situation.

Whether you need help negotiating with creditors, understanding your bankruptcy options, or simply figuring out where to start a free consultation costs you nothing and could change everything.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read