Bankruptcy: What Are The Three Main Types?

The three main types of bankruptcy in the United States are Chapter 7, Chapter 13, and Chapter 11. Each one works differently, and the right fit depends on your income, your assets, and what you're trying to protect.

If you're reading this, there's a good chance money has been weighing on you for a while. In many South Asian households, financial trouble is something people quietly carry alone, often hiding it from parents, in-laws, or the wider community out of fear of judgment. That instinct is understandable, but it isn't necessary here. Bankruptcy is a private legal process handled in federal court. It is not announced to your neighbors, your relatives back home, or your local community. It exists specifically to give people a real, legal way out of debt that has become unmanageable not as a punishment, but as a tool.

What Is Bankruptcy and How Does It Work?

Bankruptcy is a legal process, set up under federal law, that lets a person or a business get relief from debts they can't pay. It's handled in federal bankruptcy court not your local state court and it follows the same rules no matter which state you live in.

Once you file, something called an "automatic stay" kicks in almost immediately. This is one of the most important parts of the process: by law, creditors and debt collectors have to stop calling you, stop sending letters, and stop trying to garnish your wages or take legal action against you. It happens the moment your case is filed, giving you breathing room while the court sorts out what comes next.

For anyone new to the U.S. legal system, it helps to know that this process is standardized and well-established. Bankruptcy courts handle these cases every single day, and many courts have interpreters available if English isn't your first language.

What Are the Three Main Types of Bankruptcy?

There are three main types of bankruptcy that individuals and businesses can file:

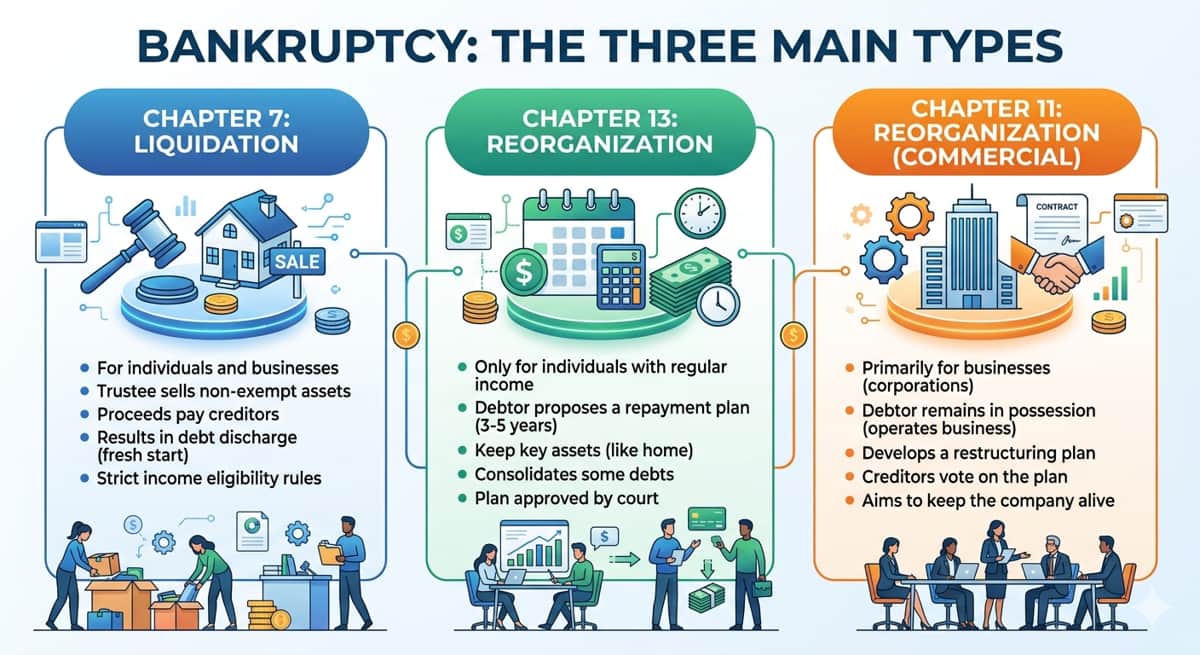

Chapter 7 – Known as liquidation. Certain assets may be sold to pay off debt, and most remaining unsecured debt is wiped out within a few months.

Chapter 13 – Known as a wage earner's plan. You keep your property and pay back debt over three to five years based on what you can afford.

Chapter 11 – Known as reorganization. Mainly used by businesses (and occasionally individuals with very high debt) to restructure what they owe while continuing to operate.

Each one is named after the chapter of the U.S. Bankruptcy Code it falls under. Here's a closer look at how each actually works.

Chapter 7 Bankruptcy (Liquidation)

Chapter 7 is often what people picture when they hear the word "bankruptcy." A court-appointed trustee reviews what you own, and if you have assets that aren't protected by law (called exemptions), those can be sold to pay your creditors. Most people who file Chapter 7, though, don't actually lose much. Many states allow you to keep essentials like a modest car, basic household items, and in some cases, a portion of home equity.

To qualify, you have to pass what's called a "means test," which compares your income to the median income in your state. If your income is below that threshold, you generally qualify. If it's above, you may still qualify depending on your expenses and debts.

The biggest appeal of Chapter 7 is speed. Most cases are resolved in about three to four months, and most unsecured debts, credit cards, medical bills, and personal loans are discharged completely. This makes it a common choice for people with limited income and few assets to protect.

Chapter 13 Bankruptcy (Repayment Plan)

Chapter 13 works very differently. Instead of selling off assets, you propose a repayment plan to the court usually lasting three to five years where you pay back some or all of your debts based on what you can realistically afford each month.

The biggest reason people choose Chapter 13 is to keep property they don't want to lose. This comes up a lot for South Asian families who own a home, or who run a small business like a motel, gas station, or retail store and can't afford to have it disrupted. If you're behind on your mortgage, Chapter 13 can also let you catch up on missed payments over time while you keep the house, instead of facing foreclosure.

Because it requires a steady, reliable income to make those monthly plan payments, Chapter 13 tends to fit people with a job or business income, rather than those with little to no income coming in.

Chapter 11 Bankruptcy (Reorganization)

Chapter 11 is mainly built for businesses, though in rare cases individuals with very large and complicated debts use it too. Instead of shutting down, the business keeps operating while it works out a court-approved plan to restructure what it owes, renegotiating with lenders, suppliers, and landlords along the way.

This matters more than people realize for South Asian entrepreneurs in the U.S., where ownership of franchise hotels, motels, gas stations, and convenience stores is especially common. If a family-run business is struggling under loan payments but is still fundamentally viable, Chapter 11 offers a way to restructure debt without closing the doors or losing the business entirely. It's a more complex and expensive process than Chapter 7 or 13, which is why it's typically reserved for businesses rather than everyday personal debt.

Chapter 7 vs. Chapter 13 vs. Chapter 11: Side-by-Side Comparison

Seeing these three side by side often makes the differences click faster than reading about them one at a time.

Chapter 7 | Chapter 13 | Chapter 11 | |

Who it's for | Individuals with low income, few assets | Individuals with steady income who want to keep property | Businesses (rarely individuals with very high debt) |

Eligibility | Must pass the means test | Must have regular income | No income limit; based on business viability |

Timeline | 3–4 months | 3–5 years | Can take a year or more |

What happens to assets | Non-exempt assets may be sold | You keep your property; pay a plan instead | Business keeps operating during reorganization |

Typical cost | Lower filing and attorney fees | Moderate; spread over the repayment period | Highest; legal and administrative fees are significant |

If you remember nothing else from this table, remember this: Chapter 7 trades some assets for a fast fresh start, Chapter 13 trades time for keeping what you own, and Chapter 11 is the business version of "restructure and keep running."

Which Type of Bankruptcy Should You Consider?

There's no single "best" type of bankruptcy; it really comes down to your income, what you own, and what you're trying to protect. A few common scenarios make this easier to picture:

If your income is low and you don't have many valuable assets, Chapter 7 often makes sense. It moves quickly and clears most unsecured debt without much to lose in the process.

If you have steady income and want to keep your home, car, or a small business running, Chapter 13 is usually the better fit. You give up speed in exchange for keeping what matters to you.

If you own a business that's struggling but still has a path forward, Chapter 11 allows you to keep operating while restructuring debt.

These are general starting points, not a diagnosis of your specific situation. Two people with similar debt can end up needing completely different solutions depending on their income, state exemptions, and goals which is exactly why talking to a licensed bankruptcy attorney before filing matters so much.

How Does Bankruptcy Affect Immigration Status or a Green Card Application?

This is one of the most common worries among South Asian immigrants, and it deserves a straightforward answer: filing bankruptcy is a civil financial matter, not a criminal one, and on its own, it does not affect your immigration status, your path to citizenship, or a green card application.

USCIS does not deny green cards or naturalization simply because someone filed for bankruptcy. That said, financial history can come up in specific contexts for example, if someone else is sponsoring you and needs to show they can financially support you (an Affidavit of Support), your financial picture could matter there. If you're navigating a visa, sponsorship, or any immigration process alongside a bankruptcy filing, it's worth speaking with an immigration attorney who can look at your specific circumstances, since immigration law and bankruptcy law are separate systems that don't always interact in obvious ways.

Will Filing Bankruptcy Affect My Family or Co-Signed Loans?

This question comes up a lot, and for good reason in many South Asian families, loans are rarely just one person's responsibility. A parent might co-sign a car loan, a sibling might back a business loan, or relatives might pool money to help someone through school.

Here's the important part: bankruptcy generally only protects the person who files it. If you file Chapter 7 and a debt is discharged, your co-signer can still be held responsible for what's owed, even though you no longer are. Chapter 13 offers a bit more protection for co-signers in some cases, since the debt may continue being paid through your repayment plan rather than discharged outright.

If a loan is shared with a family member, it's worth having an honest conversation with them before filing, and bringing this up directly with your attorney, since the details can shift depending on which chapter you file and which state you're in.

How Does Bankruptcy Affect a Small Business or Family-Owned Franchise?

Many South Asian families in the U.S. run small businesses, motels, gas stations, convenience stores, restaurants often built up over years of long hours and family labor. So this question carries real weight.

The key distinction is whether you file personally or whether the business itself files. If your business is a sole proprietorship, there's often no real separation; a personal Chapter 7 or Chapter 13 filing covers the business debt too. But if you've structured the business as an LLC or corporation, the business may need its own filing (often Chapter 11) separate from you personally.

One detail that catches people off guard: if you personally guarantee a business loan which banks almost always require for small business financing, that guarantee can pull your personal assets into the case even if the business itself files separately. This is exactly the kind of detail where sitting down with an attorney who understands both your business structure and your personal finances makes a real difference.

What Debts Can and Cannot Be Discharged in Bankruptcy?

Not all debt disappears in bankruptcy. Generally, debts fall into two groups:

Usually dischargeable (can be wiped out):

Credit card debt

Medical bills

Personal loans

Most older unpaid bills

Usually not dischargeable (you still owe these):

Most federal student loans (discharge is possible but requires meeting a very high legal standard)

Recent income tax debt

Child support and alimony

Most court fines and criminal penalties

This is one of the biggest misconceptions people have going in; many assume bankruptcy clears everything, and it doesn't. Knowing this upfront helps you set realistic expectations about what filing will actually change for you.

How Long Does Bankruptcy Stay on Your Credit Report?

A Chapter 7 bankruptcy can stay on your credit report for up to 10 years from the filing date. A Chapter 13 typically stays for up to 7 years, since it involves actually repaying some debt rather than wiping it out immediately.

That sounds discouraging, but it's not the full picture. Most people who file see their credit score start climbing again within a year or two, especially if they make on-time payments on whatever credit they still have and pick up a secured credit card or small auto loan to start rebuilding. The bankruptcy doesn't disappear from your report right away, but its actual impact on your day-to-day financial life fades much faster than the 7-to-10-year window makes it sound.

What Are the Alternatives to Filing Bankruptcy?

Bankruptcy isn't the only option, and for some people, it isn't the right one. A few common alternatives worth knowing about:

Credit counseling and debt management plans - Nonprofit credit counselors can negotiate lower interest rates and combine your payments into one manageable monthly amount, without going to court.

Debt settlement - Negotiating with creditors to pay a lump sum that's less than what you owe. This can hurt your credit similarly to bankruptcy and doesn't come with the same legal protections.

Family-funded payoff arrangements - It's common in South Asian communities for relatives to step in and help pay off debt directly. This can work, but it's worth being clear-eyed about whether it's truly sustainable or just delays a deeper problem.

None of these options pause collections the way the automatic stay in bankruptcy does, so if you're already facing wage garnishment or lawsuits, it's worth weighing that urgency against the slower pace of these alternatives.

How Do You File for Bankruptcy in the United States?

The process generally follows these steps:

Credit counseling course - Required before filing, usually a short online or phone session from an approved agency.

Means test (for Chapter 7) - Determines whether your income qualifies you.

Filing the petition - Your attorney files your case with the bankruptcy court, listing your debts, income, and assets.

Automatic stay begins - Collections and creditor contact stop immediately.

Meeting of creditors (341 meeting) - A short, fairly routine meeting where a trustee asks you questions about your finances. Creditors rarely show up.

Discharge - The court officially wipes out eligible debts (Chapter 7) or you complete your repayment plan (Chapter 13).

Attorney fees vary by location and case complexity, but many bankruptcy attorneys offer free initial consultations, and free or low-cost legal aid clinics exist in most cities for people who qualify based on income. Many bankruptcy courts also provide interpreter services, so language doesn't have to be a barrier to understanding your own case.

Getting Professional Help: Attorneys and Nonprofit Credit Counselors

Before you file anything, it's worth talking to a licensed bankruptcy attorney. Most state bar associations offer free attorney referral services, and many bankruptcy attorneys offer a free first consultation. If cost is a barrier, look for legal aid organizations in your area many offer free help to people who qualify based on income.

For more general guidance before deciding whether bankruptcy is even the right step, nonprofit credit counselors certified through the National Foundation for Credit Counseling (NFCC) are a reliable, low-cost starting point.

One more thing worth saying plainly: debt-relief scams disproportionately target immigrant communities, often promising to "settle" or "erase" debt for an upfront fee. Be cautious of anyone who guarantees results, asks for payment before doing any work, or pressures you to act immediately.

Conclusion

Chapter 7, Chapter 13, and Chapter 11 each offer a different path through debt: one fast and clean, one paced and protective of what you own, one built for businesses trying to stay open. None of them are a mark of failure. Debt is a financial problem with financial solutions, not a reflection of someone's character or worth, no matter what old narratives might suggest. If any of this feels relevant to where you are right now, the most useful next step is a conversation with a licensed bankruptcy attorney who can look at your actual numbers and help you figure out what fits.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

How Much Tax You Pay On Lawsuit Settlements

9 min read

Filing For Business Bankruptcy? You Need To Know This First

10 min read

Is Bankruptcy Discharge Public Record?

9 min read

Converting Chapter 13 To Chapter 7: What You Should Know

10 min read

The Pros And Cons Of Filing Chapter 7 Bankruptcy

14 min read

How Bankruptcy Affects Your Credit Score And How Long It Lasts

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation