Credit Counselling vs. Debt Settlement: Which One Is Right for You?

If you're lying awake at night doing math in your head, you're not alone. Maybe it's credit card balances that keep growing every month no matter how much you pay. Maybe it’s a medical bill you didn’t anticipate, or a business that didn’t pan out the way you hoped. Or maybe you’re trying to manage your own rent, groceries and car payment while still sending money home to parents or siblings who are depending on you. For many South Asian families in the US, debt isn’t just a financial issue. It feels personal.

There's the quiet fear of what relatives might think if they found out. There is pressure to “have it all figured out,” especially when you are the person that everyone else comes to for advice. And there is a deeply-ingrained habit, passed down from generation to generation, of dealing with problems privately instead of asking for help. Many of us grew up watching our parents quietly absorb financial stress rather than talk about it openly, and that habit doesn't just disappear once we're the ones paying the bills.

Here's the good news: you don't have to choose between suffering in silence and declaring bankruptcy. There are real, practical paths that can bring your debt under control, and two of the most common ones are credit counselling and debt settlement. They sound similar on the surface. Both involve working with a company that helps you deal with debt, and both can lead you toward becoming debt-free. But underneath, they work in almost opposite ways, and picking the right one can save you years of stress, protect your credit, and put real money back in your pocket.

What Is Credit Counselling?

Credit counseling is a service that helps people manage debt, create a realistic budget, and improve their overall financial health.

Credit counselling is one of the gentler ways to deal with debt. Think of it as sitting down with someone whose entire job is to look at your income, your bills, and your debt, and help you build a realistic plan to pay it all off.

Here's how it usually works, step by step:

A free or low-cost review of your finances. A certified counselor (often from a nonprofit agency) looks at what you earn, what you owe, and where your money is going each month.

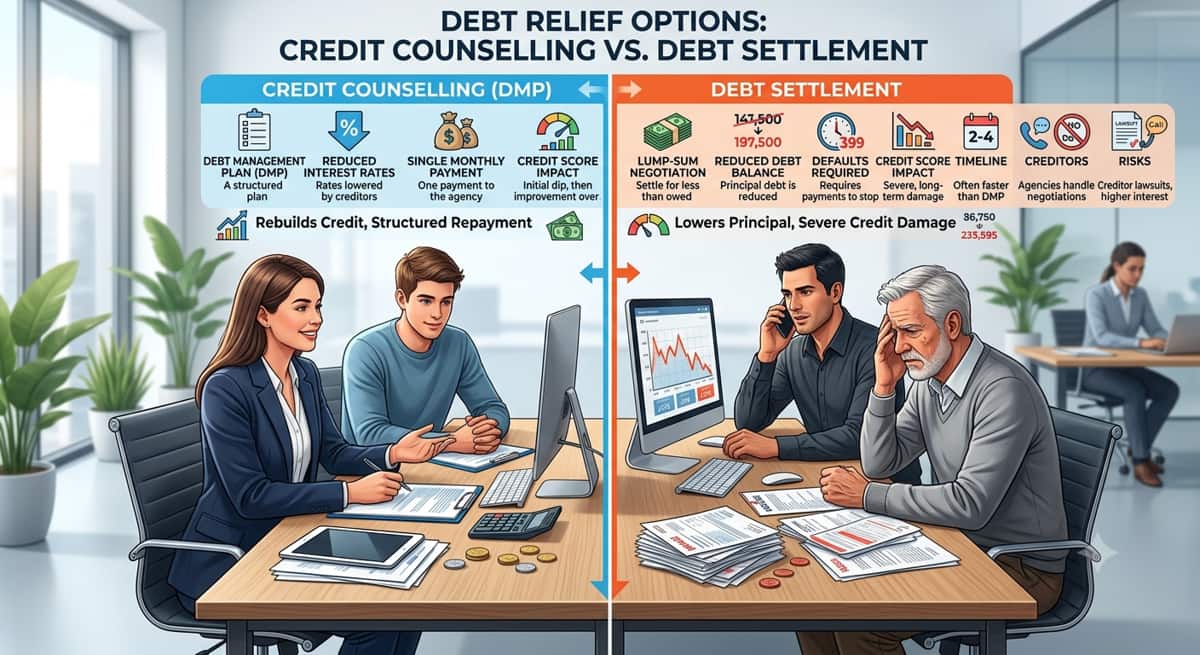

You may be enrolled in a Debt Management Plan (DMP). This is a structured repayment plan, usually for credit card debt, that combines everything into one monthly payment.

The agency talks to your creditors on your behalf. They often succeed in getting your interest rates lowered, which means more of your payment goes toward the actual debt instead of interest.

You make one monthly payment to the agency, and they distribute it to each of your creditors.

Credit counselling typically lasts three to five years, and the monthly fees are usually modest since many agencies are nonprofit and regulated by the state. It's worth noting that this option doesn't erase what you owe. It simply makes paying it back more manageable, by lowering interest costs and combining debt into one predictable bill instead of five or six different due dates to remember.

For a lot of people, that predictability is the biggest relief. Instead of juggling a bunch of minimum payments, and watching interest eat away at your progress, you get one clear number to plan around each month, and a realistic date when you’ll finally be done.

What Is Debt Settlement?

Debt settlement takes a different approach. Instead of paying off everything you owe, the goal is to convince creditors to accept less than the full amount.

Here's how the process typically works:

You stop paying your creditors directly. Instead, you deposit money into a separate savings account each month.

Once enough money builds up, the settlement company negotiates with your creditors. They offer a lump sum, often a percentage of what you originally owed, in exchange for considering the debt settled.

If creditors agree, your debt is resolved for less than the full balance.

Fees are usually charged as a percentage of your enrolled or settled debt, so the more debt you have, the more you'll likely pay in fees.

There's an important catch, though. While you're saving up for that lump-sum offer, you're not paying your creditors at all. That means missed payments can pile up, collection calls may increase, and in some cases you could even face a lawsuit before a settlement is reached. There can also be tax implications, since forgiven debt is sometimes treated as taxable income by the IRS.

This option can genuinely work, and many people do come out the other side owing significantly less than they started with. But it requires a certain amount of patience and thick skin, since the months in between enrollment and settlement can feel uncertain, and not every creditor agrees to settle. Understanding that upfront helps set realistic expectations before you commit.

Key Differences Between Credit Counselling and Debt Settlement

On the surface, both options promise relief from debt. But they get there in very different ways, and those differences matter a lot depending on your situation, your timeline, and how much risk you're willing to take on. Let's break it down piece by piece.

How Each One Affects Your Credit Score

Credit counselling tends to be gentle on your credit score. You might see a small, temporary dip, especially if some accounts get closed as part of the plan, but overall, your score usually recovers steadily as you make consistent, on-time payments through the program.

Debt settlement is a different story. Because you stop paying creditors while you save up for a settlement, your credit takes a real hit. Missed payments and "settled for less than owed" notes can stay on your credit report for up to seven years, which can make it harder to qualify for loans, credit cards, or even some apartments during that time. If you're planning to apply for a mortgage, sponsor a family member's visa paperwork that requires financial documentation, or make any major purchase in the next few years, this is worth weighing carefully.

How Long Each Option Takes

A Debt Management Plan through credit counselling usually runs three to five years. It's predictable. You know roughly when you'll be debt-free from day one.

Debt settlement is often estimated at two to four years, but that timeline can stretch depending on how quickly you can save enough to make settlement offers, and how willing your creditors are to negotiate.

Cost and Fees

Credit counselling agencies, especially nonprofit ones, usually charge low monthly fees, and many states cap what they're allowed to charge. It's a fairly affordable option for the service you're getting.

Debt settlement companies typically charge more, often 15% to 25% of your enrolled or settled debt. On a large balance, that can add up to a significant amount, so it's worth doing the math on what you'd actually pay in fees before comparing it to what you'd save. One important warning: it's illegal for these companies to charge you fees before they've actually settled a debt. If a company asks for money upfront before doing any work, that's a red flag worth taking seriously, and a good reason to look elsewhere.

Impact on Your Relationship with Creditors

With credit counselling, your creditors stay in the loop and keep receiving payments, so the relationship generally stays cooperative.

With debt settlement, things can get tense. Since you're not making payments during the savings period, creditors may call frequently, send notices, or in some cases pursue legal action before a settlement is reached.

Which Option Fits Your Financial Situation?

There's no single "best" answer here. It really depends on your income, how much debt you're carrying, and what you're comfortable with.

When Credit Counselling Makes More Sense

Credit counselling tends to work well if:

You have a steady income and can commit to a monthly payment plan

Protecting your credit score matters to you, maybe because you're planning to buy a home, sponsor a family member, or apply for a loan soon

You want predictability instead of uncertainty

You'd rather avoid the stress of collection calls and a strained relationship with creditors

This option is often a good fit for people who are managing debt within a stable but tight budget, including those balancing bills here with financial responsibilities to family abroad. For example, if you have a steady paycheck but your credit card balances have crept up over a few years, and you just need a structured way to bring them down without the added stress of a damaged credit score, credit counselling is often the more comfortable route.

When Debt Settlement Makes More Sense

Debt settlement might make more sense if:

Your debt load is large compared to your income, and a full repayment plan simply isn't realistic

Your income has dropped significantly and you're struggling to keep up with even reduced payments

You've looked at bankruptcy as the likely alternative and want to try one more option first

You're willing to accept a credit score hit now in exchange for the possibility of resolving debt faster and for less money

This path usually makes the most sense for people in more serious financial hardship, not those who are simply looking for a slightly easier payment plan. For example, if a job loss, medical emergency, or business setback has left you owing far more than you can realistically pay back in full, even with lower interest rates, debt settlement may offer a more realistic way out than continuing to fall further behind.

Pros and Cons at a Glance

Sometimes it helps to see everything side by side.

Factor | Credit Counselling | Debt Settlement |

Credit Score Impact | Low | High |

Typical Timeline | 3–5 years | 2–4 years |

Fees | Low, regulated | Higher, % of debt |

Reduces Principal? | No (reduces interest instead) | Yes |

Creditor Relationship | Stays cooperative | Often strained |

Risk of Lawsuits | Low | Higher |

In short: credit counselling trades a longer timeline for stability and credit protection, while debt settlement trades credit and certainty for the chance to pay off less overall. Neither one is objectively "better." They're built for different situations, and the right choice really comes down to what you owe, what you earn, and what kind of process you can realistically stick with for the next few years.

Common Myths About Both Options

There's a lot of misinformation out there. Let's clear a few things up.

Myth: "Both options destroy your credit the same way." Fact: They don't. Credit counselling generally has a much smaller impact than debt settlement, which can significantly damage your score for years.

Myth: "Debt settlement is always faster and cheaper." Fact: It depends entirely on how much you owe, how cooperative your creditors are, and how much you can save each month. It's not a guaranteed shortcut.

Myth: "Credit counselling is basically the same as bankruptcy." Fact: Not at all. Credit counselling is a voluntary program, not a legal process, and it doesn't show up on your record the way bankruptcy does.

Myth: "All debt relief companies are the same." Fact: There's a big difference between nonprofit credit counselling agencies and for-profit debt settlement companies. Always check for accreditation, read the fee structure carefully, and be cautious of any company promising guaranteed results or asking for money upfront.

Myth: "Once you enroll, you're stuck no matter what." Fact: Neither option is a life sentence. You can typically leave a debt management plan or a settlement program if your circumstances change, though it's worth understanding any fees or consequences of stopping early before you sign up.

Understanding the truth behind these myths matters, because a lot of people either avoid getting help altogether or pick the wrong option simply because they believed something that wasn't accurate.

How Ooraa Can Help You Choose the Right Path

Deciding between credit counselling and debt settlement isn't something you should have to figure out alone, especially when every family's financial situation looks a little different. Maybe you're supporting parents overseas. Maybe you're the one everyone else turns to for advice, which makes it even harder to ask for help yourself.

At Ooraa, we take the time to actually understand your full picture, your income, your goals, your family obligations, and your comfort level with risk, before recommending anything. Our certified counselors walk you through both options honestly, including the trade-offs, so you can make a decision with confidence instead of guesswork.

We know that for many South Asian families, this isn't just about numbers on a page. It's about protecting your ability to support the people who depend on you, while also finally getting some breathing room for yourself. Because of that, there’s no pressure, no confusing fine print or judgment in our process. Just a straightforward, free consultation to help you see your options and choose what really makes sense for your life.

Take the First Step Toward a Debt-Free Life

At the end of the day, the choice between credit counselling and debt settlement comes down to this: do you want a steadier path that protects your credit, or a potentially faster path that comes with more risk and a bigger credit impact?

Dealing with debt takes real courage, especially when there's family watching, expectations to manage, and years of "just push through it" advice in the back of your mind. But you don't have to push through it alone, and you don't have to have it all figured out before reaching out for help. Taking the first step, even just learning your options, is already progress.

Whichever path fits your life better, the most important thing is that you're no longer carrying this weight in silence. There is a way forward, and it starts with one honest conversation about where you stand today.

If you're ready to talk it through, schedule a free consultation with Ooraa today and take that first real step toward a debt-free life.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

Everything You Need To Know About Consolidating Credit Card Debt

12 min read

Do Debt Relief Programs Work?

11 min read

Debt Settlement- The Best Way To Avoid A Lawsuit

10 min read

How to Settle Debt With Bank of America in 2026

10 min read

Negotiating Debt Settlements For Your Business Debt

11 min read

Debt Management- The Right Program

9 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation