How Can You Settle Credit Card Debt Without Bankruptcy?

Credit card debt doesn't usually begin with one big mistake. More often, it grows from everyday life. A medical emergency, higher living costs, job loss, unexpected repairs, or helping family members can all lead to relying on credit cards a little more than planned. At first, the balance feels manageable. You make the minimum payment, expecting to catch up later. But as interest keeps adding up, paying off the debt becomes much harder.

If you're feeling stuck, you're not alone. Many hardworking people find themselves in this position, even if they've always tried to manage their money responsibly. For many South Asian families, the challenge can be even greater. It's common to balance expenses in the U.S. while supporting parents, siblings, or relatives overseas. At the same time, debt is often seen as something to keep private, making it difficult to ask for advice or explore available options.

The good news is that bankruptcy isn't the only way to deal with overwhelming credit card debt. Depending on your situation, you may be able to settle your debt, negotiate with creditors, or choose another solution that helps you regain control without taking such a major financial step.

What Does It Mean to "Settle" Credit Card Debt?

Settling credit card debt means negotiating with your creditor to pay less than the full amount you owe as a final payment. Once the agreed amount is paid, the remaining balance is forgiven, and the account is considered resolved.

When you pay off a credit card, you return every dollar and the interest on that dollar that you took out. Bankruptcy erases some or all of what you owe, but it does so through a lengthy process with severe long-term effects.

Neither of these two processes involve the same process as settling your debt. This means you (or someone acting on your behalf) get in touch with the credit card company (or collection agency) and, then bargain to pay less than the full amount usually upfront and they agree that this will count as the debt being "satisfied" or settled, and all further action to chase the rest of it is dropped. So say for instance you owed $10,000 and the debt collector agrees to one payment of $6,000. The balance of $4,000 would then be wiped clean.

Now one thing which a lot of people get confused with this is debt consolidation. Not even close to the same thing; When you consolidate, you're borrowing with a new loan or card to lump together different debts into one monthly payment but you're not walking away from anything; simply paying for it in a more straightforward manner. Settlement, however, lowers your amount owed.

Now it is important to recognize the difference, as that changes which option suits your case.

Signs You May Need Debt Relief (Before Considering Bankruptcy)

Sometimes it's hard to know if you're just going through a tight month or if things have actually gotten out of hand. Here are some honest signs it might be time to look into debt relief:

You're only paying the minimum. Every month, you pay just enough to keep the account from going into default but the balance barely moves.

Your cards are maxed out, or close to it. You're using most or all of your available credit, with little room to breathe if something unexpected comes up.

You're using one card to pay another. Robbing Peter to pay Paul has become a regular habit, not a one-time fix.

You've missed a payment or two. Maybe it was an honest mistake at first, but now it's starting to happen more often.

Collections calls have started. You're getting calls or letters about overdue accounts, and you've been avoiding picking up.

If two or more of these sound like you, it's a good time to look at your options before things get harder to manage.

Debt Settlement vs. Other Debt Relief Options

With so many options out there, it's easy to feel confused about which one actually fits your situation. Here's a simple side-by-side look to help you compare.

Option | How It Works | Typical Cost/Fees | Credit Score Impact | Timeline | Best For |

DIY Negotiation | You contact the creditor directly and ask to settle for less | No fees, just your time | Moderate dip while unpaid | A few weeks to a few months | People comfortable negotiating and with some savings to offer a lump sum |

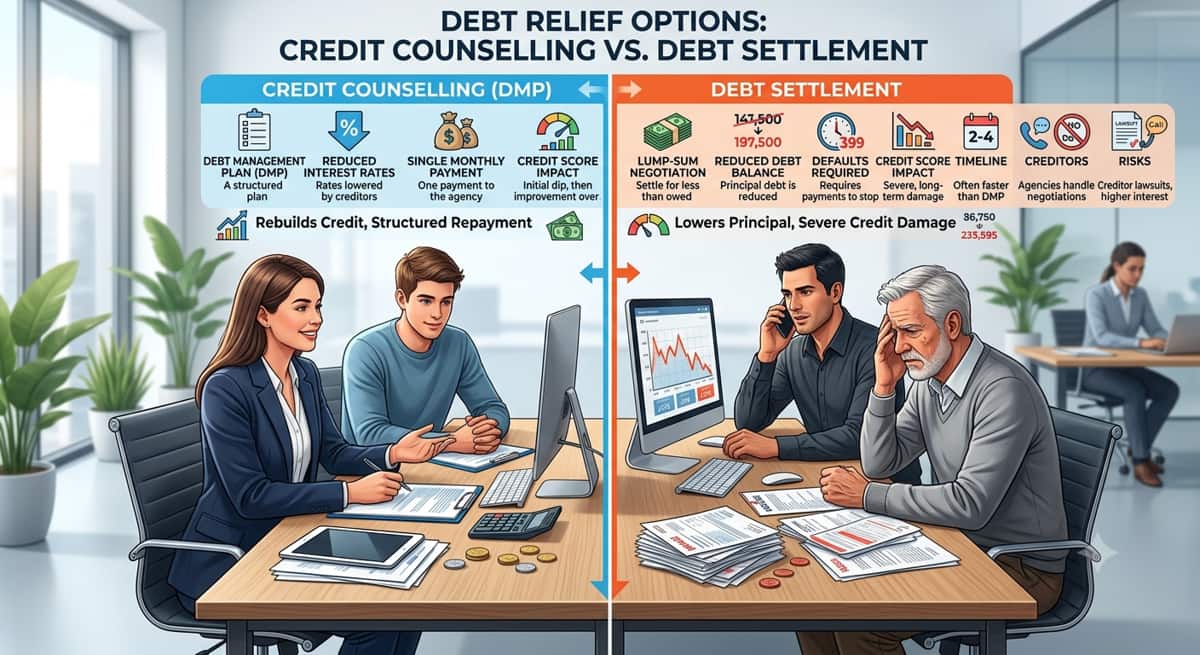

Nonprofit Credit Counseling (DMP) | An agency negotiates lower interest rates and combines payments into one | Small monthly fee (often $25–$50) | Mild, often recovers faster | 3–5 years | People who want structure and support without going the settlement route |

Debt Settlement Company | A company negotiates lump-sum settlements on your behalf | Fees based on % of debt settled | Bigger dip at first, especially while payments are paused | 2–4 years | People with larger debt who want expert help but can handle a credit hit |

Debt Consolidation Loan | You take a new loan to pay off all cards, then repay just the loan | Interest on new loan | Small dip, then often improves | 2–5 years | People with decent credit who want one simple payment |

Balance Transfer | Move balance to a card with 0% intro interest | Transfer fee (often 3–5%) | Small dip from new account | Usually 12–18 months | People with good credit who can pay it off before the intro period ends |

Bankruptcy (Ch. 7/13) | Court legally discharges or restructures debt | Court and attorney fees | Major, lasts 7–10 years | Several months to years | People with debt too large to manage through any other option |

As you can see, there's no single "best" option it really depends on how much you owe, how your credit looks right now, and how much support you want along the way.

5 Ways to Settle Credit Card Debt Without Filing Bankruptcy

Once you know where you stand, here are five real paths forward no bankruptcy required.

1. Negotiate Directly With Your Credit Card Company

You can call your credit card company yourself and simply ask for help. Explain your situation honestly job loss, medical bills, family emergency, whatever it is and ask if they have a hardship program or if they're willing to settle for a lower payoff amount. Many companies would rather get some money back than none at all, especially if you've fallen behind.

A simple way to start the call: "I'm going through a difficult financial time and want to pay what I can. Would you be willing to settle this account for a lower amount?"

Whatever they agree to, always get it in writing before you send a single payment. A verbal promise isn't enough to protect you later.

2. Work With a Nonprofit Credit Counseling Agency

If negotiating on your own feels overwhelming, a nonprofit credit counseling agency can step in and do it for you. Look for one accredited by the NFCC (National Foundation for Credit Counseling) this helps you avoid shady operators. These agencies typically set you up on a Debt Management Plan, where they work with your creditors to lower your interest rate and combine all your cards into one manageable monthly payment. Unlike debt settlement, this usually doesn't reduce how much you owe but it makes paying it off far less stressful, often within three to five years.

3. Hire a Debt Settlement Company

For-profit debt settlement company negotiate directly with your creditors on your behalf, aiming to settle your accounts for less than you owe. Here's how it typically works: instead of paying your creditors, you deposit money into a dedicated savings account each month. Once enough builds up, the company uses it to negotiate lump-sum settlements. They only get paid a fee once a debt is actually settled this is required by federal law (the FTC's Telemarketing Sales Rule), so be wary of any company asking for money upfront. Keep in mind your credit score usually drops further at first, since payments are paused while savings build up.

4. Consolidate With a Personal Loan

A debt consolidation loan lets you pay off all your credit cards at once using a new loan with a fixed interest rate and a set repayment term. This doesn't lower how much you owe, but it often means a lower interest rate and one predictable monthly payment instead of juggling several. You'll need reasonably good credit to qualify for a decent rate, so this option tends to work best if your credit hasn't taken too big a hit yet.

5. Use a 0% APR Balance Transfer Card

If your credit is still in decent shape, a balance transfer card can help you pay down debt without interest piling up. You move your existing balance onto a new card offering 0% interest for a set period, usually 12 to 18 months. There's typically a one-time transfer fee, often 3–5% of the balance. The catch is timing if you don't pay off the full balance before the introductory period ends, the remaining amount can start collecting interest at a much higher rate.

Pros and Cons of Credit Card Debt Settlement

Like any financial decision, debt settlement isn't perfect for everyone. Here's an honest look at both sides so you can weigh it clearly.

The Upsides

You could pay back less than you owe. In many cases, you settle for a portion of the original balance, not the full amount.

You avoid bankruptcy. No court process, no public record tied to a bankruptcy filing, and fewer long-term restrictions on your finances.

It can be faster than the slow grind of minimum payments. Instead of watching a balance barely shrink for years, settlement can resolve the debt in a more defined timeline.

The Downsides

Your credit score will likely drop first. Especially if payments are paused while you build up savings to negotiate with.

You may face collection calls or even a lawsuit while the debt sits unpaid. Creditors aren't required to wait patiently during this process.

The forgiven amount may count as taxable income. The IRS can treat forgiven debt as income you have to report.

There are often fees involved, especially if you work with a for-profit settlement company.

Weighing these honestly will help you decide if this path truly fits your situation.

Will Debt Settlement Hurt Your Credit Score? (And for How Long)

Debt settlement usually involves missing payments for a while before a settlement is reached, especially if you're building up savings for a lump-sum offer or working with a settlement company. Those missed payments are what really hurt your score, more than the settlement itself. Once an account is settled, it gets marked as settled on your credit report instead of "paid in full," which lenders can see for up to seven years.

But here's the part that gives most people hope your score doesn't stay low the whole time. Once the debt is settled and you start rebuilding good habits, like paying other bills on time and keeping your credit use low, your score typically starts climbing again within a year or two. Many people see real improvement well before that seven-year mark, especially if this was their only major setback.

Think of it as a dip, not a permanent ceiling. The sooner you settle and start fresh, the sooner your score starts working in your favor again.

Are Settled Debts Taxable? Understanding the 1099-C

Here's something a lot of people don't expect: the amount of debt that gets forgiven can actually count as taxable income.

If a creditor forgives $600 or more of your debt, they're required by the IRS to send you a Form 1099-C, "Cancellation of Debt." That forgiven amount then has to be reported on your tax return, just like regular income, and you may owe taxes on it. So if you settle a $10,000 balance for $6,000, that $4,000 difference could be treated as income by the IRS.

There is an exception worth knowing about, called "insolvency." If your total debts were greater than everything you own at the time the debt was forgiven, you may not have to pay taxes on that forgiven amount. This can get technical fast, though.

Because tax situations vary so much from person to person, it's worth setting aside a little money for a possible tax bill after settlement, and talking to a tax professional, so there are no surprises later.

How to Avoid Debt Settlement Scams Targeting Immigrant Communities

Unfortunately, debt settlement is an area where scammers actively target immigrant families, especially those who are newer to the U.S. financial system or more comfortable in a language other than English. Knowing the warning signs can protect you and your hard-earned money.

Red flags to watch for:

They ask for payment before settling anything. Legitimate companies only charge fees after a debt is actually settled this is the law, not just good practice.

They "guarantee" results. No honest company can promise your creditors will agree to a specific settlement.

They tell you to stop talking to your creditors completely, or to ignore calls and letters. This can leave you unprotected and unaware of what's really happening with your accounts.

They aren't licensed or accredited, and get vague or defensive when you ask questions.

How to check if a company is legitimate:

Look for NFCC accreditation.

Confirm they're licensed to operate in your state.

Search their name in the FTC and CFPB complaint databases before signing anything.

If something feels rushed, too good to be true, or hard to get straight answers about, trust that instinct and take your time.

Choosing the Right Path to Becoming Debt-Free

There's no one-size-fits-all answer here. Your best move is all about your debt amount, how bad you want to save your credit, how the time frame looks, and frankly how confident you are negotiating for yourself or with a coach helping process off of it.

If you're still not sure where to begin, one great first step is contacting an NFCC-accredited nonprofit credit counselor. And of course there is pressure to sign up with some for-profit company, where all your data will be stored and commodified as personal information: laid back, partially free or low-cost nonprofit education (including MOOC) gives you this freedom so you can see the picture clearly before obliging yourself.

No matter what you decide, just know this it IS possible to get out of debt and having help along the way is NOT a failure. This is the first step to receiving your peace of mind back.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Everything You Need To Know About Consolidating Credit Card Debt

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Do Debt Relief Programs Work?

11 min read

Does Debt Affect Your Credit Score?

11 min read

Debt Settlement- The Best Way To Avoid A Lawsuit

10 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation