Secured Loans And The Option Of Debt Settlement

Moving to the United States often brings new opportunities, but it also introduces a financial system that can feel complicated and overwhelming. For many South Asian families, there is a deep-rooted cultural pride in building a stable future often centered around purchasing a home or owning a reliable vehicle. In our community, assets like these aren’t just "things"; they are symbols of hard work and security for our children and extended family.

However, when life takes an unexpected turn whether through job loss, health issues, or rising living costs, that sense of security can feel threatened by the weight of debt. You might be struggling to keep up with monthly payments and wondering if there is a way to lower your burden without losing the assets you’ve worked so hard to secure.

Understanding the Difference: Secured vs. Unsecured Debt

When you are trying to manage your finances, it is easy to lump all your monthly bills into one category: "debt." However, in the United States, lenders treat different types of debt very differently. Knowing this distinction is vital because it changes how you should handle a financial crisis.

Generally, debt falls into two categories: secured and unsecured.

The Difference at a Glance

Feature | Secured Debt | Unsecured Debt |

What is it? | Loans backed by an asset. | Loans backed only by your promise to pay. |

Common Examples | Mortgage, auto loans. | Credit cards, personal loans, medical bills. |

What happens if you miss payments? | You risk losing the asset. | Your credit score drops; lenders may sue. |

Can you "settle" it? | Generally, no. | Yes, in many cases. |

Secured Debt: The Role of Collateral

A secured loan is tied to a specific piece of property you own, which the bank calls collateral. Because the loan is attached to this asset, the lender has a legal claim to it known as a lien until you have paid back everything you borrowed.

If you stop making payments on a secured loan, the consequences are immediate and direct. For a car loan, the lender can take the vehicle back through a process called repossession. If you fall behind on a mortgage, the bank can begin foreclosure, which eventually leads to losing your home. Because the bank has a legal right to take back your collateral to cover the debt, you cannot simply negotiate to pay them back "less" than what you owe while keeping the item. They have very little incentive to accept a settlement because they already have the right to take the property.

Unsecured Debt: Your Promise to Pay

Unsecured debt, such as credit cards or personal loans, isn't tied to a specific item. If you cannot pay these debts, the bank cannot just show up and take your car or your house immediately. Instead, they will report the missed payments to credit bureaus, damaging your credit score. Eventually, they might send your account to a collections agency or sue you for the money.

Because there is no "asset" for them to easily take back, lenders are sometimes willing to negotiate this is what we call "debt settlement." They might agree to take a smaller, lump-sum payment just to resolve the matter and move on.

Never confuse the two. If you are struggling, always prioritize your secured debts first. Losing a home or a car has a much larger impact on your family’s daily life than a temporary hit to your credit score from an unpaid credit card.

As we look at these different types of debt, are you currently finding it more difficult to keep up with your home or vehicle payments, or is your main concern related to credit cards and personal loans?

Can You Settle Secured Loans?

The short answer is no: traditional debt settlement is designed for unsecured debt, not for loans where you have put up an asset as collateral. If a company tells you they can "settle" your mortgage or your car loan for a fraction of the cost, you should be extremely cautious.

Why Secured Loans Are Different

When you sign a contract for a mortgage or an auto loan, you are agreeing to specific terms that give the lender a legal interest in that property. Unlike a credit card where the bank just has your promise to pay, a secured lender has a "safety net."

If you stop paying a credit card, the bank has to go through a long, expensive legal process to try and get their money. Often, they decide it is cheaper to accept a "settlement" a smaller amount than to keep chasing you.

However, with a house or a car, the bank already has a clear legal path to get their money back: they take the asset. They don't need to negotiate or settle because they already have the right to sell your home or car to recover their losses.

The Consequences of Stopping Payments

It is a common myth that you can stop paying a secured loan to "force" the bank to negotiate a better deal. In reality, stopping payments on these loans is very risky:

For your home: If you miss mortgage payments, you will quickly head toward the foreclosure process. This is a public legal action that can lead to you and your family being evicted from your home.

For your car: Missing payments on a vehicle loan can lead to repossession, often with very little notice. Waking up to find your car gone can be a sudden, stressful, and expensive shock.

Because your family’s stability relies on these assets, treating a secured loan like a credit card debt is dangerous. If you are struggling with these payments, do not stop paying them in hopes of a settlement. Instead, you need to reach out to your lender to discuss official programs like "loan modifications or forbearance," which are specifically designed to help people keep their homes and cars while working through temporary financial hardship.

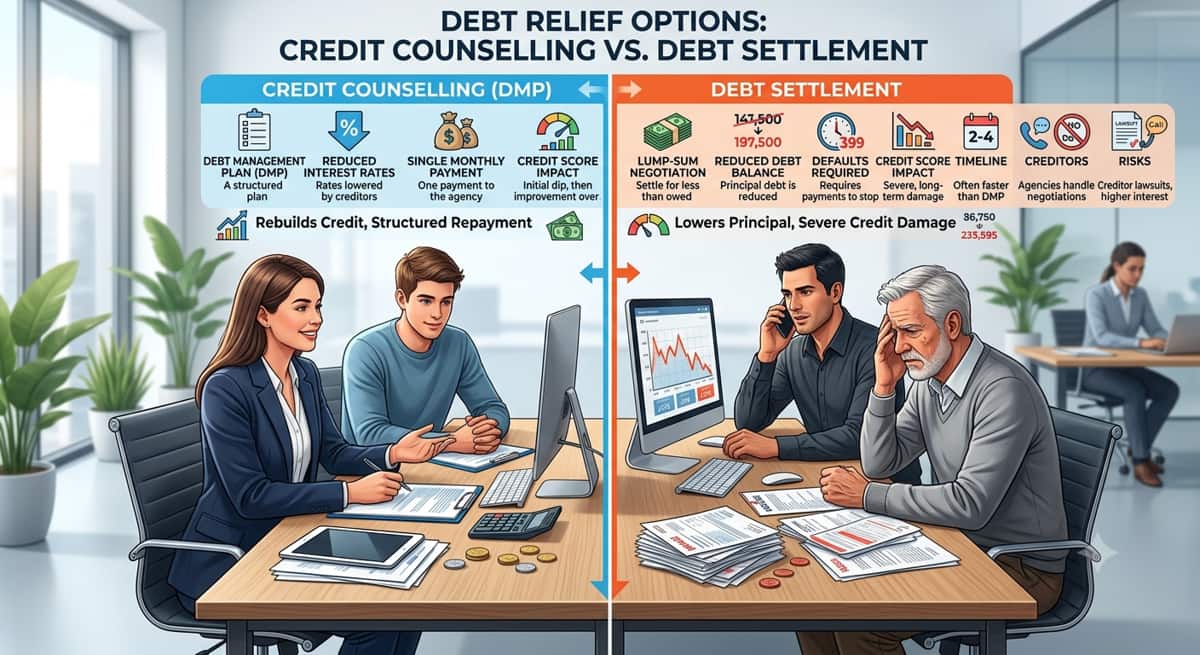

What is Debt Settlement and How Does it Actually Work?

Debt settlement is a process where you or a company you hire negotiate with your creditors to pay them less than what you actually owe to "settle" the debt for good. It is essentially a way to get a fresh start when you realize you can no longer keep up with your monthly payments. While it sounds like a perfect solution, it is a complex process that comes with real risks that you should weigh carefully.

How the Process Works

Whether you choose to handle this yourself or hire a professional company like Ooraa, the general steps look like this:

Consultation: You assess your total debt and decide if you have enough money to offer a lump-sum payment. You stop paying the creditors directly, which is what allows you to start saving that money for a future settlement offer.

Building a Dedicated Account: Because you have stopped paying your monthly bills, you must place that money into a savings account. You continue to build this fund until there is enough to make a meaningful offer to the creditor.

Negotiation: You (or your representative) contact the creditor to explain your financial hardship. You propose paying a lump sum usually 40% to 60% of the total balance in exchange for them marking the account "settled" or "paid in full."

Agreement and Payment: If the creditor accepts, you pay the agreed amount from your dedicated account. The remaining debt is then forgiven.

Should You Do It Yourself or Hire a Company?

You have two choices: doing it yourself or paying a company to do it for you.

The DIY Approach: You pay no fees, you have complete control over your money, and you can communicate directly with your creditors. However, it takes time, emotional stamina, and the ability to handle tough conversations with collectors.

Hiring a Company: They have experience negotiating and know what to say to creditors. However, you will have to pay them high fees, and you lose control over your money. Warning: Be very careful with companies that ask for large upfront fees; many are scams. Always look for reputable, non-profit credit counseling organizations first.

The Hidden Risks

Debt settlement is not a "free pass." Before you start, you must be aware of the trade-offs:

Credit Score Impact: Because you must stop making your monthly payments to save up for a settlement offer, your credit score will drop significantly. Late payments stay on your report for seven years.

Tax Liabilities: In the eyes of the IRS, forgiven debt is often considered "income." If you settle $5,000 of debt, you may receive a tax form for that amount and be required to pay income tax on it.

Collection Harassment: Once you stop paying, creditors and collection agencies will likely call you frequently. You must be prepared to handle these calls firmly and calmly.

No Guarantees: Creditors are not required to accept your offer. You could go months without paying, damage your credit, and then have the creditor refuse to settle, leaving you in a worse position than when you started.

Considering how much time and emotional energy is required for this process, would you feel more comfortable navigating these negotiations on your own, or would you prefer to explore free, non-profit resources that can guide you through the steps?

Cultural Considerations for South Asian Families in the USA

For many South Asian families, the journey to the United States is paved with immense sacrifice. There is a deep, honorable tradition of working hard to provide for our children, support extended family back home, and establish a legacy. In this context, financial stability, especially homeownership, is seen as a sign of success and a way to ensure the family's future.

Because of this, falling into debt can feel like a heavy, personal burden that goes beyond just numbers on a bank statement. Many in our community feel a strong sense of social stigma around financial struggles. There is often an unspoken pressure to keep up appearances, making it difficult to talk about money problems even with close friends or family. This silence can make a stressful situation feel isolating, as if you are the only one struggling to keep your head above water.

It is important to remember that debt is not a reflection of your character, your worth, or your ability as a provider. It is simply a financial hurdle, a temporary obstacle that can happen to anyone, especially in a complex system like the U.S. credit landscape.

Redefining Your Perspective

When you frame debt as a manageable problem rather than a personal failure, you gain the clarity needed to fix it. Your credit score is not just a digit; it is a tool for your family’s future. It is what will help you finance your children’s higher education, secure a small business loan, or navigate future life events. Protecting that tool is a sign of long-term planning, not weakness.

The Power of Seeking Help

There is incredible strength in reaching out. Many South Asian families hesitate to seek professional financial counseling because they fear judgment. However, non-profit credit counselors are trained to be objective and compassionate. They have seen every type of situation and are there to offer a roadmap, not to critique your past decisions. Whether you are dealing with overwhelming credit card bills or trying to understand how to keep your home, speaking with a neutral, qualified expert can turn a source of silent shame into a clear, actionable plan.

Alternatives to Debt Settlement for Secured Loans

If you are struggling to keep up with your mortgage or car payments, the worst thing you can do is wait until you have already missed multiple payments. Many people mistakenly think that if they can't pay, they should stop communicating with the lender. In reality, the best strategy is to be proactive. Lenders generally prefer to help you stay in your home or keep your car rather than going through the expensive and time-consuming process of taking them back.

If you are facing a temporary hardship, here are several constructive ways to protect your assets:

Loan Modification: This is a formal agreement where the lender changes the terms of your original loan to make the monthly payments more affordable. They might lower your interest rate, extend the length of the loan to reduce monthly costs, or temporarily pause a portion of the payments. This allows you to keep your property while adjusting to your new financial reality.

Forbearance: If you are dealing with a short-term crisis such as a sudden job loss or a family medical emergency you can ask your lender for a forbearance. This is a temporary pause or reduction in your payments for a set period. It gives you "breathing room" to get back on your feet without the immediate threat of foreclosure or repossession.

Refinancing: If your credit score is still in decent shape, you may be able to refinance your loan. This involves taking out a new loan with better terms to pay off the old one. The goal is to secure a lower monthly payment, which can take the pressure off your monthly budget.

Non-Profit Credit Counseling: Sometimes, the issue is not just one loan, but your entire budget. Non-profit credit counselors can help you look at your total income and expenses. They can often work with you to create a "Debt Management Plan" (DMP). While they cannot change the terms of your mortgage, they can help you manage your other debts so that you have more money available to prioritize your secured payments.

Why Working With Your Lender Matters

When you approach your lender early, you are not asking for a favor you are proposing a solution. Lenders are businesses; they want to receive their money, and they know that you are a better bet as a paying customer than the uncertainty of an empty house or a used car on a lot.

When you call them, be honest about your situation. Have your budget ready and be clear about how your financial circumstances have changed. By acting as a partner in solving the problem rather than an opponent, you demonstrate responsibility and show that you are committed to keeping your commitments. This approach keeps your assets safe and helps you avoid the severe, long-term damage that comes with defaulting on a loan.

Have you reached out to your bank to discuss any of these options yet, or does the idea of initiating that conversation feel like the biggest hurdle right now?

Protecting Your Credit Health During Financial Hardship

Even when you are navigating a difficult financial season, your credit score remains an important tool for your family’s future. While it may take a hit if you fall behind on payments, there are proactive steps you can take to minimize the damage and keep your financial options open for when things improve.

Understanding What Moves the Needle

Your credit score is built on several factors, but two stand out as the most critical during times of stress:

Payment History: This is the most important factor. Even if you cannot pay the full amount due on your credit cards, try your best to pay at least the "minimum payment" by the due date. This shows lenders that you are still committed to your obligations, even if you are struggling.

Credit Utilization: This refers to how much of your total credit limit you are currently using. If your credit cards are maxed out, your score will drop. If you have to carry a balance, try to keep it below 30% of your total limit if possible. If you are struggling to keep balances low, prioritize paying down the cards that are closest to their limits.

The Power of Proactive Communication

One of the most common mistakes is ignoring bills when money is tight. Instead, contact your creditors before a payment is late. Ask them if they have a "hardship program" available. Many lenders have internal systems in place to lower interest rates temporarily or waive late fees if you are willing to communicate your situation honestly.

Lastly, be mindful of your debt-to-income ratio, the percentage of your monthly income that goes toward paying debts. While this doesn't directly appear on your credit report, it is the key number lenders look at when you apply for future loans, such as a mortgage or business credit. Keeping this ratio in check, even while you are working through debt, will make you a much stronger candidate for credit in the future.

How to Choose a Legitimate Debt Relief Partner

When you are already feeling the weight of debt, the last thing you need is to be taken advantage of by someone promising a "quick fix." Unfortunately, the debt relief industry has its share of bad actors. Knowing how to tell the difference between a helpful partner and a predatory scammer is one of the most important steps you can take to protect your family's financial future.

Red Flags to Watch For

If you encounter any of the following, walk away immediately:

Promises of "Guaranteed" Results: No ethical organization can guarantee that they will eliminate your debt by a specific amount or boost your credit score overnight. If it sounds too good to be true, it almost certainly is.

Demands for Upfront Fees: Be extremely wary of companies that ask for large payments before they have actually helped you settle or manage a single debt. Legitimate agencies are transparent about their fees and typically charge only after they have successfully performed a service for you.

Pressure Tactics: Scammers often use high-pressure sales tactics, telling you that their offer is "time-sensitive" or that you must act now to avoid an imminent disaster. A professional organization will always give you time to review documents and make a decision without fear.

What to Look For

A legitimate debt relief partner should prioritize your financial education and well-being over a quick profit. Look for:

Non-Profit Status: Reputable organizations are often non-profits that focus on helping you create a realistic budget rather than just pushing a specific product.

Transparency: They should provide clear, written contracts that explain exactly what services you are receiving and what the total costs will be, in plain language.

By choosing a partner that values transparency, education, and your long-term success, you can move forward with confidence, knowing you are in safe, professional hands.

Your Path Forward

Dealing with debt can feel like a heavy cloud, but remember: your current situation is just a single chapter in your journey, not the final destination. By learning the difference between your options and understanding how the U.S. financial system works, you have already taken a powerful first step toward reclaiming your peace of mind.

You do not have to carry this burden alone or make these high-stakes decisions in secret. Real, non-judgmental support is available to guide your family toward safety.

Take Action Today: Reach out to a certified, non-profit credit counselor for a free, confidential consultation. They will look at your unique situation and help you build a clear, step-by-step plan to protect your assets and build a stable, stress-free future.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Ooraa Team

Our team of certified debt consultants has over 10 years of experience helping families become debt-free. We specialize in debt settlement strategies and financial education.

Related Articles

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Everything You Need To Know About Consolidating Credit Card Debt

12 min read

Credit Card Debt Forgiveness For Disabled: Do You Qualify?

11 min read

Do Debt Relief Programs Work?

11 min read

Does Debt Affect Your Credit Score?

11 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation