Filing For Business Bankruptcy? You Need To Know This First

If your business is drowning in debt and you've started quietly Googling "business bankruptcy" late at night after everyone else has gone to sleep, you're not alone. For a lot of South Asian families in the US, the business isn't just a business, it's the reason you moved here, the thing that put your kids through college, the pride you carry at every family gathering. So even thinking about bankruptcy can feel like admitting defeat in front of your whole community.

Bankruptcy is not a moral failure. It's a legal process, built into US law, designed to give struggling business owners a real second chance. Thousands of honest, hardworking people use it every year restaurant owners, motel operators, truckers, shop owners, IT consultants to stop the bleeding and start over.

What Does It Mean to File for Business Bankruptcy?

Filing for business bankruptcy means asking a federal court to either wipe out your business debts or help you restructure them into a payment plan you can actually afford. It's a legal reset button, not a punishment.

It's different from personal bankruptcy, which deals with your individual debts, credit cards, medical bills, and personal loans. Business bankruptcy deals with debts tied to your company.

Which type of bankruptcy makes sense for you depends heavily on how your business is legally set up. A sole proprietorship (where there's no legal separation between you and the business), an LLC, a corporation, and a partnership are all treated differently under bankruptcy law. This is one of the first things a bankruptcy attorney will ask you, so it helps to know your business structure before you even walk into that first consultation.

The Main Types of Business Bankruptcy in the US

There isn't just one kind of "business bankruptcy" there are a few different paths, and each one leads somewhere very different. Some shut the business down completely. Others are built to help you keep the doors open while you get back on your feet.

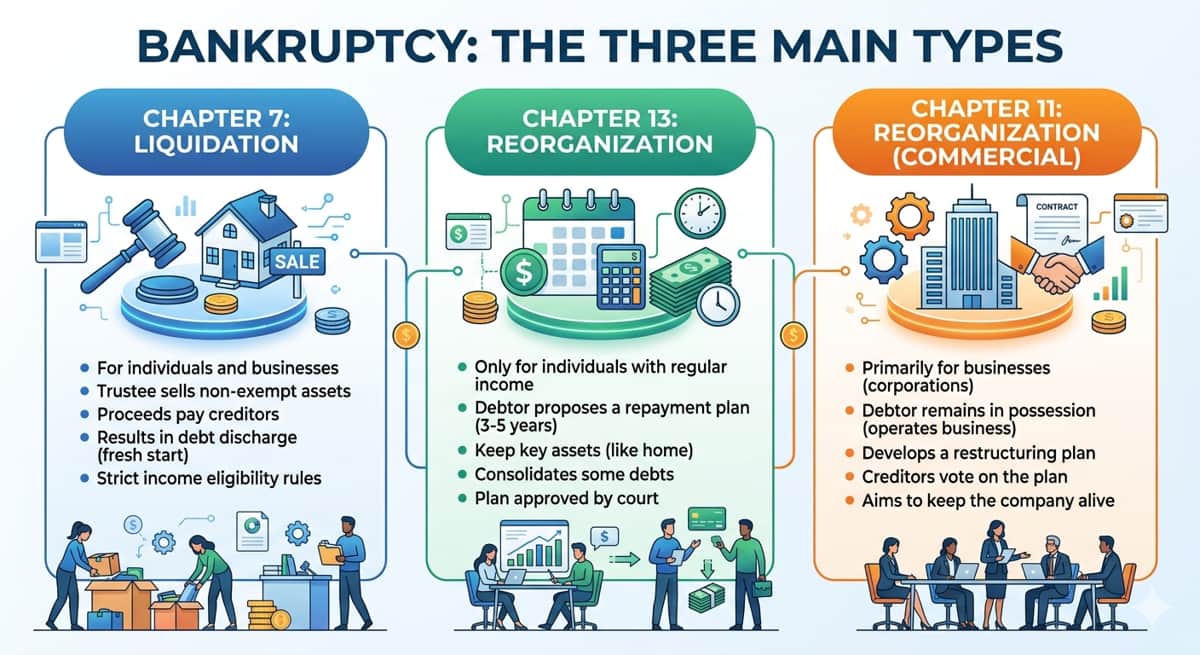

Chapter 7 - Liquidation

This is the "close it down option”. A court-appointed trustee sells off the business's assets inventory, equipment, property and uses that money to pay off creditors. Once that process is done, most remaining business debts are wiped clean. This is usually the route for businesses that simply can't be saved and the owner is ready to move on.

Chapter 11 - Reorganization

This is the option for business owners who still believe in their business and want to keep it running. Instead of selling everything off, you work out a repayment plan with creditors, often paying back a portion of what you owe over several years while the business stays open. It's more complex and more expensive than Chapter 7, which is why it's typically used by larger businesses though smaller businesses can use it too.

Subchapter V - A Faster, Cheaper Option for Small Businesses

If you run a small or family business, this one matters a lot. Subchapter V is a simplified version of Chapter 11, created specifically for small businesses under a certain debt limit. It's faster, less expensive, and easier to manage than a traditional Chapter 11 case which makes it a realistic option for a lot of South Asian-owned small businesses like retail stores, restaurants, and service businesses.

Chapter 13 - For Sole Proprietors

If you run your business as a sole proprietor, meaning there's no legal line between you and the business, your business debt is treated the same as your personal debt. In that case, Chapter 13 lets you set up a manageable repayment plan over three to five years while keeping your business and personal assets.

Are You Personally Liable for Your Business Debts?

This is usually the first question on every business owner's mind, and the honest answer is: it depends.

If your business is a sole proprietorship or a general partnership, there's no legal wall between you and your business. That means your personal assets, your house, your car, your savings could be at risk if the business can't pay its debts.

If your business is an LLC or a corporation, there's supposed to be a legal separation, called "limited liability," that protects your personal assets. But here's the catch a lot of small business owners don't realize until it's too late: if you personally guaranteed a business loan, a lease, or a line of credit (which is extremely common for newer businesses that don't yet have their own credit history), that personal guarantee LLC or a corporation can override the protection your LLC would normally give you.

And if you're married and co-own the business with your spouse, depending on your state's laws around community property, your spouse's assets could be affected too, even if their name isn't directly on the loan.personal guarantee

This is exactly why reviewing every loan, lease, and credit agreement your business has signed and checking for your personal signature on any of them is one of the most important early steps.

Will Filing for Bankruptcy Affect Your Immigration Status or Visa?

This is often the biggest, most private fear for immigrant business owners, and it deserves a straight answer: filing for business bankruptcy is not, by itself, a reason for deportation or visa denial. Bankruptcy is a financial and legal process, not a criminal one, and simply filing does not automatically put your immigration status at risk.

That said, there are situations where it's worth being extra careful:

If your visa (E-2 investor visa) is directly tied to owning and actively running that specific business, closing it could affect your visa status separately from the bankruptcy itself.

If you're in the middle of a green card process where your finances or business ownership are part of your application, it's worth understanding how that timing lines up.

"Public charge" rules, which look at whether someone might rely heavily on certain government benefits, are a separate consideration from business bankruptcy, but if you're unsure how it applies to you, it's worth asking directly.

Because this overlaps two very different areas of law, this is one of the few situations where it genuinely helps to bring in both a bankruptcy attorney and an immigration attorney before you file, not after.

How Business Bankruptcy Impacts Your Personal and Business Credit

Bankruptcy will affect your credit, but how much and for how long depends on a few things.

If the bankruptcy is tied to your personal credit (your Social Security number), it can stay on your credit report for up to 10 years for Chapter 7, or around 7 years for Chapter 13. If it's strictly a business bankruptcy tied to your business's EIN and hasn't touched your personal guarantees, your personal credit may be affected far less.

In practical terms, this can make it harder for a while to get approved for new business loans, favorable vendor payment terms, or a commercial lease. It's not permanent, and many business owners rebuild their credit steadily over the years that follow but it's realistic to expect a rocky stretch, especially in the first year or two.

Alternatives to Filing for Business Bankruptcy

Bankruptcy isn't the only way to deal with serious business debt. Depending on how much you owe and how your creditors are willing to work with you, one of these paths might get you out of trouble without ever going to court.

Debt Consolidation & Refinancing

Rolling multiple debts into a single loan, ideally with a lower interest rate, can simplify your payments and reduce what you owe each month.

Debt Settlement or Negotiation

Sometimes creditors would rather accept a smaller lump-sum payment than risk getting nothing in a bankruptcy case. Negotiating directly (or through a professional) can settle debts for less than the full amount owed.

Out-of-Court Workouts & Forbearance

This means working directly with your lenders to temporarily pause or reduce payments while your business gets back on stable footing, without involving the courts at all.

Nonprofit Credit Counseling

Agencies affiliated with the NFCC offer low-cost, sometimes free guidance and can help set up a structured debt management plan. This is a good first stop if you're not sure bankruptcy is even necessary yet.

Cultural and Family Considerations for South Asian Business Owners

Let's be honest about something most financial articles won't say out loud: for many South Asian families, a struggling business isn't just a financial issue, it's a family issue. Parents worry about what relatives will say. Adult children worry about disappointing parents who sacrificed a lot to build the business. Sometimes an entire extended family has money tied up in it, formally or informally.

That weight is real, and it's okay to feel it. But try to separate two things that often get tangled together: what your family and community might think, and what is actually the smartest financial move for your future. Making a bankruptcy decision based on fear of judgment, instead of based on the facts of your situation, often leads to more financial pain down the road, not less.

It also helps to be careful about where you get advice. Well-meaning relatives, community elders, or "a friend who went through something similar" can offer emotional support, but they're not a substitute for a licensed attorney who actually knows bankruptcy law and your specific numbers. This is a decision worth getting professional eyes on, even if it feels more private to keep it within the family.

Steps to Take Before You File

Before you make any final decision, here's a practical order of operations:

Talk to a licensed bankruptcy attorney. Most offer an initial consultation, and this conversation alone can clarify a lot.

Gather your financial and business records tax returns, loan agreements, leases, and a list of everything you owe and everything you own.

Understand the means test, which determines which type of bankruptcy you may qualify for.

Review every loan and lease for your personal signature, so you know exactly what you're personally on the hook for.

Talk to a tax professional, since certain tax debts follow different rules than other business debts.

If you're on a visa or in the middle of an immigration process, loop in an immigration attorney before you file, not after.

Your First Next Steps: How to Prepare For a Consultation

Taking the first step toward a bankruptcy consultation can feel incredibly daunting, but walking into an attorney’s office prepared will instantly give you back a sense of control. Think of this meeting as a safe space to map out your survival strategy. To get the most out of your consultation, you will want to gather a clear picture of your business finances.

Start compiling your essential paperwork: your last two to three years of corporate tax returns, active commercial leases, copies of any personal guarantee riders you signed with lenders, and an itemized log of everything you owe.

Most importantly, please remember this crucial rule: never try to transfer business funds, hide assets, or move money into a family member’s bank account to protect it right before you file. The legal system looks closely at these sudden movements, and it can be flagged as fraud which does far more damage than the bankruptcy itself. Be entirely transparent with your attorney; their job is to protect you, your family, and your future.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Related Articles

Is Bankruptcy Discharge Public Record?

9 min read

Bankruptcy: What Are The Three Main Types?

13 min read

Converting Chapter 13 To Chapter 7: What You Should Know

10 min read

The Pros And Cons Of Filing Chapter 7 Bankruptcy

14 min read

How Bankruptcy Affects Your Credit Score And How Long It Lasts

12 min read

7 Reasons Chapter 13 Bankruptcy Is A Bad Idea

17 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation