How To Get The IRS To Accept An Offer In Compromise?

Facing IRS tax debt can feel like carrying a heavy weight, especially when you are also balancing the daily demands of running a business or supporting family members both here in the United States and back home in South Asia. If you are struggling to pay your tax bill, you might be looking for a way to settle your tax debt for less than you owe.

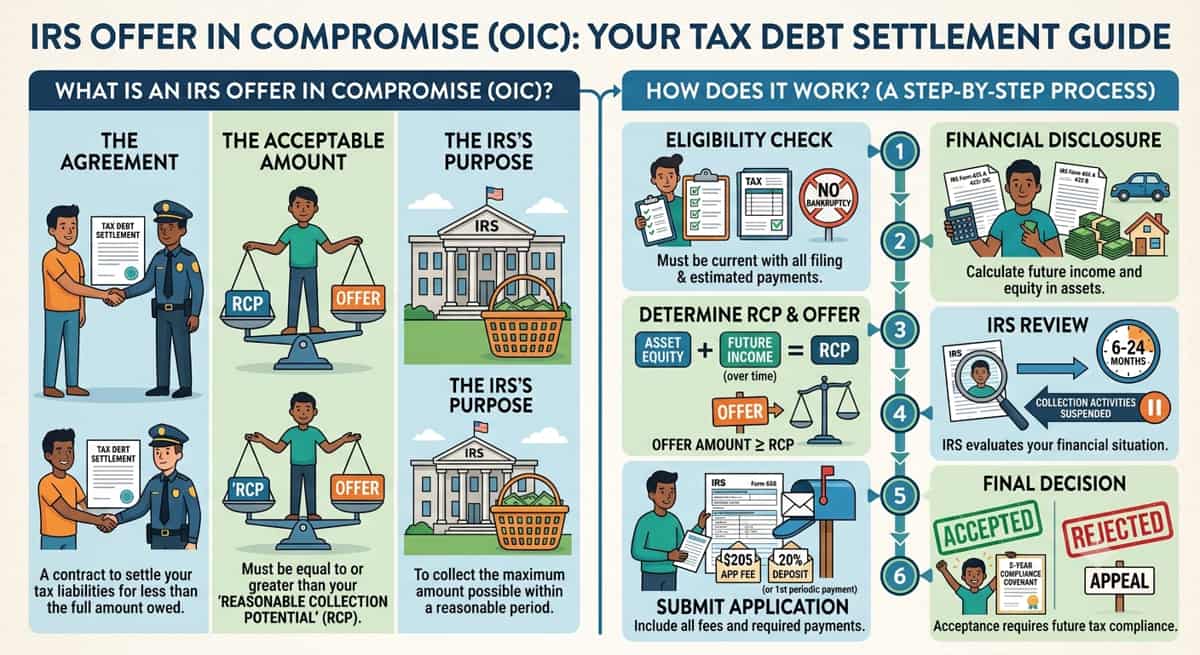

There is a legitimate government program designed to help do exactly that. It is called an Offer in Compromise (OIC). This is a formal agreement where the IRS agrees to wipe out your tax debt in exchange for a smaller, single lump-sum payment or a short-term payment plan.

What Is an Offer in Compromise (OIC)?

In plain terms, an Offer in Compromise is an agreement where you propose to pay the IRS less than your full tax bill, and the IRS agrees because they believe that's genuinely the most they're going to collect from you. It's not a discount you can just ask for, the IRS only accepts it when your financial situation supports it.

People often confuse OIC with two other things. An installment agreement is a monthly payment plan where you eventually pay the entire debt, just spread out over time. Currently Not Collectible status is when the IRS pauses collection because you genuinely can't pay anything right now, but the debt stays on the books and can come back later. An OIC is different from both; it's the only one of the three that can permanently reduce what you owe.

One more thing worth knowing upfront: be careful of companies that advertise "settle your tax debt for pennies on the dollar, guaranteed." The IRS has flagged these aggressive marketing operations sometimes called "OIC mills" on its list of tax scams to watch for in 2026. They often charge high upfront fees to people who were never going to qualify in the first place. A legitimate tax professional will tell you honestly whether an OIC is realistic for your situation before taking your money.

Why This Matters for Immigrant and First-Generation Taxpayers

If you came to the US as an adult, dealing with the IRS can feel like a different world. Back home, tax systems often work very differently, and getting a letter from the IRS can be genuinely scary especially if you're not sure what it means or whether you did something wrong.

It's also common in many South Asian families to run a small business together: a restaurant, a motel, a retail store, a gas station, or independent consulting work on a 1099. These setups come with extra tax complexity: estimated quarterly payments, payroll taxes if you have employees, and bookkeeping that's easy to fall behind on when you're busy keeping the business running.

On top of that, there's often a quiet sense of shame around owing money, which can make people put off dealing with it or turn to whoever in the community is loudly advertising a quick fix. That hesitation is completely understandable, but it's also exactly what predatory "tax relief" companies count on. The good news is that the IRS process itself is more structured and more forgiving than it might seem, and you don't need to feel embarrassed about being here, reading this.

Who Is Eligible to Apply for an Offer in Compromise?

Before the IRS will even look at your offer, you need to meet some basic requirements. Think of these as the "front door" if you don't meet them, your application gets sent back without being reviewed at all.

To apply, you must have:

Filed all your required tax returns. Every year you were supposed to file, you actually have.

Made all required estimated tax payments for the current year, if you're self-employed or have income that isn't covered by paycheck withholding.

No open bankruptcy case. If you're currently in bankruptcy proceedings, you'll need to resolve that first.

A valid extension on file, if you're applying and haven't yet filed your current year's return.

If you're a business owner with employees: you've made your required payroll tax deposits for the current quarter and the two before it.

Before you do anything else, use the IRS's free Offer in Compromise Pre-Qualifier Tool. It's not required, but it takes just a few minutes and gives you a realistic first read on whether this path makes sense for you before you spend time or money on paperwork.

Common Disqualifiers Specific to Small Business Owners

A few situations come up again and again for business-owning families:

Unfiled returns from your early years in the US. If nobody explained the filing requirements to you when you first arrived, it's easy to have gaps in your filing history without realizing it.

Missed quarterly estimated payments. If you're self-employed or run a small business, taxes aren't automatically withheld the way they are from a paycheck so missing a quarterly payment is a common and fixable issue.

Payroll tax shortfalls. If you employ family members or staff, falling behind on payroll tax deposits is treated seriously by the IRS and will block an OIC application until it's caught up.

None of these are permanent roadblocks. They just need to be fixed before you apply.

The Three Legal Grounds for an Accepted Offer

The IRS won't accept an offer just because you'd prefer to pay less. Your offer has to fall under one of three official reasons:

Ground | What it means | How common it is |

Doubt as to Collectibility | You likely can't pay the full amount, based on your income and assets | Most common roughly 90% of accepted offers |

Doubt as to Liability | You believe the IRS got the amount wrong, or you don't actually owe it | Less common, requires strong documentation |

Effective Tax Administration | You could technically pay in full, but doing so would cause real financial hardship or be unfair | Used in exceptional circumstances |

Doubt as to Collectibility is the one most people use. It's based on a calculation the IRS calls your Reasonable Collection Potential, which we'll walk through next.

Doubt as to Liability is different; it's not about whether you can pay, but whether the amount itself is correct. Maybe the IRS made a calculation error, or assessed tax on income that wasn't actually taxable. This requires a separate form (Form 656-L, not the standard Form 656) and solid evidence to back up your claim.

Effective Tax Administration covers situations where paying in full would technically be possible, but would create serious hardship for example, it would leave you unable to cover basic living expenses, or there's some other exceptional circumstances that makes full payment unfair.

How the IRS Calculates Your Offer Amount (Reasonable Collection Potential)

This is the part that decides whether your offer gets accepted or rejected, so it's worth understanding even in simple terms.

The IRS calculates something called your Reasonable Collection Potential (RCP) basically, their estimate of the most they could realistically collect from you. Your offer needs to be at or above this number, or it won't be accepted.

The formula looks like this:

RCP = Equity in your assets + (Monthly disposable income × 12 or 24 months)

A few pieces worth knowing:

"Equity in your assets" means things like the value of your home, car, or savings, minus what you still owe on them.

"Monthly disposable income" means what's left over after your allowable living expenses and the IRS uses standard amounts for things like food, clothing, housing, and transportation, called National Standards. If your actual spending falls within those standard amounts, the IRS generally won't question it or ask for receipts.

The 12 or 24 multiplier depends on whether you choose a lump-sum or periodic payment plan.

A simple example: Say someone has $5,000 in equity across a car and a small savings account, and after allowable expenses, has $300 left over each month. If they choose the lump-sum option (12-month multiplier), their RCP would be:

$5,000 + ($300 × 12) = $5,000 + $3,600 = $8,600

That $8,600 is roughly what their offer would need to be at or above for the IRS to consider accepting it even if their total tax debt is much higher, like $40,000. This is exactly how an OIC can meaningfully reduce what you owe.

Step-by-Step: How to Apply for an Offer in Compromise

Confirm you're eligible. File any missing tax returns first, and run the free Pre-Qualifier Tool to get a realistic sense of where you stand.

Gather your financial documents. You'll need recent bank statements, pay stubs, vehicle and property values, and if you're self-employed or run a business your business financial records too.

Complete the required forms. Fill out Form 656 (this is the actual offer) along with Form 433-A (OIC) if you're an individual, or Form 433-B (OIC) if you're applying for a business.

Calculate your offer amount based on your RCP. Be realistic here. Offering an amount that's too low compared to your actual RCP is the single most common reason offers get rejected.

Choose how you'll pay:

Lump sum: Pay 20% of your offer upfront with your application, then the rest in five or fewer payments if accepted.

Periodic payment: Submit your first payment with your application, then continue paying monthly while the IRS reviews your offer.

Pay the $205 application fee, unless you qualify for a waiver. If your income falls under the IRS's Low-Income Certification thresholds (based on your family size and where you live), both the fee and the upfront payment are waived.

Submit your application either by mail to the address listed on Form 656-B, or online through your IRS Individual Online Account.

Respond quickly if the IRS asks for more information. If they request additional documents, the clock is on you, not them slow responses mean slow processing.

What Happens After You Submit

Once your offer is in the system, a few things happen:

The IRS generally pauses other collection activity while they review your offer, though they may still file a Notice of Federal Tax Lien.

Any payments you make during the review period are non-refundable and get applied toward your tax debt either way.

Processing usually takes 6 to 12 months or more, depending on how complex your case is. If the IRS hasn't made a decision within two years, your offer is automatically accepted.

If you already have an installment agreement, you don't need to keep paying it while your OIC is under review.

How to Improve Your Chances of IRS Acceptance

Be accurate, not optimistic. Don't understate your assets or overstate your hardship. A mismatched RCP calculation is the number one reason offers get turned down.

Stay current while your offer is pending. Keep filing and paying on time during the review period, falling behind now can cause your offer to be rejected outright.

Disclose everything, including overseas accounts or property. If you have savings, property, or family financial ties back home, these need to be disclosed. This isn't the place for specific advice on foreign account reporting rules, talk to a tax professional about that separately but hiding assets, intentionally or not, can sink an otherwise strong offer.

Vet anyone you hire carefully. Look for a licensed CPA, Enrolled Agent, or tax attorney, and be wary of anyone who guarantees results before reviewing your actual financial details.

Keep records of everything. Save copies of every form, every document you send, and proof of mailing or submission.

What Happens If Your Offer Is Rejected?

A rejection isn't the end of the road.

You can appeal using Form 13711 within 30 days of receiving your rejection letter.

Fast Track Mediation may be available to resolve a specific disagreement, but only before a rejection letter is issued not after.

If an OIC genuinely isn't the right fit, there are other paths: an installment agreement, Currently Not Collectible status, or a partial-pay installment agreement that combines elements of both.

An Offer in Compromise is just one tool inside a bigger IRS framework sometimes called "Fresh Start," designed to help people get back into good standing. If this particular door doesn't open, there's usually another one that will.

After Acceptance - Staying Compliant for 5 Years

Getting your offer accepted feels like a huge relief, and it is but there's one important condition attached: for the next five years, you need to file every return and pay every tax on time.

If you default during that window a late filing, a missed estimated payment, a new balance due the IRS can reinstate your full original tax debt, including all the interest and penalties that the OIC was supposed to eliminate.

A simple way to protect yourself: set calendar reminders for filing and payment deadlines, and consider working with a tax professional for at least the first year after acceptance, just to build the habit and avoid an accidental slip-up undoing everything you worked for.

Conclusion: Is an Offer in Compromise Right for You?

An Offer in Compromise can genuinely reduce what you owe the IRS but only when four things line up: you meet the basic eligibility requirements, you have a valid reason the IRS recognizes, your offer matches what they could realistically collect from you, and you're ready to commit to five years of clean tax compliance afterward.

This is a real, legitimate program but it's not automatic debt forgiveness, and it's not for everyone. The most reliable first step is the IRS's free Pre-Qualifier Tool, followed by a conversation with a licensed tax attorney who can look honestly at your numbers before you commit any time or money.

And if you come across an ad promising to "settle your tax debt for pennies on the dollar, guaranteed" slow down. The real process takes documentation, patience, and an honest look at your finances. Anyone offering you a shortcut around that is usually selling something other than help

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

What Is an IRS Offer in Compromise and How Does It Work?

12 min read

What Is The Difference Between Criminal Tax Penalties And Civil Tax Penalties?

11 min read

IRS Form 433: What You Need To Know

10 min read

Tax Evasion Vs Tax Fraud And The Statute Of Limitations

9 min read

What Is An IRS Substitute For Return(SFR)?

12 min read

IRS Currently Not Collectible Status: What Are The Pros And Cons?

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation