Debt Management- The Right Program

Every month, you set aside money to send back home to your family, you're keeping up with rent, groceries, and bills, and then the credit card statements arrive each one a little higher than the last. You're not alone. Many people juggling life in the U.S. while supporting loved ones abroad find themselves carrying more credit card debt than they ever expected.

A debt management program is simply a structured plan, usually set up with the help of a credit counseling agency, that combines your debts into one manageable monthly payment often at a lower interest rate. This article walks you through what these programs really are, why they might (or might not) be the right fit for you, and how to choose wisely without falling into common traps.

What Is a Debt Management Program - and Is It Right for You?

In plain terms, a debt management program (DMP) is an agreement set up through a nonprofit credit counseling agency. The agency talks to your creditors on your behalf, often gets your interest rates lowered, and combines all your payments into a single monthly bill that you pay to them; they then distribute it to each creditor.

A debt management program is a structured repayment plan, arranged through a credit counseling agency, that consolidates your unsecured debts into one monthly payment often with reduced interest rates typically completed within three to five years.

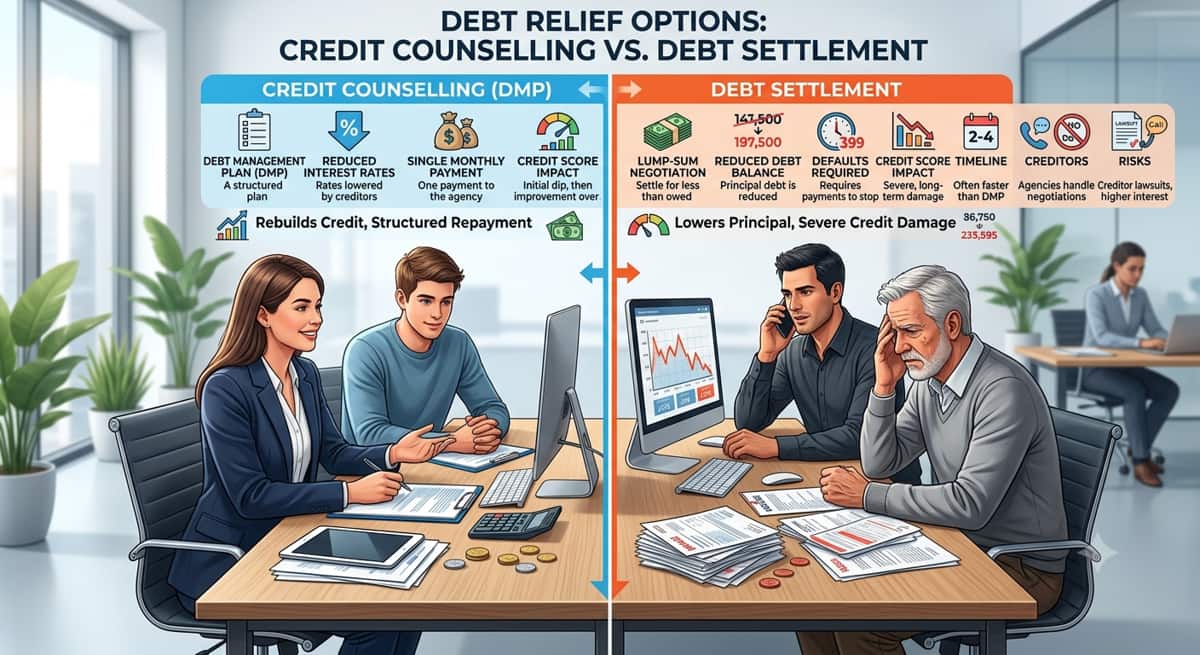

This is different from a debt consolidation loan, where you borrow new money to pay off old debts, and different from debt settlement, where a company negotiates to pay less than what you actually owe (often damaging your credit in the process).

Who tends to qualify for a DMP? Generally, people with:

Credit card balances

Medical bills

Other unsecured debts (meaning debts not tied to property, like a house or car)

If most of your debt falls into these categories and you have steady income to make a consistent monthly payment, a DMP could be worth exploring.

Why South Asians in the USA Face Unique Debt Challenges

If you're part of the South Asian community in the U.S., your financial picture often looks a little different and that's worth acknowledging.

Many families balance sending remittances home with covering their own household expenses. There's often a sense of shared financial responsibility helping siblings, parents, or extended family with visa fees, legal costs, or emergencies back home. On top of that, immigration-related expenses (green card applications, lawyer fees, work permit renewals) can pile up quickly and unexpectedly.

There's also the matter of credit history. If you're relatively new to the U.S. financial system, you might have what's called a "thin credit file"meaning you simply haven't built up much credit history yet, even if you're financially responsible. This can affect which debt relief options are realistically available to you.

And then there's the cultural piece. In many South Asian households, debt carries a sense of shame or failure, something to hide rather than address. But debt is a financial situation, not a reflection of your character or worth. Recognizing these pressures is the first step toward making a clear-headed decision about what to do next.

The 4 Main Types of Debt Relief Programs - Explained Simply

Before you can choose the right path, it helps to understand your real debt options. Here's a breakdown of the four most common routes.

1. Debt Management Plan (DMP)

This is the option discussed above working with a credit counseling agency to consolidate payments and often reduce interest rates. It typically takes three to five years to complete.

Pros: Lower interest rates, one simple monthly payment, creditors are often more cooperative when a reputable agency is involved.

Cons: You'll usually need to close the credit cards involved, and it requires consistent monthly payments over several years.

2. Debt Consolidation Loan

A debt consolidation loan combines multiple debts into a single loan with one monthly payment, making repayment easier to manage. It can help reduce financial stress, simplify budgeting, and potentially lower interest costs, depending on the loan terms and your credit profile.

Pros: Can simplify your finances and potentially lower your overall interest costs.

Cons: Usually requires a decent credit score to qualify for a good rate. If your credit isn't strong, the loan terms might not actually save you money.

3. Debt Settlement

With debt settlement, a company negotiates with your creditors to let you pay less than the full amount you owe, sometimes significantly less.

Pros: Could reduce your total debt amount.

Cons: This route can seriously hurt your credit score, often involves you stopping payments for months (which creditors don't like), and any forgiven debt may be counted as taxable income.

4. Bankruptcy (Chapter 7 & Chapter 13)

Bankruptcy is generally considered a last resort when other options aren't realistic. Chapter 7 can wipe out most unsecured debts but may require giving up certain assets. Chapter 13 sets up a repayment plan over three to five years while you keep your property.

A note for visa holders and green card applicants: bankruptcy can have implications for immigration proceedings in some cases, so this is an area where speaking with both a bankruptcy attorney and an immigration attorney is important before moving forward.

A quick but important note: every financial situation is different, and outcomes from any of these programs can vary widely depending on your specific circumstances. Speaking with a licensed, accredited credit counselor before making a decision is always a smart move.

How to Choose the Right Debt Management Program - 5 Key Factors

Rather than thinking of this as "picking a product," think of it as answering a few honest questions about your situation.

1. What kind of debt do you have, and how much? Unsecured debts like credit cards and medical bills are generally what DMPs and debt settlement address. If most of your debt is secured (like a car loan or mortgage), these programs won't apply to it.

2. Can you realistically make a consistent monthly payment? DMPs require commitment over several years. Be honest about your monthly cash flowafter rent, bills, remittances, and essentials, what's left over?

3. How much will this affect your credit score? Generally speaking, DMPs tend to be gentler on your credit than debt settlement or bankruptcy, though closing credit cards can have some initial impact. Debt settlement and bankruptcy tend to cause more significant, longer-lasting dips.

4. How quickly do you need to be debt-free? If you're facing a more urgent situation like an upcoming major expense or a need to qualify for a loan soon your timeline might push you toward a faster (though sometimes more drastic) option.

5. Could this affect your immigration status? This is often overlooked, but it's a big one. If you're on a visa, have a pending green card application, or are otherwise navigating immigration processes, certain debt relief options particularly bankruptcy could have downstream effects. This is worth discussing with a qualified immigration attorney alongside your financial decision.

If you're working on rebuilding or strengthening your credit alongside any of these options, it's worth exploring resources on improving your credit score as a complementary step.

Red Flags to Watch Out For in Debt Relief Companies

Unfortunately, debt relief is an area where scams and predatory practices are common. Here's what to watch for:

Upfront fees before any service is provided. Under FTC rules, debt relief companies generally cannot charge fees before they've actually settled or reduced your debt.

Guarantees that your debt will simply "disappear." No legitimate company can promise this debt relief always involves some kind of negotiation, repayment, or legal process.

Pressure to immediately stop talking to or paying your creditors. This is a common tactic used by less reputable settlement companies and can lead to a snowball of late fees, collection calls, and credit damage.

No verifiable address, or no accreditation from organizations like the NFCC (National Foundation for Credit Counseling) or FCAA (Financial Counseling Association of America).

One more thing worth knowing: some predatory services specifically target immigrant communities with ads in Hindi, Urdu, Bengali, and other languages, knowing that people may be more likely to trust something presented in their native language. Familiarity isn't the same as legitimacy always verifying accreditation regardless of what language a company advertises in.

A few questions worth asking any debt relief company before signing anything:

Are you accredited by the NFCC or FCAA?

What fees will I be charged, and when?

Can you put your promises in writing?

What happens to my credit score during this process?

Can I cancel at any time without penalty?

Step-by-Step: How to Enroll in a Debt Management Program

If a DMP sounds like the right fit, here's generally how the process works:

List out all your debts. Write down each balance, interest rate, and creditor. This gives you (and your counselor) a clear picture to work from.

Get a free credit counseling session. Reach out to an NFCC-member agency for an initial consultation this is typically free and gives you a chance to ask questions before committing to anything.

Review the proposed plan carefully. Look at the fees involved, the expected timeline, and the agreements being made with your creditors. Make sure you understand exactly what you're signing up for.

Stop using the credit cards included in the plan. This is usually a requirement the goal is to pay down existing balances, not add new charges.

Make one monthly payment to the agency. They handle distributing the funds to each of your creditors according to the agreed plan.

Keep an eye on your credit report. Throughout the process, check periodically to make sure payments are being reported correctly and your progress is on track.

Debt Is Temporary, Financial Freedom Is Possible

If there's one thing to take away from all of this, it's that debt is a situation not a life sentence, and certainly not a reflection of your worth or your family's honor. Many people, including those balancing family responsibilities across continents, have walked this path and come out the other side.

Reaching out for help with a debt management plan, credit counseling, or any other form of debt relief isn't a sign of failure. It's a sign that you're taking your financial future seriously. The sooner you understand your options and your monthly payment plan, the sooner you can start working toward becoming debt-free on your own terms.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read