Veteran Debt Relief | Effective Military Debt Solutions

If you served in the military and now feel like your bills are winning, you are not alone, and you are not failing. Veteran debt relief simply means the programs, legal protections, and practical strategies built specifically to help service members, veterans, and their families bring debt back under control. Research on veteran households has found something many people don't expect: veterans actually carry more credit card debt and report more money stress than civilians with the exact same income, age, and background. For South Asian veteran and military families in the U.S., there is often a second layer on top of that a quiet rule that money problems stay inside the family, plus real financial responsibilities to parents or relatives back home or nearby.

What Is Veteran Debt Relief?

Veteran debt relief is the set of programs, legal protections, and repayment strategies designed specifically to help service members, veterans, and their families reduce, restructure, or manage debt. It's different from generic "debt relief" you'll see advertised everywhere, because it includes protections that only apply to people connected to the military things like interest rate caps under the Servicemembers Civil Relief Act (SCRA), lending limits under the Military Lending Act (MLA), and hardship programs run through the VA.

You'll often see "military debt solutions" and "veteran debt relief" used as if they mean the same thing, but there's a useful distinction. Some protections (like the SCRA interest rate cap) are tied to active-duty status and mostly apply while you're serving or for a short period after. Others like nonprofit credit counseling, debt consolidation, or VA benefit overpayment plans apply just as much to veterans years after they've left service.

Why Do So Many Veterans and Military Families Struggle With Debt?

Veterans are statistically more likely than civilians to carry credit card debt and rely on costly credit options like payday or pawnshop loans, even when researchers control for income, age, and education. That's not a character flaw, it's a pattern with clear causes rooted in how military life actually works.

A few of the biggest drivers:

Frequent moves (PCS). Every move comes with upfront costs, deposits, travel, replacing things that don't survive the move often before reimbursement arrives.

Deployment income gaps. Special pays and allowances can shift or disappear depending on deployment status, which makes budgeting unpredictable even for disciplined savers.

The shift to civilian pay. Leaving service often means losing housing allowances, health coverage, and steady paychecks all at once, right when job-hunting expenses are highest.

Limited hands-on financial training during service. Many service members get classroom-style financial briefings but little real practice managing a full civilian budget before they're suddenly doing it on their own.

Family separation costs. Maintaining two households, travel for reunions, or supporting a spouse managing things solo all add real, recurring expenses.

If money stress ever starts to feel like more than you can carry especially if it's affecting how you're feeling day to day please know support exists beyond financial fixes too. The Veterans Crisis Line (dial 988, then press 1) is free, confidential, and available right now, any time, day or night.

How Military Life Cycle Events Create Debt

Three moments tend to create the most financial strain, back to back:

PCS orders - moving costs hit before reimbursements land, often forcing a credit card balance that lingers for months.

Deployment - pay and routines change quickly, and family budgets back home don't always adjust in time.

Separation from service - the loss of steady military pay and benefits collides with job-search costs and moving expenses, all in the same few months.

How Is Debt Different for South Asian Veteran and Military Families in the U.S.?

South Asian military families deal with the same debt triggers as anyone else in the service: PCS moves, deployment gaps, the shock of civilian pay but two extra layers often make things harder. The first is cultural: many South Asian households were raised with a strong, often unspoken rule that financial struggle stays private, even from close friends. The second is structural: ongoing financial support to parents, in-laws, or extended family whether that's a monthly remittance abroad or covering costs for relatives living nearby is a real, recurring budget line that most generic debt calculators and advice columns completely ignore.

If you've grown up hearing that debt reflects badly on your family's name or your own discipline, it makes sense that asking for help can feel uncomfortable. But here's a reframe worth sitting with: using a legitimate, free counseling service to organize your finances is not a failure, it's the same kind of practical, informed decision-making your family probably valued in every other area of life. Plenty of financially successful people, including many who built wealth specifically by being careful with money, have used professional debt counseling at some point. It's a tool, not a verdict.

A few access barriers worth naming honestly:

Language comfort. Some financial documents and call centers can be harder to navigate if English isn't your first or most comfortable language and ask if interpretation services are available, because many nonprofit counseling lines offer them.

Trust in unfamiliar institutions. It's natural to prefer advice from someone you know personally over a stranger on the phone. That instinct is good just to make sure the "someone you know" giving financial advice actually has the training to back it up, because debt strategy mistakes can be expensive to undo.

Family-network advice as a first stop. This is often genuinely useful for everyday money habits, but specific tools like SCRA interest caps or DMP enrollment require speaking with the right institution directly. Family advice can point you in the right direction, but it can't file the paperwork for you.

What Legal Protections Help Veterans and Service Members With Debt?

Two federal laws form the backbone of military debt protection: the Servicemembers Civil Relief Act (SCRA) and the Military Lending Act (MLA). Both exist specifically because military life creates financial vulnerabilities that civilian consumer law doesn't fully address.

Servicemembers Civil Relief Act (SCRA): Interest Rate Caps and Protections

The SCRA caps interest at 6% on most debts you took on before you entered active duty credit cards, auto loans, personal loans, even certain mortgages. This protection isn't automatic. You have to request it in writing from each lender, include a copy of your military orders, and do it no later than 180 days after leaving active duty. For most debts, the lower rate applies only during your active-duty period; for mortgages specifically, the 6% cap continues for one full year after your service ends. It's worth noting this protection is tied to active-duty status, so if you're a veteran who has already separated, check with each lender about timing; the request window does still apply for a period after you get out.

Military Lending Act (MLA): Protection From Predatory Lending

The MLA caps the cost of certain consumer credit products including payday loans, vehicle title loans, and many installment and credit card products at 36% Military Annual Percentage Rate (MAPR) for active-duty service members and certain dependents. It does not cover mortgages or loans secured by a vehicle you're purchasing. If a lender tries to charge more than that on a covered product, ask them directly whether they've checked your MLA status covered lenders are required to verify this through the Department of Defense's database.

VA-Specific Hardship and Overpayment Programs

If you've received a VA benefit overpayment notice, you're not stuck paying it back all at once. The VA Debt Management Center offers repayment plans, and you can formally request a hardship determination if paying it back would cause serious financial difficulty. Don't ignore these notices; reach out to the Debt Management Center directly to set up terms that actually fit your budget instead of letting the debt go to collections.

What Are the Most Effective Debt Relief Options for Veterans?

The core options most veterans choose between are: free military-specific financial counseling, nonprofit credit counseling through a debt management plan, debt consolidation loans, debt settlement, and as a last resort bankruptcy. Each works differently, and the right one depends heavily on your specific numbers, not on which option sounds the most appealing.

Free Military and Veteran-Specific Financial Counseling

Military OneSource offers free, confidential financial counseling to service members, veterans (for a period after separation), and their families at no cost, no sales pitch. The National Foundation for Credit Counseling (NFCC) also has counselors experienced with military-specific situations. If you want ongoing, personalized planning rather than a one-time session, the Military Financial Advisors Association connects you with fee-only fiduciary advisors meaning they're paid a flat fee by you, not commissions from selling products, which removes a major conflict of interest. Start here before paying anyone for debt help.

Nonprofit Credit Counseling and Debt Management Plans (DMPs)

A debt management plan combines unsecured debts (think credit cards) into one monthly payment that a nonprofit agency distributes to your creditors, often at a reduced interest rate they've negotiated on your behalf. Realistically, most DMPs run three to five years. Your credit report will typically show the accounts as being paid through a debt management plan, which is a far better look to future lenders than missed payments or collections but it's not invisible, so go in with accurate expectations rather than a promise that it won't show up anywhere.

Debt Consolidation Loans: When They Help and When They Don't

A personal debt consolidation loan replaces several debts with a single new loan, ideally at a lower interest rate. This genuinely helps when you qualify for a meaningfully lower rate and you're disciplined about not running the old cards back up. It backfires when the new loan's rate isn't actually lower once fees are factored in, or when old accounts stay open and get used again. If any of your existing debt qualifies for the SCRA's 6% cap, compare that rate carefully against any consolidation offer before signing anything you may already have access to at a better rate than the loan you're being offered.

Debt Settlement: Risks Veterans Should Understand Before Signing Up

Debt settlement means negotiating to pay less than you owe, usually in a lump sum, in exchange for the creditor writing off the rest. Two things people are often surprised by: first, any forgiven amount over $600 generally counts as taxable income, and the creditor will send you (and the IRS) a Form 1099-C reflecting it so a "$5,000 win" can come with an unexpected tax bill the following spring. Second, settlement usually requires you to stop paying the original creditor while negotiations happen, which can drop your credit score by 100 points or more and stays on your report for years. If you're on a fixed VA income, that tax surprise deserves real attention before you commit talk to a tax professional about your specific numbers first.

Bankruptcy as a Last-Resort Option for Service Members and Veterans

Bankruptcy can genuinely be the right move when debt has become unmanageable through other paths, but it's a legal process with long-term consequences, not a quick fix. Chapter 7 can eliminate most unsecured debt relatively quickly but may require giving up certain assets; Chapter 13 sets up a repayment plan over three to five years and lets you keep more property. One detail worth knowing: debt discharged in bankruptcy is not treated as taxable income, unlike debt settlement. Service members and veterans in security-sensitive roles should also ask how a bankruptcy filing could interact with a security clearance review before filing. This is genuinely not a do-it-yourself decision speak with a licensed bankruptcy attorney, ideally one with military-client experience, before moving forward. (Nothing here is legal advice it's general information to help you ask the right questions.)

How Do You Choose the Right Debt Relief Option for Your Situation?

The right option really comes down to three things: how much debt you're carrying relative to your income, whether that debt is pre-service or post-service (which determines SCRA eligibility), and how much breathing room is actually left in your budget after fixed obligations including any money you regularly send to family.

As a general guide:

If your debt is mostly manageable but disorganized, free counseling can usually get you a clear plan without committing to anything yet.

If you have multiple high-interest unsecured debts and steady income, a debt management plan often makes the most sense.

If you qualify for a meaningfully lower rate and won't reopen old accounts, consolidation can work well.

If you're facing genuinely unaffordable debt and have weighed the tax and credit consequences honestly, settlement may be worth exploring with a tax professional in the loop.

If none of the above realistically covers your situation, bankruptcy, discussed with an attorney, is there as a structured reset.

Before committing to anything that charges a fee, talk to a free counselor first. A 30-minute call can save you from a program that isn't actually the best fit.

Step-by-Step: How to Start the Debt Relief Process as a Veteran

Gather every statement you have, and sort debts into pre-service and post-service this single step determines your SCRA eligibility.

Book a free counseling session through Military OneSource or the NFCC. It costs nothing and gives you an outside, professional read on your situation.

Check whether SCRA or MLA protections are already applied to your existing accounts; many people qualify and never request it.

Compare what the counselor recommends against the five options above, and ask direct questions about timelines and credit impact.

If it feels right, bring trusted family into the conversation not as a confession, but as a team decision. Asking for support is not the same as losing face.

Set a 90-day check-in with yourself to review progress and adjust the plan if something isn't working.

Final Thoughts: Taking the First Step Toward Financial Stability

Debt is common, fixable, and nothing to be ashamed of especially when the causes are tied directly to the demands of military life. Free, professional help is sitting right there waiting for you, whether that's a counselor at Military OneSource or a fiduciary advisor who understands your situation. The hardest part is usually just making the first call. Once you do, you're not figuring this out alone anymore.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

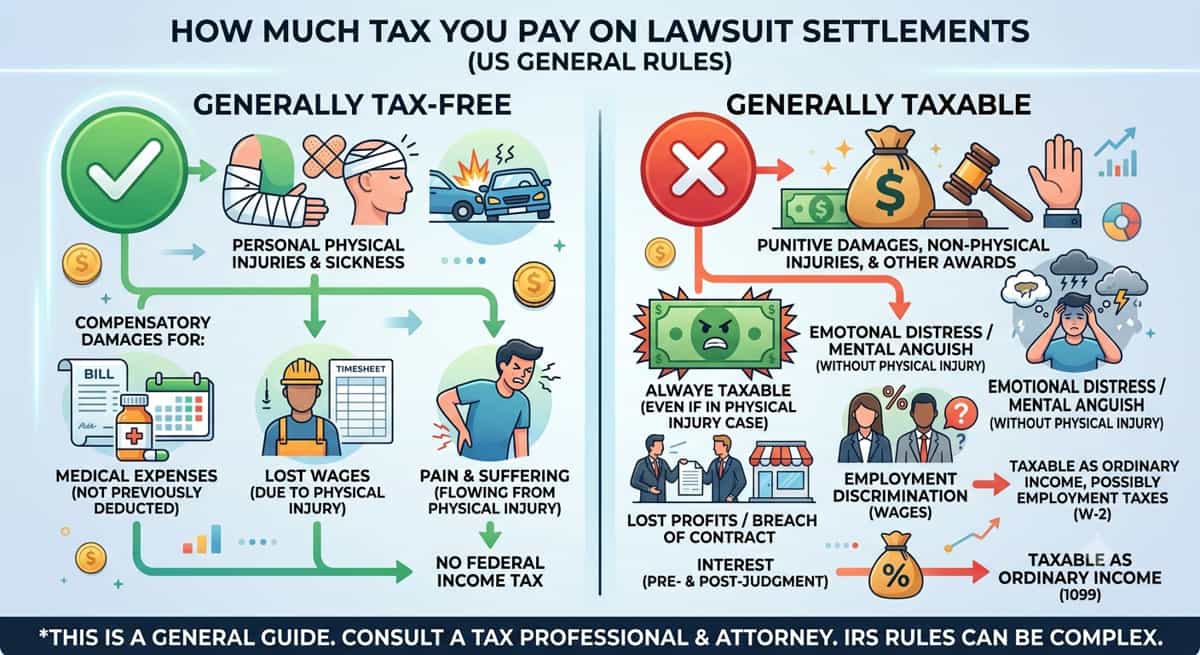

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read