Should You Choose Debt Settlement Or Credit Counseling?

You worked hard to build a life in the United States. But somewhere between the credit card bills, the medical expenses, and maybe a student loan or two, the debt quietly piled up. And if you're like many South Asian families here, you may have kept it to yourself because in our communities, talking about money problems can feel shameful.

You may be wondering: Is there a way out that doesn't destroy everything I've built?

There is. Two of the most common paths are debt settlement and credit counseling and they work very differently. This article breaks both down in plain language, so you can walk away knowing exactly which one fits your situation.

So, should you choose debt settlement or credit counseling? Let's find out.

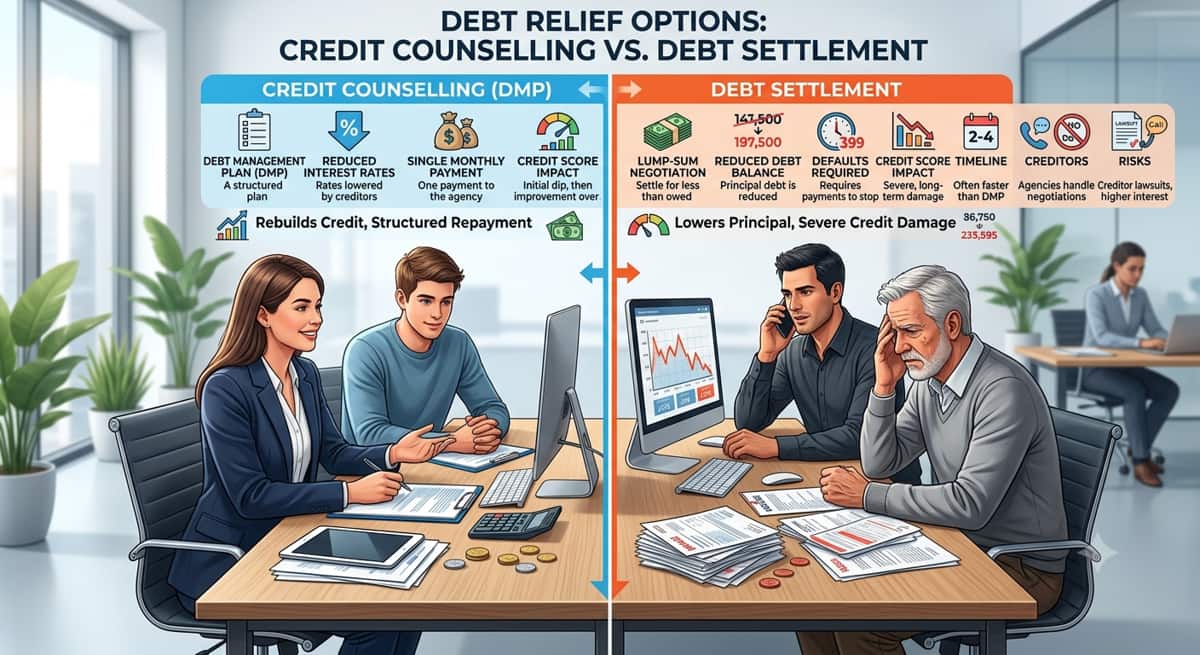

What Is Debt Settlement?

Debt settlement is when you negotiate with the people you owe money to your creditors and agree to pay them less than the full amount you owe. In return, they agree to consider the debt paid and close the account.

Here's how it typically works:

You stop making payments on the debt and start saving that money in a separate account instead.

Once enough has accumulated, a settlement company (or you directly) contacts your creditor to negotiate.

You offer a lump-sum payment often 40–60% of what you originally owed.

The creditor agrees, accepts the payment, and forgives the remaining balance.

This option is generally for people who are already behind on payments and carrying a large amount of unsecured debt things like credit card balances or medical bills.

Many South Asian families also carry debt across multiple cards or have co-signed loans with a spouse, parent, or sibling. That shared financial responsibility matters here, because settling one person's debt doesn't automatically protect the co-signer.

How Does Debt Settlement Affect Your Credit Score?

This is where it gets difficult. Debt settlement does real damage to your credit.

When a debt is settled, your credit report gets marked as "settled for less than the full amount" which tells future lenders you didn't pay what you originally agreed to. That mark can stay on your report for up to 7 years.

Most people see their credit score drop anywhere from 75 to 150+ points, sometimes more and that's on top of the damage already done by missed payments leading up to settlement.

There's also a tax angle worth knowing: if a creditor forgives more than $600 of your debt, the IRS may treat that forgiven amount as taxable income. You could receive a Form 1099-C at tax time, meaning you might owe taxes on money you never actually received in hand.

What Is Credit Counseling?

Credit counseling is a service offered by nonprofit agencies where a trained, certified counselor sits down with you either in person, by phone, or online reviews your full financial picture, and helps you build a realistic plan to get out of debt.

If your debt load qualifies, they may recommend a Debt Management Plan (DMP). Here's how it works:

You make one single monthly payment to the credit counseling agency.

The agency distributes that payment to each of your creditors on your behalf.

In many cases, your creditors agree to lower your interest rates, sometimes significantly, which means more of your payment goes toward the actual balance, not just interest charges.

The whole process typically takes 3 to 5 years to complete.

The most important thing to understand: with credit counseling, you are paying back everything you borrowed. There's no debt forgiveness here. What you're gaining is a more manageable structure and lower interest, not a reduction in what you owe.

For many South Asian families, this actually feels like the more honorable path. There's no defaulting, no broken agreements with creditors, just a structured, disciplined plan to clear the debt and move forward. That sense of order and responsibility resonates deeply with values many of us grew up with.

Does Credit Counseling Hurt Your Credit Score?

Not nearly as much as settlement does and in many cases, it actually helps over time.

Enrolling in a Debt Management Plan may leave a small note on your credit report, but it carries nowhere near the damage of a settlement or a string of missed payments. More importantly, because you're making consistent, on-time payments every month through the DMP, your credit score can gradually improve throughout the process.

And unlike debt settlement, you don't need to fall behind on your payments to qualify. You can enroll while still current on your accounts which protects your credit from the start.

Debt Settlement vs. Credit Counseling — At a Glance

Sometimes the clearest way to see the difference is side by side.

Factor | Debt Settlement | Credit Counseling (DMP) |

How it works | Negotiate to pay less than owed | Pay full balance at reduced interest |

Credit score impact | Significant negative impact | Minimal to moderate impact |

Time to complete | 2–4 years | 3–5 years |

Best for | Severe financial hardship | Stable income, high-interest debt |

Tax implications | Forgiven debt may be taxable | None |

Cost | 15–25% of enrolled debt in fees | ~$25–$50/month in agency fees |

Risk level | High — lawsuits, collector calls, credit damage | Low |

Credit report effect | Negative mark for up to 7 years | Far less damaging |

The bottom line is straightforward: debt settlement costs less in total repayment but comes with serious risks: damaged credit, potential tax bills, and the possibility of being sued by a creditor. Credit counseling takes longer and requires paying back the full amount, but it's a much safer, more stable path that protects your financial reputation along the way.

If you're trying to decide between the two, the table above isn't just a comparison, it's a map of what each road actually looks like before you start walking it.

When Debt Settlement Makes Sense — And When It Doesn't

Debt settlement isn't for everyone. Used in the right situation, it can offer genuine relief. Used in the wrong one, it can make things significantly worse.

It may be a reasonable option if:

You owe $10,000 or more in unsecured debt credit cards, medical bills, personal loans

You are already behind on payments or have accounts in collections

You are facing a creditor lawsuit and need to negotiate quickly

You are in genuine financial hardship job loss, medical crisis, or a major life disruption with no realistic way to repay the full amount

It's probably not the right fit if:

You have a steady income and your main frustration is high interest rates

Someone co-signed a loan with you a parent, spouse, or sibling because settlement won't protect them from collections

You're planning to apply for a mortgage, car loan, or rental in the next few years, since the credit damage will follow you

One thing many South Asian families don't initially mention and really should be is money sent home regularly as remittances, shared business ownership with family members, or financial obligations abroad. These factors can affect what options are realistically available to you, and a good counselor needs the full picture to give you honest advice.

No two financial situations are exactly alike. What worked for a neighbor or a cousin may not be right for you. Before making any decision, speaking with a certified financial counselor even just for a free initial consultation can save you from a costly mistake.

When Credit Counseling Is the Better Path

If you still have a regular income but feel like you're barely keeping up making minimum payments every month, watching the interest pile up, never actually getting ahead, credit counseling was essentially built for that situation.

This option tends to work best when:

You have a steady paycheck but your credit card interest rates are eating you alive

You want to protect your credit score because you're planning something important buying a home, sponsoring a family member's visa, or co-signing a loan for your child's education

You want one manageable monthly payment instead of juggling five different due dates and balances

You're current on payments but feel like the debt will never actually end

How to find a legitimate credit counseling agency:

Not all agencies are trustworthy and some are outright predatory. Look for agencies that are members of the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). You can also use the Consumer Financial Protection Bureau (CFPB)'s online counselor directory to find vetted, approved agencies in your state.

If you're unsure about an agency, check them with your state attorney general's office before sharing any financial information.

A note specifically for South Asian families: Language should never be a barrier when it comes to something this important. Some nonprofit credit unions and community organizations serving South Asian-American communities offer financial counseling in Hindi, Urdu, Bengali, Tamil, and other languages. It's worth searching locally or asking an agency directly whether they have bilingual counselors available because understanding every detail of your plan matters.

Beware of Debt Relief Scams Targeting Immigrant Communities

Here's something nobody warns you about enough: the debt relief industry has a serious scam problem and immigrant communities, including South Asian Americans, are frequently targeted.

Predatory companies know that people in financial distress are desperate for a way out. They use that desperation against you.

Watch out for these warning signs:

They guarantee they can settle or erase your debt no legitimate company can promise this

They demand upfront fees before doing anything for you this is actually illegal under FTC rules for debt relief companies

They pressure you to immediately stop all contact with your creditors without explaining the full consequences

They promise to "erase" or "wipe out" your debt completely and quickly

They are vague about their fees, their process, or their credentials

If something feels off, trust that feeling.

You can report suspicious debt relief companies or file a complaint through the Consumer Financial Protection Bureau (CFPB) , or through the Federal Trade Commission (FTC). Your state attorney general's office is also a powerful resource; many have dedicated consumer protection divisions that handle exactly these cases.

No legitimate counselor will ever make you feel rushed, pressured, or ashamed. If one does, walk away.

How to Decide: A Simple 3-Step Framework

If you're still not sure which path is right for you, work through these three steps before making any decisions.

Step 1: Be honest about your hardship level

Ask yourself: Are you already missing payments and getting calls from collectors? Or are you still current but drowning in interest charges with no end in sight? If you're already behind and the debt feels completely unmanageable, settlement may be worth exploring. If you're struggling but still holding on, credit counseling is likely the safer starting point.

Step 2: Add up your total unsecured debt

If your unsecured debt credit cards, medical bills, personal loans are under $5,000, you may be able to tackle it yourself with a structured payoff plan. If it's over $10,000 and you genuinely have no way to repay the full amount, debt settlement becomes more relevant. If the total feels manageable but the interest rates are the real problem, credit counseling is likely your best fit.

Step 3: Talk to a certified nonprofit credit counselor - for free

Before you sign anything or pay anyone, get a free initial consultation with a nonprofit credit counselor. This costs you nothing. They'll review your full financial picture, explain your options honestly, and tell you what makes the most sense for your specific situation without pressure and without a sales pitch.

You don't have to figure this out alone. One conversation can bring a lot of clarity.

The Right Answer Depends on Your Situation

There is no single correct answer here, only the answer that fits your life right now.

Debt settlement can reduce what you owe, but it comes at a real cost to your credit and carries genuine risks along the way. Credit counseling takes longer and requires repaying everything, but it's a steadier, safer road that keeps your financial standing intact.

What matters most is that you make this decision with clear information, not out of panic, and not based on a promise that sounds too good to be true.

Taking the first step doesn't have to be complicated. A free consultation with a nonprofit credit counselor costs you nothing and can give you a clear picture of exactly where you stand and what your real options are.

And if you've been putting this off because it feels embarrassing or overwhelming you're not alone. Every year, thousands of South Asian families across the U.S. face this exact situation and find their way through it. Asking for help isn't a sign that you failed. It's a sign that you're ready to take control.

Speak with a certified nonprofit credit counselor today many offer free consultations and bilingual support.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Bhupinder Bajwa

.

Related Articles

How Interest Rates Affect Debt

13 min read

How To Pay Off Debt Fast With Low Income

11 min read

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Everything You Need To Know About Consolidating Credit Card Debt

12 min read

Do Debt Relief Programs Work?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation