What is an IRS Tax Lien and How is it Different from an IRS Levy?

Navigating the world of tax debt can bring up unfamiliar terms, and two of the most confusing are "tax lien" and "tax levy." While they both relate to the government's efforts to collect unpaid taxes, they are fundamentally different actions. Understanding this distinction is the first step toward finding the right solution. Simply put, an IRS tax lien is the government's legal claim on your property. Think of it as a public notice that you owe the government money. It attaches to all your current and future assets, including your home, car, and financial accounts. This claim secures the government's interest in your property and makes it extremely difficult to sell or refinance any of it. The tax lien itself doesn’t take your property, but it does make it clear to the world—from banks to potential buyers—that the government has first rights to your assets should you try to sell them. An IRS tax levy, on the other hand, is the actual seizure of your assets. If you continue to ignore your tax debt, the IRS can move from a claim (a lien) to an action (a levy). A tax levy is when the IRS takes your property or money directly. This can mean garnishing your wages, levying your bank accounts, or seizing your car or other valuable property to sell it and satisfy the tax debt. The key difference is simple: a lien is a claim, while a levy is a collection. One is a legal warning, and the other is a direct, forceful action. Here is a table to help you visualize the difference:Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

Bhupinder Bajwa is a Certified Debt Specialist and Financial Counselor with over 10 years of experience helping families overcome financial challenges. Having worked extensively with the South Asian community in the U.S., he understands the cultural nuances and unique financial hurdles they may face. He is passionate about offering clear, compassionate, and actionable guidance to help individuals and families achieve their goal of becoming debt-free.

Related Articles

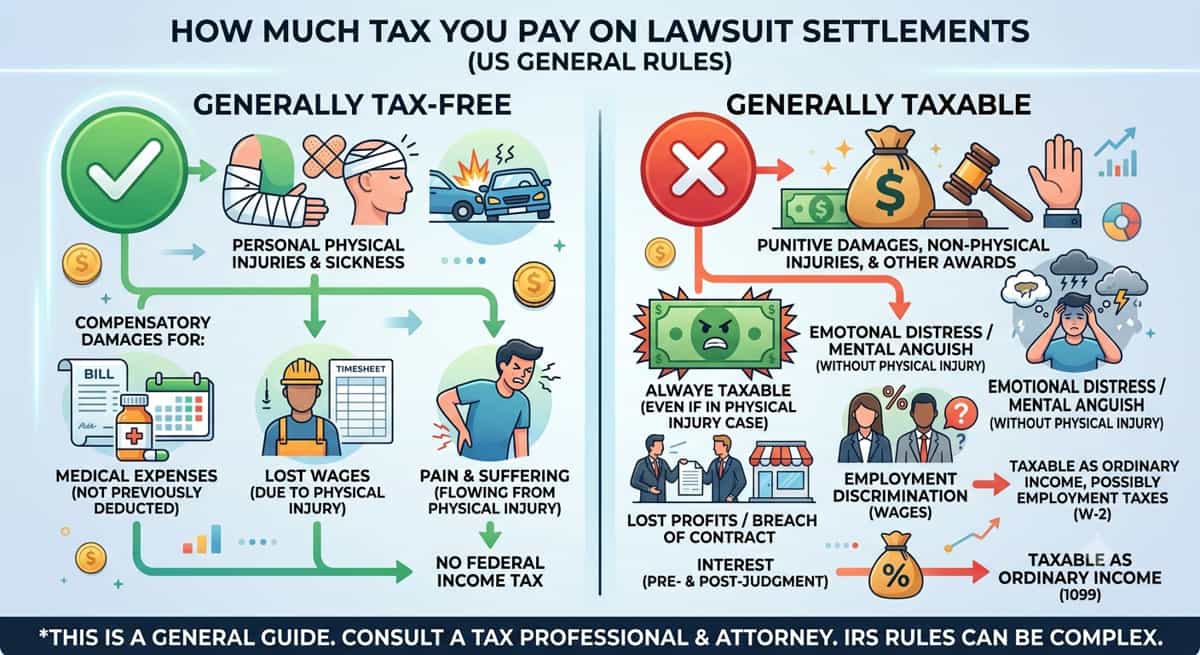

How Much Tax You Pay On Lawsuit Settlements

9 min read

Commercial Debt Management: What Business Owners Should Know

11 min read

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation

Related Posts

- How Much Tax You Pay On Lawsuit Settlements

9 min read

- Commercial Debt Management: What Business Owners Should Know

11 min read

- How Interest Rates Affect Debt

13 min read

- How To Pay Off Debt Fast With Low Income

11 min read