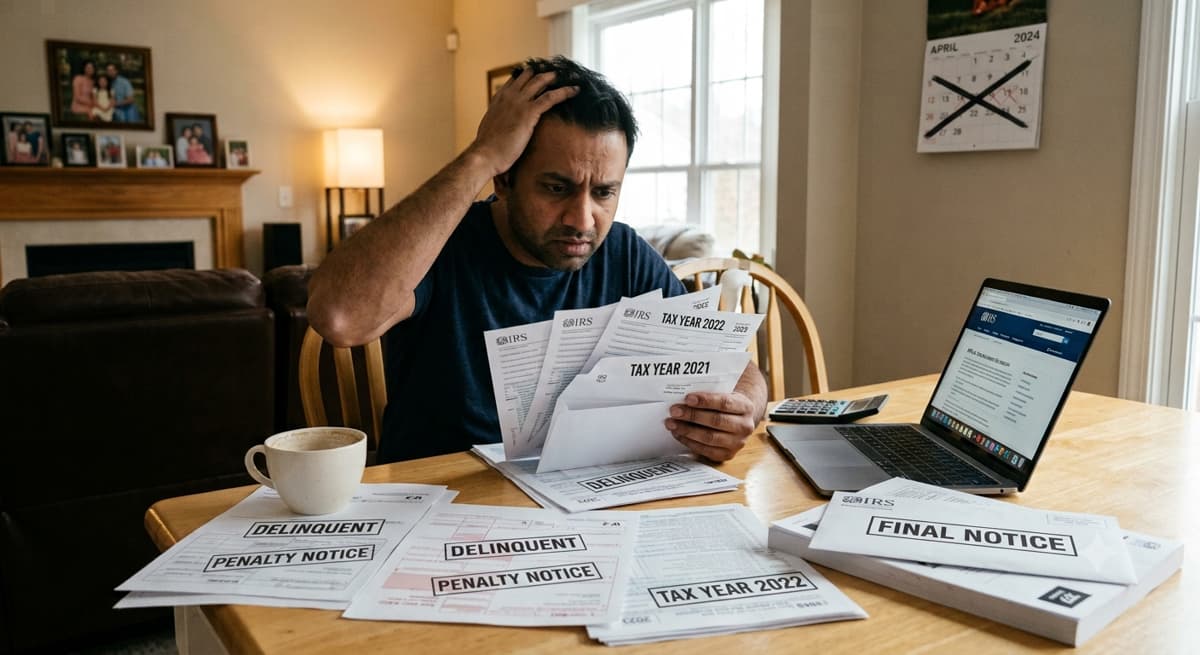

Seeing an envelope from the IRS in your mailbox can make your stomach drop. Maybe you haven't opened it yet. Maybe it's been sitting on the kitchen counter for a week, and every time you walk past it, you feel a little sick.

Here's what you need to know before you read any further: owing the IRS money is a common, fixable problem. It is not a crime, and it does not mean your life is about to fall apart. Every year, millions of Americans, including a lot of immigrant families, end up owing back taxes for reasons that have nothing to do with dishonesty. The IRS has set up real, legal ways to deal with this.

If you owe the IRS and don't pay, you'll be charged a monthly penalty plus interest on the unpaid amount, and the IRS will send a series of notices asking for payment. If you ignore those notices long enough, the IRS can eventually file a lien or garnish wages and bank accounts. But you have options the entire time, including monthly payment plans, settling for less than you owe, and temporary hardship pauses. The single most important thing you can do is respond, not hide.

What Counts as "Unpaid IRS Taxes"?

"Unpaid IRS taxes" usually means one of three things, and it's worth knowing which one applies to you, because it changes what happens next.

The first and most common situation is a balance due. You filed your tax return, the return showed you owed money, and you didn't pay all of it. The IRS already knows about this debt because you reported it yourself.

The second is an unfiled return with tax owed. Maybe you didn't file at all for one or more years, out of fear, confusion, or just not knowing how. The IRS may not know the exact amount yet, but if you had taxable income, the debt exists whether a return was filed or not.

The third is a new balance from an audit or adjustment. Sometimes the IRS reviews a past return, finds unreported income or a miscalculation, and sends you a bill for the difference, often with penalties added on.

It also matters how far behind you are. Being a few weeks late on one payment is very different from carrying a balance that's been sitting unpaid for a year or more. The penalties and interest are the same in both cases, but the longer a balance sits, the more it grows, and the more collection steps the IRS may take.

Why This Happens So Often in Immigrant and South Asian Households

If you're dealing with this, you are far from alone, and there are real reasons this happens more often in immigrant communities than people talk about.

A lot of South Asian families in the US are managing complicated tax situations for the first time. Maybe you have W-2 income from a job, plus 1099 income from consulting or freelance work, plus a small family business like a motel, gas station, or restaurant that runs partly on cash. Maybe you're sending money home to family in India, Pakistan, Bangladesh, or Sri Lanka, and you're not sure whether that remittance needs to be reported, or you've heard scary things about FBAR and foreign account reporting and you've frozen up instead of asking for help.

And for a lot of first-generation parents, there's a language barrier that makes IRS letters feel impossible to deal with, on top of a cultural instinct to handle problems quietly rather than calling a government number. All of this adds up to one thing: tax debt happens here for ordinary, fixable reasons. It is not a reflection of anyone's character.

What Actually Happens If You Don't Pay the IRS

The IRS doesn't show up at your door. What actually happens is a predictable, step-by-step process, and understanding it takes a lot of the fear out of it.

The IRS Notice Timeline

The first letter you'll get is Notice CP14. It tells you how much you owe, including any penalties and interest so far, and asks for payment within 21 days. This is simply the IRS letting you know there's a balance, it isn't a threat.

If you don't respond, you'll typically get Notice CP501, a reminder that the balance is still open, followed by CP503, a second reminder with slightly more urgency. If the balance still isn't addressed, the IRS sends CP504, which is more serious. CP504 warns that the IRS may move forward with collection action, like a levy, if the debt isn't resolved. Each notice gives you a window to respond, and responding at any point in this sequence, even late, stops things from escalating further.

Penalties and Interest: How Fast Debt Grows

Two separate charges build on top of what you originally owed.

The failure-to-pay penalty is 0.5% of your unpaid balance for each month or partial month it remains unpaid, capped at 25% of the original amount owed. If you set up an IRS payment plan, this penalty rate is cut in half, to 0.25% per month, for as long as you're current on the plan.

The failure-to-file penalty is steeper: 5% per month, also capped at 25%, and it applies if you didn't file your return at all by the deadline. This is exactly why tax professionals repeat one piece of advice so often: file your return even if you can't pay. The failure-to-file penalty is ten times larger than the failure-to-pay penalty, so filing late but paying nothing is far better than not filing at all.

On top of both penalties, the IRS charges interest on the unpaid balance, compounded daily. The rate is set quarterly; for individuals, it's 7% for the first and third quarters of 2026 and 6% for the second quarter. Because it compounds daily, the balance grows a little every single day it's unpaid, which is why even partial payments made early help reduce what you ultimately owe.

Liens, Levies, and (Rarely) Passport Restrictions

If a balance goes unaddressed long enough, the IRS can take two kinds of action.

A Notice of Federal Tax Lien is a legal claim against your property, it doesn't take anything from you directly, but it can show up during a mortgage or loan application and complicate selling property. A levy is more direct: it allows the IRS to actually take funds, for example from a bank account or paycheck, to satisfy the debt.

In rare cases involving very large, long-ignored balances (generally above a high threshold set by law), the IRS can certify the debt as "seriously delinquent" to the State Department, which can affect passport renewal. This is genuinely rare and almost always follows years of no response to multiple notices, not a single missed payment. The good news: the IRS very rarely takes any of these steps against someone who is actively making payments on an agreed plan.

Will Unpaid Taxes Affect My Visa, Green Card, or Citizenship?

This is usually the question underneath all the other questions, and it deserves a direct, careful answer.

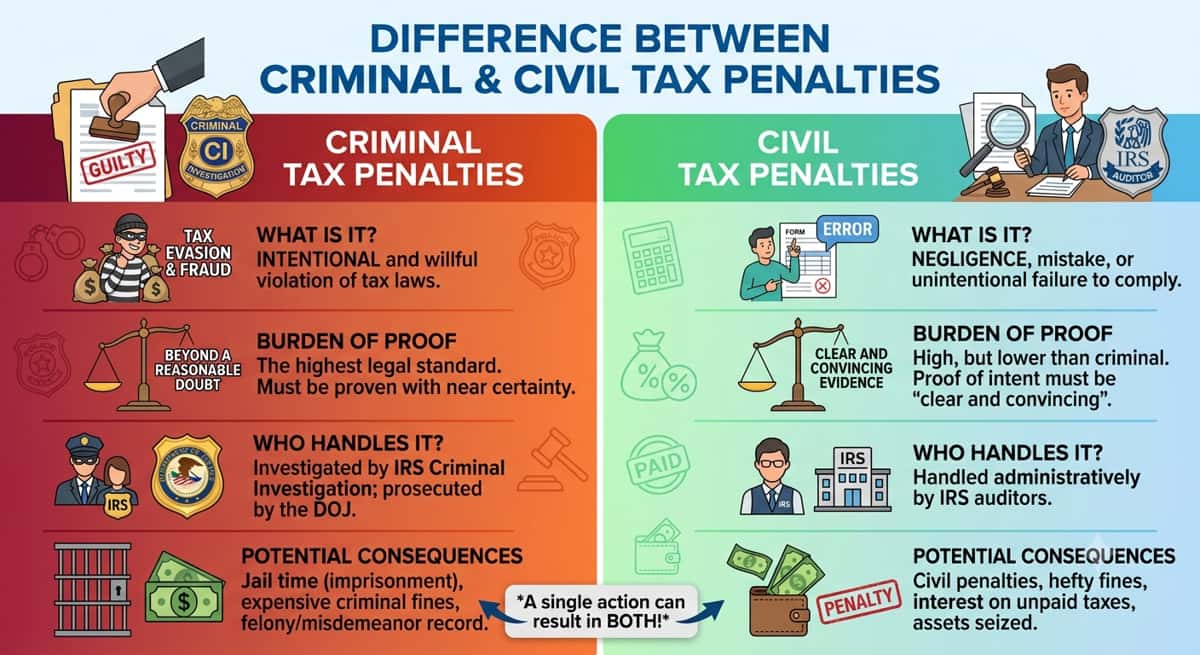

Owing back taxes is a civil, financial matter. It is completely different from tax fraud or tax evasion, which involve intentionally lying or hiding income, and which are criminal matters. Simply owing money you've honestly reported, or falling behind on payments, does not put you in that category.

That said, immigration applications do sometimes ask about tax compliance, and unresolved tax debt can come up during certain processes. For example, during naturalization, USCIS reviews "good moral character," and some applicants choose to show proof of an active IRS payment plan to demonstrate they are addressing a known debt rather than ignoring it. Certain visa or status applications may also ask whether you have outstanding federal debts.

This is genuinely a case where the details of your specific situation, your visa category, how long the debt has existed, and whether you're already on a payment plan matter a lot, and getting it wrong can have real consequences. This article cannot give you immigration legal advice. If you have an upcoming visa renewal, green card application, or naturalization interview and you also have unpaid taxes, talk to an immigration attorney, ideally one who also understands tax debt, before your filing. Resolving the tax side proactively, even by simply starting a payment plan, is almost always viewed better than leaving it open.

Will Owing the IRS Hurt My Credit Score?

Owing the IRS money does not, by itself, lower your credit score. Federal tax liens were removed from the three major credit bureaus' reporting criteria years ago, so a tax debt alone won't show up on your credit report the way a missed credit card payment would.

Where it can still cause problems is during major financial transactions. If the IRS files a lien on your property and you later apply for a mortgage or a business loan, the lender's underwriting process can turn up that lien through public records, even though it's not on your credit report. This can complicate or delay approval. The takeaway: your credit score itself is safe, but a long-ignored balance can still get in the way of buying a home or financing a business down the road.

What to Do If You Owe the IRS and Can't Pay in Full

If you're staring at a notice right now, here's the actual order of operations.

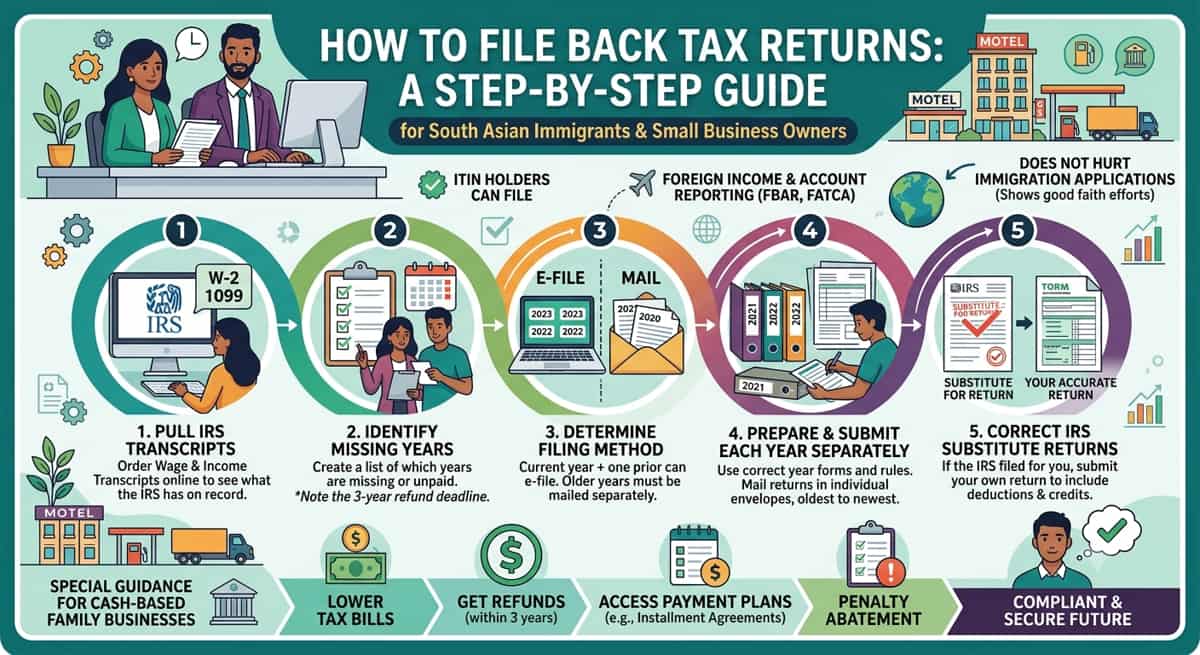

Step 1 — File Your Return Even If You Can't Pay

If you haven't filed yet, file now, even with zero payment attached. As covered above, the failure-to-file penalty is far more expensive than the failure-to-pay penalty, and most relief options require all your returns to be filed before the IRS will even consider them.

Step 2 — Pay What You Can Now

Even a partial payment helps, because interest and the failure-to-pay penalty are both calculated on the remaining balance. Paying something today, even a small amount, immediately starts shrinking what future penalties and interest are calculated against.

Step 3 — Choose a Resolution Option

Once you've filed and paid what you can, you have several real paths forward, depending on how much you owe and your financial situation.

Short-term payment plan: For balances under $100,000 (combined tax, penalties, and interest), you can get up to 180 days to pay in full, with no setup fee. Good if you just need a few extra months.

Long-term installment agreement: A monthly payment plan, generally for balances under $50,000, set up online in most cases. Setup fees are reduced or waived for lower-income applicants, and the IRS applies that discount automatically if you qualify.

Offer in Compromise (OIC): This lets you settle your debt for less than the full amount owed, if the IRS agrees you genuinely can't pay the full balance even over time. You'll need to have filed all required returns and made current-year estimated payments to qualify, and approval isn't guaranteed, but for the right situation it can meaningfully reduce what you owe.

Currently Not Collectible (CNC) status: If paying anything right now would create real financial hardship, the IRS can temporarily pause collection. The debt doesn't disappear, and interest keeps accruing, but it buys breathing room while your situation stabilizes.

First-Time Penalty Abatement: If you've generally filed and paid on time in the past and this is a one-off situation, you may qualify to have penalties (though not interest) waived for this instance.

Step 4 — Get Help If You're Overwhelmed

You don't have to figure this out alone, and you don't have to pay a fortune to get real help. The Taxpayer Advocate Service is a free, independent office within the IRS that steps in specifically when someone is facing hardship or can't get their issue resolved through normal channels. Low Income Taxpayer Clinics (LITCs) offer free or low-cost help from licensed attorneys, CPAs, and enrolled agents for qualifying lower-income taxpayers, and many LITCs have staff who speak languages common in South Asian communities. These are real, legitimate, no-catch resources, not a trick.

Should You Hire a Tax Professional or Handle It Yourself?

For a simple, recent balance with a clear payment plan, many people handle it themselves directly through the IRS website. But if your situation involves multiple unfiled years, business income, foreign accounts, or a large balance, getting professional help is usually worth it.

A tax attorney becomes important if there's a legal dispute, a criminal question, or significant assets at risk.

Be cautious of national "tax relief" companies that advertise heavily, promising to settle your debt for "pennies on the dollar." Some are legitimate, but this space also attracts predatory firms that charge large upfront fees and deliver little, and they specifically target people who are scared and unfamiliar with the system, which unfortunately includes a lot of immigrant taxpayers. Before paying anyone a retainer, check that they're a verifiable, licensed CPA, EA, or attorney, and be wary of anyone who guarantees a specific settlement amount before reviewing your actual financial details.

Common Mistakes to Avoid When You Owe the IRS

A few patterns show up again and again, and avoiding them will save you real money and stress.

Ignoring the notices. Letters don't stop coming because you don't open them, they keep escalating.

Not filing out of fear. This triggers the much larger failure-to-file penalty and removes you from eligibility for most relief options.

Draining retirement savings or borrowing from family at high informal interest to pay the IRS immediately, when a payment plan would have been far less costly overall.

Using unlicensed preparers who may file inaccurately or disappear when problems arise.

Assuming the debt will quietly expire. The IRS generally has 10 years from when a tax is assessed to collect it (this is called the Collection Statute Expiration Date, or CSED). While real, this is not a strategy, certain actions (like requesting a payment plan) can pause or extend that clock, and the interest and risk of collection action in the meantime make "waiting it out" a poor plan.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

Self-Employed and Owe Taxes? A Guide for 1099 Workers

11 min read

Unfiled Tax Returns: What Should You Do?

11 min read

How Do I File Returns For Back Taxes?

12 min read

What Is The Difference Between Criminal Tax Penalties And Civil Tax Penalties?

11 min read

Tax Evasion Vs Tax Fraud And The Statute Of Limitations

9 min read

What Is An IRS Substitute For Return(SFR)?

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation