Bankruptcy Chapters 7, 13 And 11 - What You Need To Know

In many South Asian communities, the pressure to achieve financial success is immense, and carrying debt or facing financial distress often comes with a significant burden of cultural pressure and intense social stigma. The concept of bankruptcy can feel like a deep personal failure, making it incredibly difficult to discuss or seek help for. This environment of shame can prevent families from making timely, responsible decisions to secure their financial futures.

We understand these unique challenges. As experienced professionals in debt relief and financial management, our goal is to cut through the stigma and provide unbiased, expert guidance on US bankruptcy law. This article serves as a trusted resource to demystify Chapters 7, 13, and 11, giving you the knowledge needed to make a sound financial choice. Our core thesis is simple: Bankruptcy is not a moral failure; it is a powerful legal tool enshrined in U.S. law, designed to provide responsible individuals and families with a necessary fresh start and a path back to financial stability.

Why Understanding US Bankruptcy Law is a Critical Financial Decision

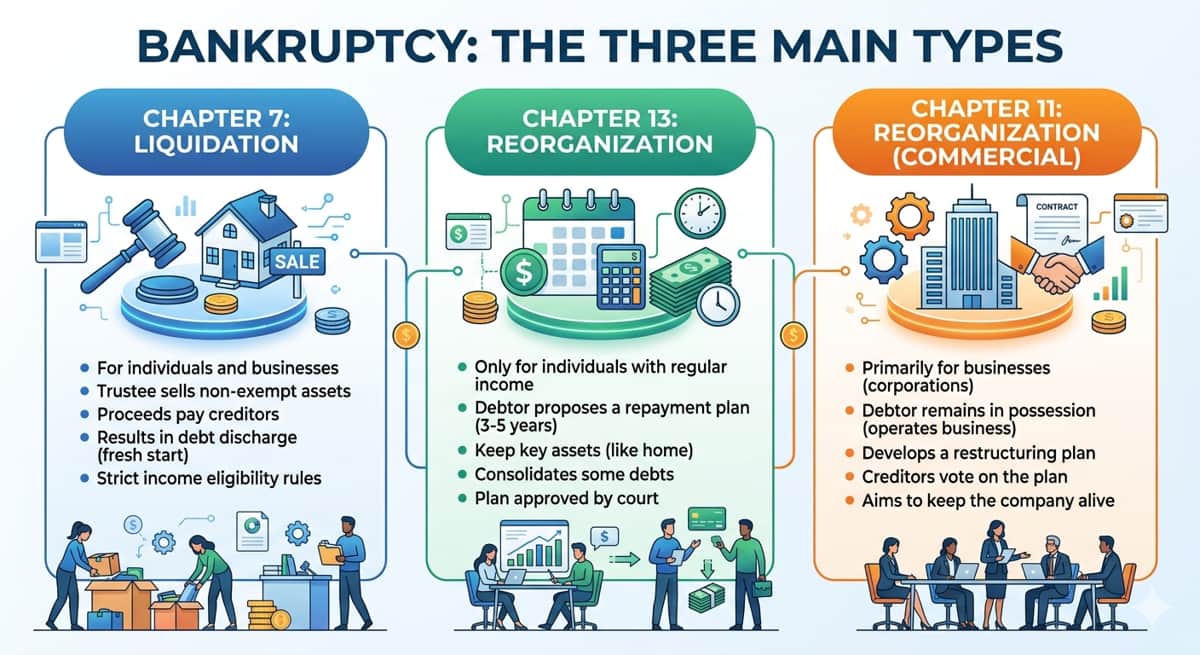

Understanding U.S. bankruptcy law is one of the most significant financial decisions you may ever face. It is a powerful federal process designed to give individuals and businesses a chance to resolve overwhelming debt.1 Broadly, this process leads to one of two outcomes:

Liquidation (Chapter 7): Selling non-exempt assets to pay creditors, resulting in a quick discharge of most debts.

Reorganization (Chapter 13 and Chapter 11): Creating a structured payment plan to repay debts over time while often allowing you to retain valuable assets.

Because bankruptcy has long-lasting effects on your credit, assets, and future financial life, it is a high-stakes matter requiring absolute precision. Accuracy and professional advice are non-negotiable. This is not a time for guesswork. By understanding the core mechanisms of Chapter 7, Chapter 13, and, in certain cases, Chapter 11, you position yourself to make a financially sound decision rather than an emotionally driven one.

Deep Dive into Chapter 7 Bankruptcy: The Liquidation Path

Chapter 7, often referred to as "liquidation" bankruptcy, is designed for debtors who truly cannot afford to repay their outstanding debts. It is the quickest path to eliminating unsecured debt and achieving a financial fresh start.

Eligibility and the Mandatory "Means Test"

To qualify for Chapter 7, you must demonstrate that your income is low enough to make repayment impossible. This is determined by the Means Test a crucial part of the process.

The Means Test compares your average income over the past six months to the median income for a household of your size in your state.2 If your income falls below the state median, you automatically qualify. If it is above the median, the test proceeds to analyze your necessary living expenses to determine if you have enough disposable income to feasibly fund a Chapter 13 repayment plan. The U.S. Trustee—a representative of the Department of Justice—oversees this process and is tasked with administering the bankruptcy case fairly.

How Assets and Debt Are Handled (Exemptions)

When you file for Chapter 7, a trustee is appointed to review your assets.4 The term "liquidation" is often frightening, but it’s important to understand the concept of exemptions.

Federal and state laws allow you to protect certain properties—called exempt assets—from being sold.5 For example, the homestead exemption protects a specific amount of equity in your primary residence, and other exemptions protect necessary items like household goods, basic vehicles, and retirement funds.6 Only non-exempt assets (like a second home, expensive jewelry, or excess cash) can be sold by the trustee to pay creditors.

Pros and Cons: When Chapter 7 is the Best Fresh Start

Pros:

Quick Discharge: The process typically takes only four to six months from filing to debt discharge.

Comprehensive Relief: It eliminates most unsecured debts including credit card balances, medical bills, and personal loans.

Immediate Protection: The filing immediately triggers an "automatic stay," halting creditor calls, lawsuits, and most collection activities.

Cons:

Asset Risk: There is a risk of losing any non-exempt assets, which is why a thorough exemption analysis by an attorney is vital.

No Solution for Foreclosure: While the automatic stay halts foreclosure temporarily, Chapter 7 does not provide a mechanism to catch up on missed mortgage payments, meaning the loss of the property is often unavoidable without another plan.

Deep Dive into Chapter 13 Bankruptcy: The Reorganization Path

Chapter 13, often called "reorganization" or "wage earner’s" bankruptcy, is designed for individuals who have a steady income but need time to restructure their debts and catch up on payments.1 Unlike Chapter 7, Chapter 13 focuses on repayment over elimination.

Who Qualifies: Secured Debt Limits and Income Requirements

Chapter 13 is often necessary for individuals who fail the Chapter 7 Means Test because their income is too high, or for those who possess significant assets they wish to protect. To qualify you must have regular income and your debt levels must not exceed statutorily defined limits for both secured debt (like mortgages and car loans) and unsecured debt (like credit cards). If you possess significant assets, Chapter 13 provides a structured way to keep them while meeting your obligations.

Developing the 3-to-5 Year Repayment Plan

The core of Chapter 13 is the repayment plan. This is a detailed proposal outlining how you will repay certain creditors over a three- to five-year period.4 The plan length is usually five years if your income is above your state’s median.

The plan must satisfy the "best interest of creditors" test, meaning unsecured creditors must receive at least as much as they would have received if you had filed for Chapter 7. This plan dictates monthly payments to the Chapter 13 Trustee, which are then distributed to your creditors.6 In certain cases, you may utilize a "cramdown," a legal mechanism that allows you to reduce the principal balance of certain secured loans (often vehicle loans) to the actual fair market value of the collateral.

Key Advantages: Saving a Home and Vehicle

The primary benefit of filing Chapter 13 is the ability to retain valuable secured assets, such as your home or car. If you have fallen behind on your mortgage or vehicle payments, Chapter 13 allows you to:

Stop Foreclosure/Repossession: The automatic stay halts collection efforts, including foreclosure actions.

Cure Arrearages: You can pay the total amount of your missed payments (arrearages) over the life of the plan, effectively getting back on track with your original loan terms.

The Role of the Chapter 13 Trustee

The Chapter 13 Trustee acts as a fiduciary intermediary. They are responsible for reviewing and challenging your proposed repayment plan, collecting your monthly payments, and distributing the funds to your creditors.9 The Trustee also holds mandatory meetings with you and your creditors.10 They are central to ensuring the plan is fair, feasible, and legally compliant throughout the entire three-to-five-year period.

Deep Dive into Chapter 11 Bankruptcy: Reorganizing High-Value Assets

Chapter 11 for Businesses vs. Individuals

While Chapter 7 and Chapter 13 are the most common filings for consumers, Chapter 11 is traditionally the primary tool for large corporations seeking financial restructuring. However, it is an essential option for high-net-worth individuals whose secured or unsecured debt totals exceed the limits set for Chapter 13. When consumer debt is too high for Chapter 13, Chapter 11 provides the necessary legal framework to reorganize finances and secure high-value assets.

The Complexities of Chapter 11 for Individual Debtors

Filing Chapter 11 is significantly more complex, time-consuming, and expensive than either Chapter 7 or Chapter 13.1 The process involves extensive disclosure, reporting requirements, and the creation of a detailed, court-approved disclosure statement and plan of reorganization. Due to the high administrative costs and complexity, it is typically reserved only for those whose financial circumstances strictly prohibit filing under the more streamlined consumer chapters.

The Decision-Making Matrix: Choosing the Right Chapter

Selecting the appropriate bankruptcy chapter is the most crucial step and depends entirely on your specific financial goals. Your choice dictates your eligibility, your required payments, and the fate of your assets.

Comparative Analysis: Chapter 7 vs. Chapter 13

The fundamental differences can be summarized as follows:

Feature | Chapter 7 (Liquidation) | Chapter 13 (Reorganization) |

Eligibility | Must pass the Means Test (low income). | Must have regular income and be within debt limits. |

Asset Retention | Only exempt assets are protected (risk of loss). | You keep all assets; use payment plan to catch up on secured debt. |

Discharge Timeline | Quick (4–6 months). | Long (3–5 years). |

Goal | Eliminate unsecured debt immediately. | Restructure debt and cure missed payments. |

Key Factors Influencing the Choice

To make an informed decision, you and your attorney must carefully review several key financial factors:

Disposable Income: If you have significant discretionary income, you will be ineligible for Chapter 7 and must file Chapter 13.

Asset Ownership: If you own a home or vehicle with substantial, non-exempt equity that you want to keep, Chapter 13 is the necessary route.

Previous Bankruptcy History: There are waiting periods between filings. For example, if you received a Chapter 7 discharge recently, you cannot file Chapter 7 again but may be able to file Chapter 13.

Tax Debts: Certain priority tax debts can be repaid interest-free through a Chapter 13 plan, a key advantage over Chapter 7.

Critical Financial and Cultural Nuances for South Asian Residents

For South Asian residents in the U.S., debt relief is rarely a purely financial decision; it involves unique cultural and legal complexities that must be addressed by an experienced professional.

Immigration Status Implications

A frequent and critical concern is whether filing for bankruptcy will jeopardize your immigration status, such as your Green Card application, H-1B, or other visa renewals. The general legal consensus is that filing for Chapter 7 or Chapter 13 bankruptcy does not affect your immigration status or future applications, as bankruptcy is a civil financial remedy and not a criminal or immigration offense. However, given the high stakes involved, this must always be confirmed directly with your qualified bankruptcy attorney, particularly if any debt involves government entities.

Protecting Overseas Assets and Family Loans

The U.S. bankruptcy court takes a comprehensive view of a debtor’s global finances. Assets held in home countries (like real estate in India, Pakistan, or Bangladesh) must be disclosed to the bankruptcy trustee. While the trustee's jurisdiction to seize and liquidate foreign property is limited and complex, non-disclosure is illegal and can lead to the dismissal of your case or criminal charges. Additionally, co-signed family loans (debts where a relative is also legally liable) add complexity, as the bankruptcy discharge does not remove the liability from the co-signer.

The Role of a Culturally Competent Advisor

A legal professional who understands both U.S. bankruptcy law and the unique financial structures and cultural sensitivities of the South Asian diaspora is invaluable. They can help navigate asset disclosure, explain the impact on family members, and address the cultural stigma with sensitivity and expertise.

Establishing Trust: What to Look for in a Financial Expert

The Absolute Necessity of a Licensed Bankruptcy Attorney

Given the life-altering nature of bankruptcy, relying on non-legal advice or generalized information is extremely risky. Filing for bankruptcy involves complex federal statutes, local court rules, and strict timelines. You must engage a licensed bankruptcy attorney who practices actively in your jurisdiction. They are the only professionals qualified to evaluate your assets, perform the Means Test accurately, advise on exemptions, and represent you in court. This is not a process suitable for self-filing.

Three Questions to Ask Your Potential Attorney

To ensure you are working with an experienced and trustworthy professional, ask:

"How many Chapter 7 and Chapter 13 cases have you filed in this district in the last year?"

"Do you primarily represent debtors (individuals) or creditors (banks)?"

"Based on my circumstances, what are the three most critical risks you see in my case?"

Conclusion: Taking the First Step Toward Financial Freedom

Navigating the complexities of Chapters 7, 13, and 11 can be challenging, but understanding the differences empowers you to make an informed choice about your financial future. Bankruptcy, far from being an endpoint, is a powerful protection mechanism offered by federal law, providing a structured, legal pathway to manage debt and start anew. Whether you need the quick relief of Chapter 7 or the asset protection of Chapter 13, the goal remains the same: eliminating stress and rebuilding security. Do not allow fear or cultural stigma to delay necessary action. Your next, most important step is to immediately consult with a qualified, licensed bankruptcy attorney who can analyze your specific situation and guide you toward lasting financial freedom.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Related Articles

Filing For Business Bankruptcy? You Need To Know This First

10 min read

Is Bankruptcy Discharge Public Record?

9 min read

Bankruptcy: What Are The Three Main Types?

13 min read

Converting Chapter 13 To Chapter 7: What You Should Know

10 min read

The Pros And Cons Of Filing Chapter 7 Bankruptcy

14 min read

How Bankruptcy Affects Your Credit Score And How Long It Lasts

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation