The Pros And Cons Of Filing Chapter 7 Bankruptcy

If you are struggling with overwhelming debt, you may be considering legal options to regain your footing. One of the most common paths is Chapter 7 bankruptcy. Chapter 7 bankruptcy is a legal process in the United States that allows individuals to eliminate most of their unsecured debts, such as credit card balances and medical bills, through a court-ordered discharge. Essentially, it is a federal program designed to provide a "fresh start" to those whose income is insufficient to pay back what they owe.

For South Asian communities living in the U.S., the decision to file for bankruptcy is often more than just a financial one; it is a deeply personal and cultural crossroad. Many individuals feel the weight of the "model minority" myth, which creates an unspoken pressure to appear financially successful and stable at all times. This can make the reality of debt feel like a private failure rather than a manageable financial hurdle.

Furthermore, unique pressures such as sending remittances to family back home in countries like India, Pakistan, or Bangladesh, or the high costs associated with maintaining social standing and community obligations, can accelerate financial strain. It is important to remember that the U.S. legal system views bankruptcy as a tool for economic recovery, not a reflection of your character or your family’s honor. Understanding the pros and cons is the first step toward reclaiming your financial future.

What Is Chapter 7 Bankruptcy?

Chapter 7 bankruptcy is a legal process that wipes out most of your unsecured debt like credit cards and medical bills giving you a fresh financial start. Most people keep their everyday belongings, and the whole process usually wraps up in 3–6 months.

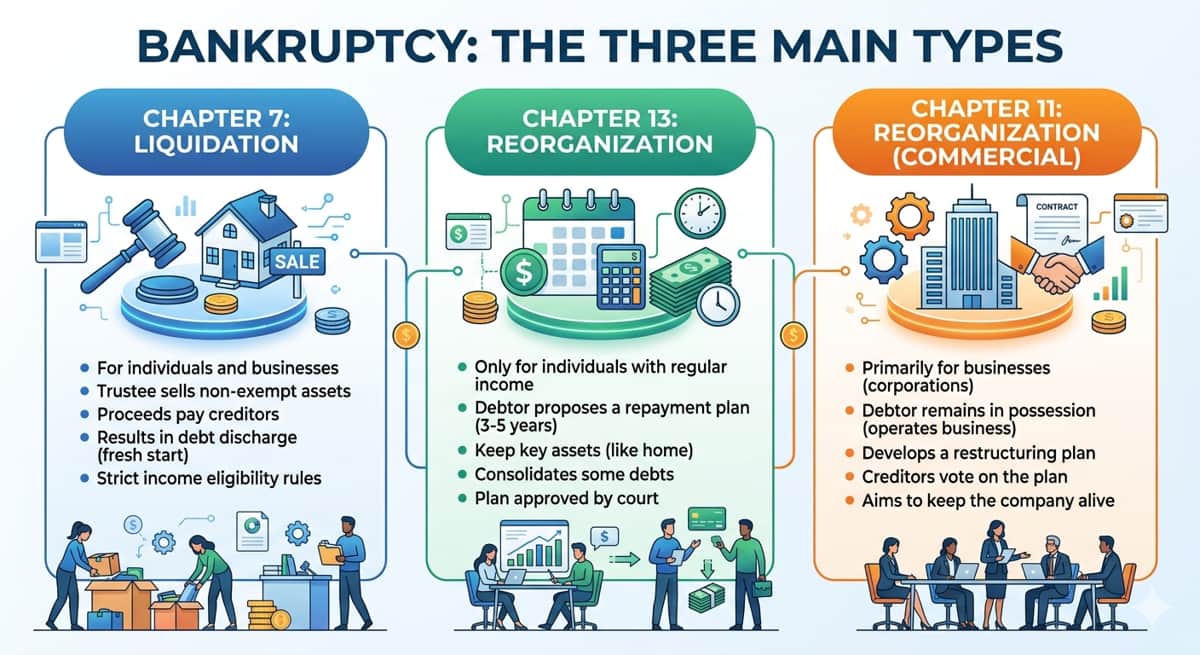

Often called "liquidation bankruptcy," Chapter 7 is a court-supervised process where an appointed trustee reviews what you own to see if anything can be sold to repay what you owe. But the word "liquidation" sounds scarier than it usually is. In reality, most people who file for Chapter 7 walk away keeping their clothes, furniture, and often their car or home thanks to legal protections called exemptions that shield your essential belongings.

Who Actually Qualifies for Chapter 7?

Not everyone can file. To be eligible, you need to pass what the court calls the Means Test, a straightforward calculation that checks whether your income is low enough that repaying your debts simply isn't realistic.

Here's how it works: the test compares your average monthly income over the past six months against the median income for a household your size in your state.

If your income falls below that median, you generally qualify right away — no further questions asked.

If your income is higher, the test takes a closer look at your necessary living expenses things like rent, groceries, and utilities to see what's left over after the basics are covered.

If there's little to nothing left after your essentials, you can typically move forward with Chapter 7 and clear the slate on your qualifying debts.

The Pros of Filing Chapter 7 Bankruptcy

The moment you file for Chapter 7, something called the Automatic Stay kicks in and it's one of the most powerful protections in the entire process. From that point forward, creditors are legally required to stop all collection activity against you.

That means no more constant phone calls from debt collectors. No more wage garnishments eating into your paycheck before it even reaches you. If a creditor is mid-lawsuit or threatening to freeze your bank account, those actions are immediately put on pause.

For families already stretched thin, this alone can bring real emotional relief — giving you the breathing room to focus on what comes next without the fear of your income shrinking overnight.

Most of Your Debt Gets Wiped Out

The end goal of Chapter 7 is something called a discharge, a permanent court order that legally releases you from the obligation to repay certain debts. Once discharged, creditors can never come after that money again.

This applies to most unsecured debts, including:

High-interest credit card balances

Personal loans

Medical bills

For anyone who leaned on credit cards during a period of job loss, a family emergency, or to support loved ones, this discharge can be genuinely life-changing. Instead of sending money toward mounting interest each month, you can finally redirect it toward your actual life.

A Faster Path to a Fresh Start

Chapter 7 is built for speed. Most cases are resolved in four to six months from filing to discharge compared to Chapter 13, which locks you into a repayment plan lasting three to five years.

If you're at a point where repaying what you owe simply isn't possible, waiting five years for relief isn't realistic. Chapter 7 lets you close that chapter relatively quickly and start rebuilding your credit and financial footing within the same year.

You Keep More Than You Might Expect

A lot of people assume bankruptcy means losing everything. That's rarely how it works. Both federal and state laws include exemptions protections that let you hold onto the things essential to your daily life.

In most cases, you can keep:

Clothing and household furniture

Appliances and tools you use for work

A significant amount of equity in your car

Your home, in many situations

The reality is that the vast majority of Chapter 7 cases are "no-asset" cases, meaning everything the filer owns is already protected. You're clearing your debt not starting over from nothing.

The Cons of Filing Chapter 7 Bankruptcy

Filing for Chapter 7 will cause a significant drop in your credit score and the record stays on your credit report for 10 years from the date you file. That's because lenders see a bankruptcy as a sign of high risk, at least in the short term.

This doesn't mean you'll have no access to credit for a decade. But in the first few years, getting approved for a mortgage, a business loan, or even a competitive interest rate becomes noticeably harder. If buying a home or growing a business is part of your near-term plan, this timeline is something you need to seriously factor in before deciding to file.

Some Assets Could Be at Risk

Exemptions protect the essentials, but not everything you own is covered. If you have non-exempt assets like a second property, luxury items, high-value jewelry, or investment accounts the court-appointed trustee has the authority to sell those to repay your creditors.

This is especially worth thinking through if you've built up equity in a rental property or hold significant assets outside the basic exemption limits. Before filing, it's important to get a clear picture of what's protected in your state and what isn't because the "liquidation" part of this process is real, even if it rarely affects everyday belongings.

It Becomes Part of the Public Record

Bankruptcy filings are public records. The court doesn't broadcast your filing, but the information is searchable and in practice, landlords running background checks, certain employers, and lenders will be able to see it.

For many people, especially those in tight-knit communities where financial reputation carries social weight, the idea of this becoming known can feel like a heavy burden on top of an already stressful situation. It's worth acknowledging that fear honestly — while also recognizing that in most real-world cases, the filing stays largely invisible to your day-to-day social circle.

Not Every Debt Gets Erased

Chapter 7 doesn't wipe the slate completely clean for everyone. Certain debts are legally protected from discharge and will remain your responsibility even after the process is over. These include:

Student loans - rarely dischargeable without exceptional circumstances

Child support and alimony

Most recent unpaid income taxes

Debts tied to fraud or serious personal misconduct

If the bulk of what you owe falls into these categories, Chapter 7 may not deliver the full relief you're hoping for. Knowing exactly what will and won't go away is essential before you commit to this path.

Specific Considerations for the South Asian Community

A primary concern for many South Asian residents is how bankruptcy might affect their legal standing in the U.S., particularly for those on H1-B visas or those applying for a Green Card. There is a common myth that filing for bankruptcy will label you a "public charge," leading to visa denials or deportation. This is incorrect. Bankruptcy is a civil legal process, not a criminal one, and the "public charge" rule typically refers to the use of specific government welfare programs, not the legal elimination of debt. In fact, U.S. law prevents the government from discriminating against individuals solely because they filed for bankruptcy. While it is always wise to consult an immigration attorney if your case involves fraud or criminal issues, a standard Chapter 7 filing should not hinder your path to citizenship or your ability to renew your visa.

Assets Held Abroad

Many South Asian families maintain financial ties to their home countries, such as owning a family home in India, land in Pakistan, or bank accounts in Bangladesh. When you file for Chapter 7 in the U.S., you are legally required to disclose all assets, regardless of where they are located in the world. The U.S. bankruptcy court technically has jurisdiction over your global property. While it is more difficult for a U.S. trustee to seize and sell a physical house in another country, failing to disclose it can lead to a charge of perjury or the dismissal of your case. An experienced attorney can help you determine if your foreign assets can be protected through "exemptions" or if the cost of the court pursuing those assets outweighs their value, often allowing you to keep them.

Remittances and Family Support

Sending money home to support elderly parents or family members is a standard responsibility for many in the diaspora. However, during the months leading up to a bankruptcy filing, large or frequent "remittances" can be flagged as "preferential transfers" or "fraudulent transfers" by a trustee. Essentially, the court wants to ensure you aren't sending money to relatives to hide it from your creditors. If you are planning to file Chapter 7, you may need to temporarily pause or significantly reduce these payments to avoid legal complications. Once your case is discharged and your debts are wiped away, you will have more disposable income to resume supporting your loved ones without the burden of U.S. debt hanging over your head.

Chapter 7 vs. Alternatives: Is it Right for You?

Debt Management Plans (DMP)

A Debt Management Plan is a structured way to pay off your debt without filing for bankruptcy. You work with a non-profit credit counseling agency that negotiates with your creditors to lower your interest rates or waive late fees. You make one monthly payment to the agency, and they distribute the funds to your creditors. This is an excellent option if you have a steady income and can afford to pay back the full amount of your debt over three to five years. Unlike Chapter 7, a DMP does not wipe away your debt, but it helps you pay it off faster and cheaper while avoiding the long-term credit damage of a bankruptcy filing.

Chapter 13 Reorganization

If you earn too much money to qualify for Chapter 7, or if you are behind on your mortgage and want to prevent the bank from taking your home, Chapter 13 may be the better choice. Instead of liquidating assets, you create a court-approved plan to pay back a portion of your debt over three to five years. This is often called a "wage earner’s plan." It is particularly useful for families who want to keep non-exempt property like a family business or a second vehicle while still receiving legal protection from creditors and eventually discharging whatever debt remains at the end of the plan.

Debt Settlement

Debt settlement involves negotiate with creditors to pay a lump sum that is less than the total amount you owe. While this sounds appealing, it carries significant risks, especially when using "for-profit" companies. These companies often advise you to stop making payments to your creditors, which can lead to lawsuits and a destroyed credit score. There is also no guarantee that a creditor will agree to settle. Furthermore, the IRS may treat the "forgiven" portion of your debt as taxable income. For many South Asian families, the unpredictability of debt settlement can create more stress and financial instability than the structured, legal relief provided by Chapter 7.

Step-by-Step: The Filing Process in the USA

Filing for Chapter 7 bankruptcy is a structured legal process that requires strict adherence to federal rules and timelines. To successfully navigate a "fresh start" in the USA, follow these essential steps:

Complete Pre-Filing Credit Counseling: Before you can file any paperwork with the court, you must complete a counseling session with an agency approved by the U.S. Trustee Program. This session must occur within the 180 days before you file.

File the Bankruptcy Petition: Your attorney (or you, if filing alone) submits a series of detailed forms to the bankruptcy court. These forms disclose your income, expenses, assets, and every person or company you owe money to.

The Automatic Stay: Once filed, the court issues an "automatic stay," which legally prevents creditors from calling you, suing you, or garnishing your wages.

The Meeting of Creditors (341 Meeting): About a month after filing, you will attend a meeting with your court-appointed trustee. You will answer questions under oath about your financial documents. While creditors can attend, they rarely do.

Complete a Financial Management Course: After your case is filed but before your debt is officially erased, you must complete a second course on personal financial management. This "Debtor Education" course teaches you how to budget and manage credit moving forward.

Receive Your Discharge: Usually, about 60 to 90 days after your 341 meeting, the court will issue a discharge order. This officially wipes out your eligible debts, and your case is closed.

Mandatory Education Requirements

The U.S. government requires these two courses: Credit Counseling (pre-filing) and Debtor Education (post-filing) to ensure you understand your options and have the tools to stay debt-free in the future. Both can typically be completed online or over the phone in about two hours. Failing to file the completion certificates for these courses will result in the court dismissing your case without wiping away your debt.

Expert Tips for Rebuilding After Bankruptcy

Recovery begins the moment your discharge is granted. To rebuild your credit, start with a "credit mix" that shows you can handle different types of debt. A common first step is applying for a secured credit card. You provide a cash deposit that serves as your credit limit, making it a low-risk tool for banks. Using this card for small, monthly expenses and paying the balance in full ensures you are building a positive payment history. You might also consider a credit-builder loan from a local credit union, where your payments are held in a savings account until the loan is paid off, effectively demonstrating your reliability to credit bureaus.

If homeownership is part of your future plan, the timeline depends on the type of loan you seek. For a government-backed FHA loan, the standard waiting period is two years from your discharge date. In cases of extreme hardship beyond your control, this can sometimes be shortened to 12 months. For a conventional loan (backed by Fannie Mae or Freddie Mac), the wait is typically longer, requiring four years after your discharge. During this time, maintaining a clean record with no new late payments is essential to prove to lenders that you have established a stable financial lifestyle in the USA.

Conclusion: Empowerment Over Embarrassment

Choosing to file for Chapter 7 bankruptcy is a significant decision that involves weighing clear trade-offs. On one hand, you gain the immediate relief of the automatic stay and the life-changing ability to wipe out high-interest credit card debt and medical bills. On the other hand, you must accept a temporary impact on your credit score and the potential loss of non-essential assets.

In the South Asian community, the emotional weight of this decision can often feel heavier than the financial one. However, it is vital to view bankruptcy not as a failure, but as a legal tool designed specifically to help families regain their footing and contribute to the economy once again. Because every family’s financial situation and immigration status is unique, you should not navigate this path alone. Consulting with a qualified bankruptcy attorney is the best way to ensure your assets are protected and that you are making the most informed choice for your family's future in the USA.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

Do Debt Relief Programs Work?

11 min read

Filing For Business Bankruptcy? You Need To Know This First

10 min read

Is Bankruptcy Discharge Public Record?

9 min read

Debt Settlement- The Best Way To Avoid A Lawsuit

10 min read

Bankruptcy: What Are The Three Main Types?

13 min read

How to Settle Debt With Bank of America in 2026

10 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- Do Debt Relief Programs Work?

11 min read

- Filing For Business Bankruptcy? You Need To Know This First

10 min read

- Is Bankruptcy Discharge Public Record?

9 min read

- Debt Settlement- The Best Way To Avoid A Lawsuit

10 min read