Understanding Tax Settlement: The Offer In Compromise

That letter from the IRS sitting on your kitchen table you've read three times, but it still doesn't feel real. Maybe it's $18,000. Maybe it's more. You're already sending money home to your parents in Gujarat or Sylhet, your kids are in school, and the rent isn't getting any cheaper. The last thing you want is to tell your family you're drowning in tax debt. In South Asian communities, financial struggle often carries a quiet shame, something you carry alone.

But here's what most people don't know: the IRS doesn't always demand every dollar you owe. There's a legitimate federal program called the Offer in Compromise (OIC) that may allow you to settle your tax debt for significantly less than the full amount.

What Is an Offer in Compromise (OIC)?

An Offer in Compromise is an official agreement between you and the IRS that allows you to settle your tax debt for less than the full amount you owe.

Think of it this way: if you genuinely cannot pay back everything you owe and the IRS can see that they would rather accept a realistic, smaller amount now than chase an unreachable full payment for years. It's practical for both sides.

The program is authorized under IRC § 7122, and the IRS considers three situations where an OIC makes sense:

You can't pay the full amount — This is the most common reason. Your income, savings, and assets simply don't add up to what you owe.

You dispute the debt itself — You believe the IRS calculated your tax liability incorrectly.

Paying in full would be deeply unfair — Even if you technically could pay, doing so would cause serious financial hardship or would be unjust given your circumstances.

Here's a real-world example many in our community can relate to: imagine a software engineer in New Jersey who owes $42,000 in back taxes. After reviewing his monthly income, living expenses, and savings, the IRS determines he can realistically repay only $9,000. Under OIC, that $9,000 could be accepted as full settlement and the remaining debt is gone.

It's not a loophole. It's a legitimate path to tax debt relief that thousands of Americans use every year.

Who Qualifies for an Offer in Compromise?

Not everyone who owes back taxes will qualify for an OIC and that's important to understand upfront. The IRS approves roughly 30 to 40 out of every 100 applications it receives. The decision comes down to one core question: Can you realistically pay back what you owe, given your income, expenses, and assets?

The IRS calls this your Reasonable Collection Potential (RCP) essentially, the maximum amount they believe they can collect from you. If your offer meets or exceeds that number, you have a strong chance of approval.

But before the IRS even looks at your finances, you need to meet some basic requirements:

You Must Be Current on All Tax Filings

Every tax return you were required to file must be submitted before you apply. If you've missed any years, file those returns first.

This is especially relevant if you arrived in the U.S. on an H-1B or L-1 visa, or recently transitioned off a student visa. It's easy to miss a filing year during those transitions and many people don't realize it until a notice arrives.

You Must Be Current on Estimated Tax Payments

If you're self-employed whether you run a restaurant in Queens, a convenience store in New Jersey, or you freelance as an IT consultant you're expected to pay taxes quarterly. You must be up to date on those payments before applying.

You Cannot Be in Active Bankruptcy

If you currently have an open bankruptcy case, the IRS will not process your OIC application. The two processes conflict legally, and you'll need to wait until the bankruptcy is resolved.

Once you've confirmed you meet these basics, use the free IRS OIC Pre-Qualifier Tool to get an early sense of whether you're likely to qualify. It takes about 10 minutes and asks straightforward questions about your income and assets.

One important note: many South Asian families have layered finances with a spouse on a dependent visa contributing income, money sent from relatives abroad, or shared household expenses with extended family. These situations can complicate your income picture significantly. If your finances feel complicated, a licensed tax professional can help you present them accurately and fairly.

How Much Will the IRS Accept?

"The IRS calculates your offer based on what they believe they can realistically collect from you, not what you owe."

This is one of the most misunderstood parts of the OIC process. Your offer amount isn't a negotiation based on what feels fair it's a math-based calculation. The IRS uses a specific formula that looks at your monthly disposable income (what's left after allowable living expenses) and the value of your assets.

There are two ways to structure your payment, and each uses a slightly different formula:

Lump-Sum Cash Offer (5 Payments or Fewer)

Formula: (Monthly Disposable Income × 12) + Net Asset Value

You must include a 20% non-refundable deposit when you submit your application. Even if the IRS rejects your offer, they keep that deposit.

Periodic Payment Offer (6–24 Monthly Payments)

Formula: (Monthly Disposable Income × 24) + Net Asset Value

With this option, you continue making monthly payments while the IRS reviews your case — which can take six months to a year.

A simple example: Say you're a Bangladeshi-American small business owner in Queens. After accounting for rent, groceries, utilities, and other IRS-approved living expenses, you have $300 left each month. Your car and savings account add up to $4,000 in total asset equity.

Lump-sum offer: ($300 × 12) + $4,000 = $7,600

Periodic offer: ($300 × 24) + $4,000 = $11,200

Either figure could potentially settle a debt many times larger if your documentation supports it.

How to Apply for an Offer in Compromise: Step by Step

The application process has several moving parts, but if you take it one step at a time, it's very manageable. Here's exactly what to do:

Step 1: Check Your Eligibility First Before filling out a single form, use the free IRS OIC Pre-Qualifier Tool It takes about 10 minutes and tells you whether pursuing an OIC makes sense for your situation. Don't skip this, it saves time and sets realistic expectations.

Step 2: Gather Your Financial Documents You'll need recent tax returns, pay stubs, bank statements, property records, and business financials if you're self-employed. The more organized you are here, the smoother the process.

Step 3: Complete the Required IRS Forms

Form 656 — the actual Offer in Compromise application

Form 433-A (OIC) — for individuals, detailing your full financial picture

Form 433-B (OIC) — for business owners

These forms ask detailed questions about your income, expenses, assets, and debts. Answer everything honestly and completely.

Step 4: Pay the Application Fee The filing fee is $205. If your income falls below IRS low-income guidelines, this fee can be waived entirely.

Step 5: Keep Filing and Paying During Review Once submitted, the IRS typically takes 6 to 12 months to decide. During that entire period, you must stay current on all tax filings and any required payments. Falling behind automatically disqualifies your application.

Step 6: Respond Quickly to Any IRS Requests The IRS may ask for additional documents or clarification. Respond promptly delays can slow your case or result in it being closed.

Step 7: Wait for the Decision There are three possible outcomes:

Accepted — you pay the agreed amount and the debt is resolved

Rejected — you have 30 days to appeal

Returned — your application was incomplete or you fell out of compliance; this is not the same as a rejection and may be resubmitted

A note on language barriers: If English is not your first language, navigating IRS forms can feel overwhelming. The IRS does offer some multilingual resources, but working with a bilingual Enrolled Agent or CPA, someone who understands both the tax code and your cultural context can make a significant difference in how accurately your case is presented.

One important warning: Be very cautious of companies advertising "pennies on the dollar" tax settlements, especially those advertising heavily in South Asian community media. The IRS has explicitly warned against OIC mills companies that charge large upfront fees, make unrealistic promises, and often file applications on behalf of people who don't even qualify. Always verify credentials before hiring anyone to help with your taxes.

What Happens After You Submit Your OIC Application

Once your application is in, the waiting begins and it can feel uncertain. Here's what's actually happening behind the scenes and what to expect.

The IRS Pauses Collection Activity From the moment the IRS receives your OIC, they put collection efforts on hold. That means no levies, no garnishments, and no aggressive collection action while your case is under review. This alone brings significant relief to many families dealing with mounting pressure.

The Review Typically Takes 6 to 12 Months During this time, an IRS examiner reviews your financial forms, verifies your income and assets, and determines whether your offer reflects your true ability to pay. Stay patient and stay compliant.

Three Possible Outcomes

Accepted — You pay the agreed settlement amount. Your tax debt is officially resolved and the IRS releases any existing tax liens.

Rejected — The IRS doesn't believe your offer reflects your collection potential. You have 30 days to appeal through the IRS Independent Office of Appeals — and it's worth doing.

Returned — This is different from a rejection. Your application was either incomplete or you fell behind on filings or payments during review. A returned application can often be corrected and resubmitted.

If Accepted: Your Work Isn't Quite Done Acceptance comes with a condition you must stay fully compliant with all tax obligations for the next 5 years. That means filing on time, paying what you owe, and not falling behind again. If you do, the original debt can be reinstated.

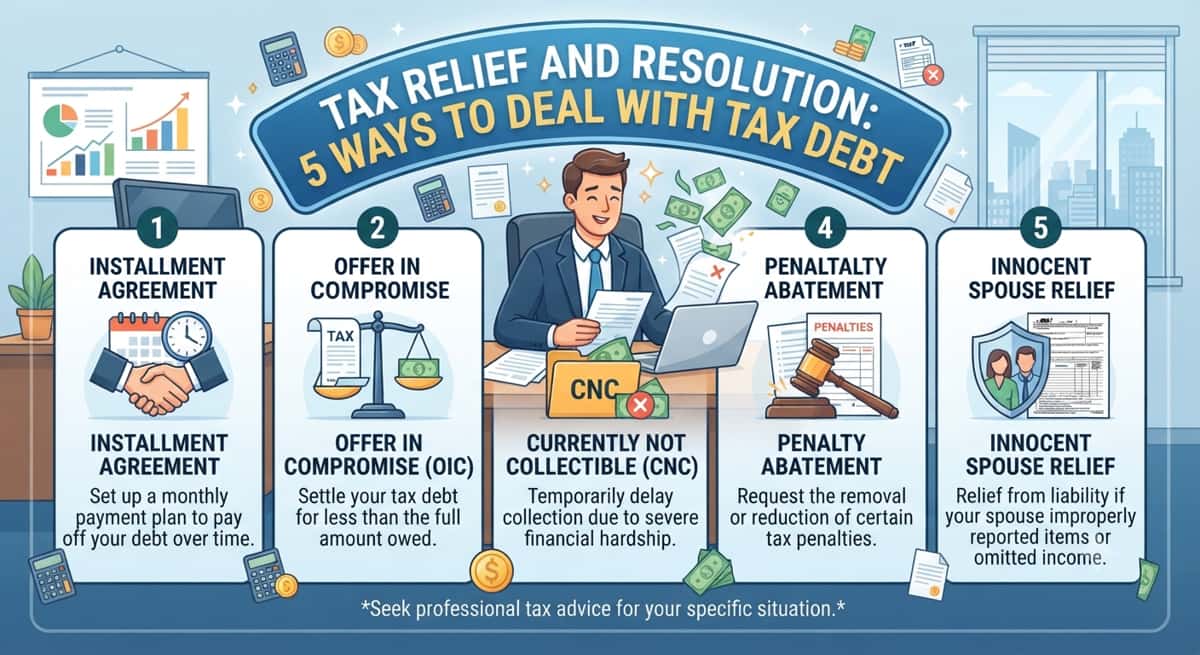

Offer in Compromise vs. Other IRS Tax Relief Options

OIC is a powerful tool but it's not the only one. Depending on your situation, a different relief option might actually be a better fit. Here's a clear breakdown:

Relief Option | Best For | What It Does |

Offer in Compromise | Can't pay the full amount | Settle your debt for less than you owe |

Installment Agreement | Can pay, but need more time | Break your debt into manageable monthly payments |

Currently Not Collectible | Severe financial hardship | Temporarily pauses all IRS collection activity |

Penalty Abatement | First-time or minor penalties | Reduces or removes penalties added to your tax bill |

Innocent Spouse Relief | Disputes over joint tax filings | Removes your liability for a spouse's tax errors |

What each option means in plain terms:

Installment Agreement is the most common path. If you can pay your full debt over time, the IRS will often work out a monthly payment plan without much friction.

Currently Not Collectible (CNC) status is worth knowing about, especially if you recently arrived in the U.S., lost your job, or are on an H-4 dependent visa with no income of your own. If paying anything right now would leave you unable to cover basic living expenses, the IRS can formally pause collection giving you breathing room until your situation improves.

Penalty Abatement won't erase your underlying tax debt, but if a significant portion of what you owe is penalties and interest, reducing those can make the remaining balance much more manageable.

Innocent Spouse Relief is particularly relevant if you filed jointly with a spouse and later discovered they underreported income or made errors you had no knowledge of. You shouldn't have to carry that burden alone.

The right option depends entirely on your specific income, assets, and circumstances — which is why speaking with a qualified tax professional before deciding is always a smart move.

Common Mistakes South Asian Taxpayers Make When Pursuing an OIC

Even well-intentioned applications get rejected often because of avoidable mistakes. Here are the ones that come up most often in the South Asian immigrant community:

1. Underreporting Household Income If your spouse works, that income counts even if they're on an H-4 visa and the income is modest. Similarly, regular money received from family abroad can sometimes be considered income depending on how it's structured. The IRS looks at your full household financial picture, so everything needs to be accurately disclosed.

2. Trusting the Wrong Companies Ads promising to "settle your IRS debt for pennies on the dollar" are common in South Asian community newspapers, radio stations, and WhatsApp groups. Many of these companies are unlicensed, charge large upfront fees, and file applications for people who don't even qualify. Always verify that anyone helping you is a licensed Enrolled Agent (EA), CPA, or tax attorney.

3. Submitting an Offer That's Too Low The IRS uses a specific formula to calculate what they expect. If your offer falls significantly below that number without strong justification, it gets rejected quickly and you've lost your application fee.

4. Applying Before All Tax Returns Are Filed This is an automatic disqualifier. If you have unfiled returns from previous years which is surprisingly common among immigrants navigating changing visa statuses file those first.

5. Not Disclosing Foreign Bank Accounts or Assets Many South Asian families have bank accounts, property, or investments back home in India, Pakistan, Bangladesh, or elsewhere. Under FBAR and FATCA rules, these must be reported to the U.S. government. Failing to disclose them even unintentionally can seriously damage your OIC application and create separate legal problems.

Free help is available. Some South Asian community organizations partner with VITA (Volunteer Income Tax Assistance) programs that offer free, IRS-certified tax help to qualifying individuals. It's worth checking if one is available in your area before paying for help.

Take the First Step Toward Tax Relief

Owing money to the IRS is stressful under any circumstances but carrying that weight quietly, while also supporting a family and building a life in a new country, is something many in our community know all too well. You don't have to figure this out alone.

The Offer in Compromise is a real, federally authorized program that has helped thousands of Americans resolve tax debt they couldn't fully pay. It takes preparation, honest financial disclosure, and patience but for those who qualify, it can mean a genuine fresh start.

Seeking help isn't a sign of failure. It's a sign that you're taking your financial future seriously.

Your next step: Start with the free IRS OIC Pre-Qualifier Tool at irs.gov — it takes about 10 minutes and costs nothing. If it looks promising, reach out to a licensed Enrolled Agent, CPA, or tax attorney who understands your situation.

Our team has worked with South Asian families across the U.S. to navigate IRS tax relief programs with clarity and confidence. Contact us today for a free consultation.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

What Are The Dangers Of Filing Your Own Taxes?

11 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

Tax Relief And Resolution: 5 Ways To Deal With Tax Debt

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- What Are The Dangers Of Filing Your Own Taxes?

11 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read