Understanding the Basics: What is Chapter 13 Bankruptcy?

Chapter 13 bankruptcy is a legal process known as a reorganization bankruptcy. It's designed specifically for individuals with a steady, reliable income who need help managing their debt but want to avoid selling off their property. Think of it not as a way to wipe out your debts completely, but as a structured plan to pay back a portion of what you owe over a set period. This is the core difference between Chapter 13 and Chapter 7 bankruptcy. In a Chapter 7 bankruptcy, a trustee liquidates (sells) a debtor's non-exempt assets to pay off creditors. The remaining eligible debts are then discharged. With Chapter 13, you keep your assets. Instead, you enter into a repayment plan that typically lasts three to five years. During this time, you make regular, court-ordered payments to a trustee who then distributes the money to your creditors. One of the most significant features of Chapter 13 is the automatic stay, which takes effect the moment you file. This legal protection immediately stops most collection activities, including harassing phone calls, foreclosure proceedings, repossessions, and lawsuits. This provides a crucial window of relief. The repayment plan also allows you to catch up on missed mortgage or car payments and restructure your debts, so you can keep your home, car, and other valuable assets. In a Chapter 13 filing, you can generally keep all of your assets, as long as you can afford to pay for them under the court-approved plan.Is Chapter 13 the Right Fit? A Closer Look at Your Situation

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Related Articles

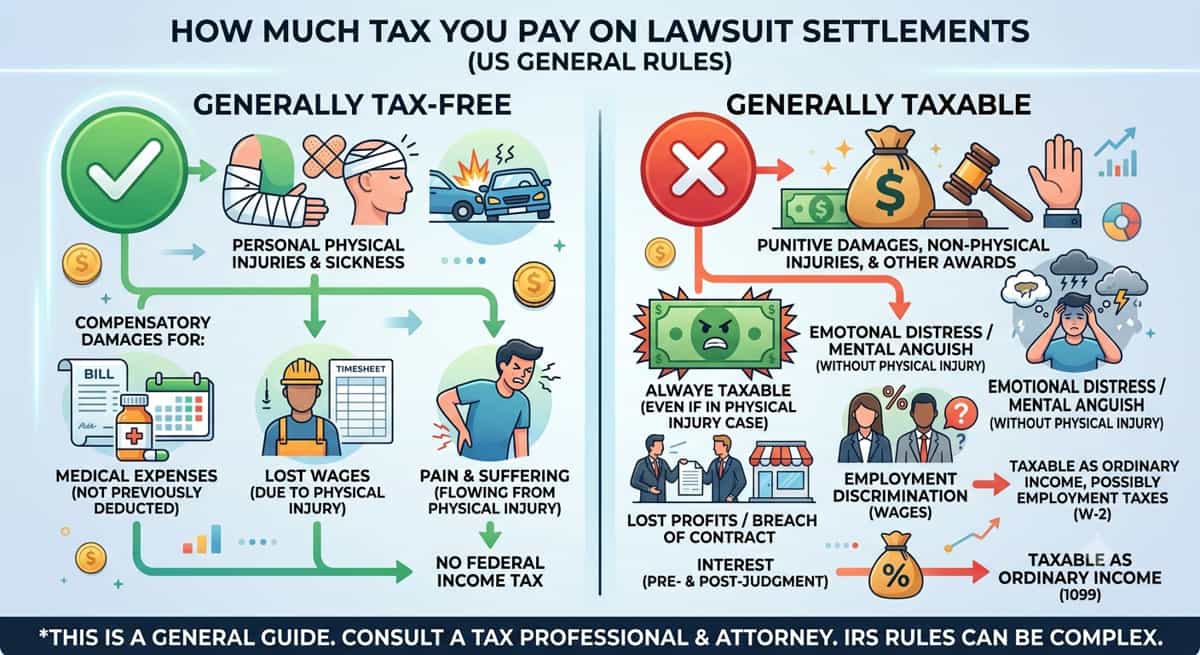

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read