How Interest Rates Affect Debt

Interest rate is the price you pay for borrowing money. It's typically expressed as a percentage, indicating how much you pay back in addition to what you originally borrowed. It means your debt is costing you more each month and it can take longer to pay off, even if you're making payments every month.

But if you're new to US credit you just moved here a few years ago, or maybe you are the first in your family to get approved for a credit card, auto loan, or student loan this can feel confusing. But at home borrowing probably was different, and you never had to pay attention to APRs or variable rates. In America, interest is baked into just about everything: credit cards, car loans, student loans even in one weird little corner of the health care system.

What Is an Interest Rate, Really?

The interest rate is like a rental cost for money. And when a bank or credit card company lends you money, they charge you for it with a percentage of that amount each year as the price for getting to borrow the money. When you take out a loan for $1,000 at 20%, essentially what you're doing is giving them back $1,000 and then also paying them back some of that 20% depending on how long it takes you to pay it back.

You will also often see those two related terms are interest rate and APR (Annual Percentage Rate). They may sound the same, but they are not exactly identical. The interest rate itself is only how much you have to pay for the money in terms of borrowing. And APR is not just the interest rate but also some other lender charges like origination fees. That's why the APR on a loan is sometimes a wee bit higher than that interest rate you were quoted and it's the number to compare when you're shopping between lenders.

Then there is a difference between fixed and variable rates. A fixed rate remains constant over the entirety of the loan an auto loan, for example, or generally speaking any private student loan works this way. A variable rate can be both good or bad over time, but generally follows larger economic trends. Variable rates are one reason credit card debt can quietly get pricier even if you haven't made a single new charge.

Simple Interest vs. Compound Interest

This is where it gets expensive, if you're not careful. You can also think of it as: Simple interest is based solely on your opening balance. With compound interest, you are charged interest on your initial balance as well as any accumulated interest so in effect, you start paying interest on your interest.

Lets say you have a $5000 credit card balace at 20% interest, and make just the minimum monthly payment. As a result of the daily compounding interest associated with credit card debt, you are charged interest on an ever-increasing balance even as you make payments. That $5,000 debt may low-key become one that takes years to pay off and costs thousands above the original amount not because you let it accrue more spending, but how compounding works.

How Interest Rates Directly Affect Your Debt

Your interest rate isn't just a number on a statement it shapes almost every part of your repayment experience.

Your monthly minimum payment. A higher rate usually means a higher minimum payment, because more of that payment is going toward interest rather than your actual balance.

How long it takes to pay off your debt. Higher rates stretch out your payoff timeline, sometimes by years, especially if you're only making minimum payments.

How much you pay in total. This is the part people underestimate. Two people can borrow the exact same amount and end up paying wildly different totals, just because of the rate they were charged.

Which debts you should tackle first. When you're juggling multiple balances, the interest rate not the size of the balance is usually what should guide which one you pay off first.

Here's a simple side-by-side to show how much of a difference the rate alone makes on the exact same $10,000 balance, assuming a $300 monthly payment:

12% APR | 22% APR | |

Monthly payment | $300 | $300 |

Time to pay off | ~39 months | ~55 months |

Total interest paid | ~$1,750 | ~$5,900 |

Same amount borrowed. Same monthly payment. But the higher rate costs over $4,000 more and takes over a year longer to pay off. That's the real weight an interest rate carries.

Why Do Interest Rates Change? (The Federal Reserve's Role)

You may have heard news about the Federal Reserve "raising rates" or "cutting rates" and wondered what that has to do with your credit card. The Federal Reserve is the US central bank, and one of its main tools for managing the economy is setting a benchmark rate that influences how much it costs banks to borrow money from each other.

When that benchmark rate goes up, banks and lenders typically pass some of that cost on to you, especially on variable-rate debt like credit cards. This means your APR can climb even if you never missed a payment or added a new charge simply because broader interest rates moved. The reverse is also true: when the Fed lowers rates, variable-rate debt can get a little cheaper over time.

This matters for planning ahead. If you're carrying credit card debt, it's worth knowing that your rate isn't fixed in stone just because your card company set it once. It can shift with the broader economy, which is one more reason high-interest debt deserves a plan rather than just minimum payments on autopilot.

What Determines Your Interest Rate

Not everyone gets the same rate for the same type of loan. Lenders look at several personal factors to decide what to offer you:

Credit score — a numeric snapshot of how reliably you've repaid debt in the past

Length of credit history — how long you've had accounts open

Debt-to-income ratio — how much you owe compared to how much you earn

Type of debt — credit cards typically carry higher rates than secured loans like auto loans, because there's less collateral backing them

Which lender or card issuer you use — rates vary company to company for the same borrower

Here's something worth naming directly: if you recently moved to the US, or you're building credit for the first time as an adult, you may have what's called a "thin" credit file meaning there isn't much history for lenders to judge you by. Even with a strong income and no history of missed payments anywhere, this often results in a higher starting interest rate than someone with five or ten years of US credit history. It can feel unfair, especially if you've never missed a bill in your life. The good news is that this is very fixable it just takes a bit of intentional groundwork.

Building Credit History as a Newcomer or First-Generation Borrower

A few practical starting points:

Secured credit card. You put down a deposit (often $200–$500), which becomes your credit limit. Used responsibly, it builds a payment history just like a regular card.

Credit-builder loan. Offered by many credit unions and community banks you make small payments into a locked savings account, and each payment is reported to the credit bureaus.

Rent-reporting services. Some services report your on-time rent payments to credit bureaus, turning a bill you're already paying into credit history.

Becoming an authorized user. If a trusted family member with strong credit adds you to their card as an authorized user, their positive history can help build yours too.

None of these fix a rate overnight, but six to twelve months of consistent, on-time activity can noticeably improve the rates you're offered going forward.

How Rising Interest Rates Affect Different Types of Debt

Not all debt reacts to rate changes the same way. Here's a quick breakdown.

Credit Card Debt

Almost always variable-rate, which means credit card debt is the most directly exposed to rate increases. If you carry a balance, a Fed rate hike can raise your APR within a billing cycle or two, increasing your minimum payment without you spending a single extra dollar.

Personal Loans

These can be fixed or variable depending on the lender. Fixed-rate personal loans are predictable your payment won't change even if the broader rate environment shifts. This predictability is part of why personal loans are sometimes used to consolidate higher-rate credit card debt.

Auto Loans

Typically fixed for the life of the loan once you sign. Your existing auto loan payment won't move with rate changes, but if you're shopping for a new loan, rising rates mean new auto loans get pricier for everyone.

Student Loans (Federal vs. Private)

Federal student loans usually carry a fixed rate set at the time you borrow, so they're largely insulated from Fed rate changes after the fact. Private student loans, on the other hand, are often variable and behave more like a personal loan worth watching closely if that's part of your debt picture.

The Real Cost of Minimum Payments

Minimum payments exist to keep your account in good standing not to get you out of debt quickly. On a high-interest credit card, paying only the minimum each month can mean it takes well over a decade to clear a balance you could have paid off in a few years with slightly higher payments, and you could end up paying two to three times the original amount in interest alone.

This isn't about blaming anyone for paying the minimum sometimes it's genuinely all that fits in the budget that month. But it's worth knowing the trade-off clearly: the minimum payment protects your credit report, not your wallet.

Strategies to Reduce the Impact of High Interest Rates

After you know what your rate is costing could be when it comes to money and stress, a few actionable tips can help more than you think.

Debt avalanche vs. debt snowball. The avalanche method is to focus on the debt with the highest interest rates first, paying as little as possible on everything else which mathematically saves you money in the long term. The snowball method involves paying down your smallest balance first, irrespective of rate. It builds momentum and is more motivational. Neither is "wrong" you will actually stick with the best method.

Balance transfer cards. Certain credit cards feature a low or even 0% teaser phase on transferring the debt from a card with higher interest. Transfers are usually accompanied by a fee (typically 3–5% of the balance) and unless you pay off the transfer or raise your overall credit score, at the end of serving time in promotional limbo, it is affordable to be slammed with a fixed amount and debt load at today's high standard rates.

Debt consolidation loans. By rolling multiple high-interest debts into one loan at a lower, fixed rate, you can reduce the total interest you'll pay and simplify your payments provided that the new rate moves the needle and is actually lower than what you're already paying on different compromise.

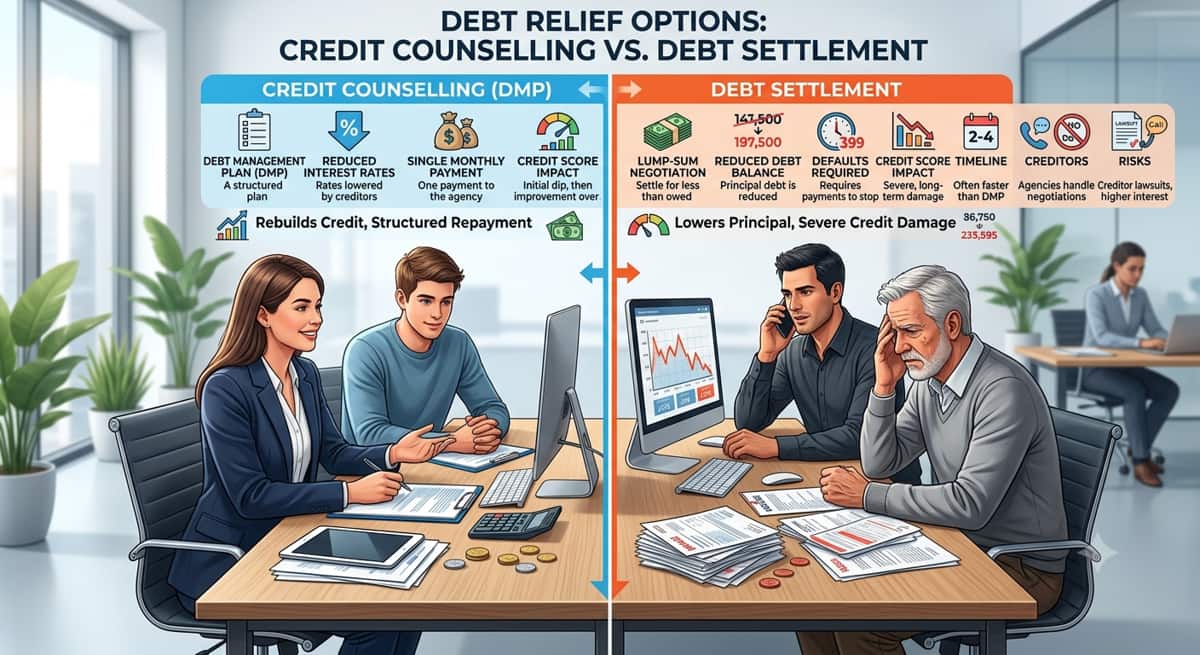

Nonprofit Credit Counseling And Debt Management Plans. Approved non-profit credit therapy agencie may contact your creditors directly to look for lower interest levels, merging the payments into a single monthly payment. This is unlike a loan you are not adding debt but simply reorganizing the debt you already have.

Debt settlement. This means reaching an agreement with creditors to settle debt for less than the total amount owed, typically in one payment. It can decrease your debt for less money but usually does a real number on your credit score and may have tax issues so I wouldn't recommend to go in lightly or blind.

A note for interest-conscious borrowers. If your family has made the decision to avoid interest-based products for religious reasons, there are still a few ways that you can win: use additional or bonus money to pay off principal only; find other community funding alternatives (if and where applicable); prioritize debt payoff timelines that don't include switching or balance transfers/loans. You might want to talk it through with a finance counselor who knows about these sorts of things.

A Note on Remittances and Debt Repayment Priorities

For many South Asian families in the US, there's an added layer most personal finance advice doesn't talk about: the ongoing responsibility of sending money home. Balancing debt repayment with remittances to parents or extended family can feel like an impossible juggling act, especially when both feel non-negotiable.

There's no one-size-fits-all answer here, and this isn't about choosing one over the other. But it can help to look at the math side by side: high-interest debt typically grows faster than most remittance needs can be safely delayed for a short period. Having an honest conversation with family about temporarily adjusting the amount or timing of transfers even for a few months while you pay down a high-rate balance can end up saving real money for everyone in the long run, rather than paying interest charges that benefit no one.

When to Consider Professional Debt Relief Help

A few signs it might be time to bring in outside help:

Your balance isn't going down much even though you're paying every month

You're using credit cards to cover everyday essentials like groceries or bills

Your variable-rate debt has climbed noticeably and your payments feel harder to keep up with

You're losing sleep or avoiding opening your statements

If any of this sounds familiar, legitimate help is available. Look for NFCC-accredited nonprofit credit counseling agencies, which offer free or low-cost consultations and can help you build a realistic debt management plan. Certified financial counselors can also help you look at your full picture income, expenses, and debt and map out a plan.

One important word of caution: debt relief scams disproportionately target immigrant and first-generation communities, often through cold calls, aggressive ads, or someone claiming they can "erase" your debt for an upfront fee. Watch for these red flags:

Asking for payment before any service is provided

Guaranteeing they can eliminate your debt or stop all collection calls

Pressuring you to act immediately without giving you time to think

Refusing to explain their process clearly in writing

A legitimate credit counselor will never guarantee outcomes and will always explain fees upfront.

Bringing It All Together

Your interest rate is one of many, but perhaps the strongest influences on what your debt actually costs you often stronger than the amount itself. Knowing how it works satisfies curiosity, but also alters actual decisions: which debt to tackle first, whether or not consolidation is going to help out at all, and when you should call for outside professional assistance.

If you are at a loss as to where you should begin, we want you to know that you do not have to take the journey alone. Also, a no-fee consultation with a nonprofit credit counselor can clarify your whole picture so you produce an actual plan that conforms to your life not some very rudimentary template.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Do Debt Relief Programs Work?

11 min read

Does Debt Affect Your Credit Score?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation