Why Your Paycheck Disappears So Fast in 2026 — And How to Break the Debt Cycle

Your paycheck lands. For a few minutes, things feel normal. Then rent, credit cards, loan payments, subscriptions, groceries, gas, and minimum payments hit — and suddenly, your account feels empty again.

In 2026, this feeling is more common than most people realize. U.S. household debt reached $18.8 trillion in Q1 2026, while credit card balances remained around $1.25 trillion, according to the New York Fed. A Bankrate survey found that 47% of credit cardholders are currently carrying credit card debt — and 61% of those people have been in debt for at least a year.

If your paycheck disappears every month, you are not alone. And you are not failing. There may be structural reasons your money is moving out faster than it comes in.

Why Your Paycheck Feels Smaller in 2026

The cost of everyday life has shifted significantly. Even people with stable incomes are finding that their paycheck is already spoken for before the month starts. Here is where most of it goes:

• Rent and housing costs — still near historic highs in most cities

• Groceries and household essentials — consumer prices remain elevated

• Utility and energy bills

• Gas and transportation

• Subscriptions and autopay charges — many people have more than they realize

• Insurance premiums — health, auto, and renter’s

• Credit card minimum payments

• Personal loan payments

• Medical bills

• Family obligations and caregiving costs

Your income may not be the only issue. The real problem may be that too much of your paycheck is already committed before you even get to use it.

The Minimum Payment Trap

Credit card minimum payments are designed to keep your account in good standing — not to help you get out of debt. When you only pay the minimum, most of that payment often goes toward interest, not toward reducing your actual balance.

Example: A $8,000 credit card balance at 22% APR on minimum payments only will reduce very slowly because interest keeps adding up each month. The same balance paid at $300 per month clears significantly faster and costs much less in total interest.

Minimum payment is not always a payoff plan. Sometimes it is just a pause button.

Why Credit Card Debt Is Draining Paychecks

Credit card debt is one of the biggest reasons people feel financially squeezed after payday. Total U.S. credit card balances sat around $1.252 trillion in Q1 2026. Bankrate reported the average credit card interest rate at 19.57%, while Forbes noted average APR on accounts carrying balances reached 21.52% as of early 2026.

When rates are that high, every monthly payment is fighting two battles: the existing balance you already owe, and the new interest added that month. That is why some people pay hundreds of dollars every month and still feel like the balance barely moves.

Signs You Are Stuck in a Debt Cycle

A debt cycle can be hard to see from the inside because it just feels like normal stress. Here are some signs that debt may be quietly controlling your monthly income:

• Your paycheck is mostly gone within a few days of payday

• You pay one credit card using another

• You use personal loans to cover credit card bills

• You only ever make minimum payments

• Your balances are not going down despite regular payments

• You avoid checking your bank account or statements

• Unknown phone numbers make you anxious

• You delay one bill to pay another

• You cannot save anything even after cutting expenses

• Every month seems to start with debt pressure already in place

If 3 or more of these feel familiar, it may be time to review your options. Visit your debt-options

Paycheck-to-Paycheck Living Is Not Always a Spending Problem

There is a common assumption that living paycheck to paycheck means someone is spending carelessly. That is often not true.

For many households, the issue is not discretionary spending — it is the weight of existing financial obligations. High-interest debt, unexpected medical expenses, job loss or reduced hours, emergency borrowing, family responsibilities, and years of rising living costs can push anyone into a tight spot.

PYMNTS and LendingClub reported that 43% of consumers at least occasionally revolve credit card balances, and that number rises to 65% among consumers who describe themselves as financially struggling. Credit has become a survival tool for many households — not just a convenience.

Being in a debt cycle does not mean you made bad decisions. It often means the system caught up with you before you could catch up with it.

How Debt Quietly Takes Control of Your Monthly Income

The debt cycle rarely has one dramatic cause. Most of the time, it is a combination of obligations stacking on top of each other every month:

• Credit card minimums — keeps accounts current but may not reduce balances meaningfully

• Personal loan payments — adds fixed pressure that does not flex when things get harder

• Late fees — makes the following month harder than it needs to be

• Interest charges — increases the real cost of purchases made months or years ago

• Collection accounts — creates ongoing urgency and may affect your credit

• Autopay bills — pulls money out before you can plan or redirect it

The problem is not always one big bill. Often, it is many small and medium payments hitting at the same time, leaving very little room to breathe.

How to Break the Debt Cycle

Breaking out of the debt cycle takes clarity before it takes action. Here are practical steps:

1. List every debt in one place. Include creditor name, balance, interest rate, minimum payment, due date, and account status. Seeing everything together is often the most clarifying step.

2. Separate needs, wants, and debt payments. This helps you understand how much of your income is going toward survival vs. paying off past obligations.

3. Identify high-interest debt first. Credit cards and payday loans tend to grow the fastest and usually need the most urgent attention.

4. Stop using new credit to pay old debt. This is one of the clearest signs a debt cycle is deepening. If you notice this pattern, it is worth reviewing your situation seriously.

5. Review your options before missing more payments. Options may include debt consolidation, debt settlement, credit counseling, hardship programs, or in severe cases, bankruptcy.

6. Speak with a qualified professional before deciding. Every situation is different. A structured conversation about your specific debt may open up options you did not know existed.

When Budgeting Alone May Not Be Enough

Budgeting is a useful tool when the main issue is spending patterns. But if your monthly debt payments are already consuming a large portion of your income, interest is growing faster than you can pay it down, or you are using new credit to cover old debt — a budget may not be enough to solve the underlying problem.

At that point, you may need to explore structured debt relief options. Cutting a streaming subscription will not make a meaningful difference if hundreds of dollars are going to minimum payments on high-interest credit cards every month.

Debt Relief Options You Can Explore

If your debt situation feels unmanageable, here is a general overview of options worth understanding:

Debt Consolidation — May help if you have good credit and want to combine multiple payments into one. You may still repay the full balance, so the interest rate on the new loan matters.

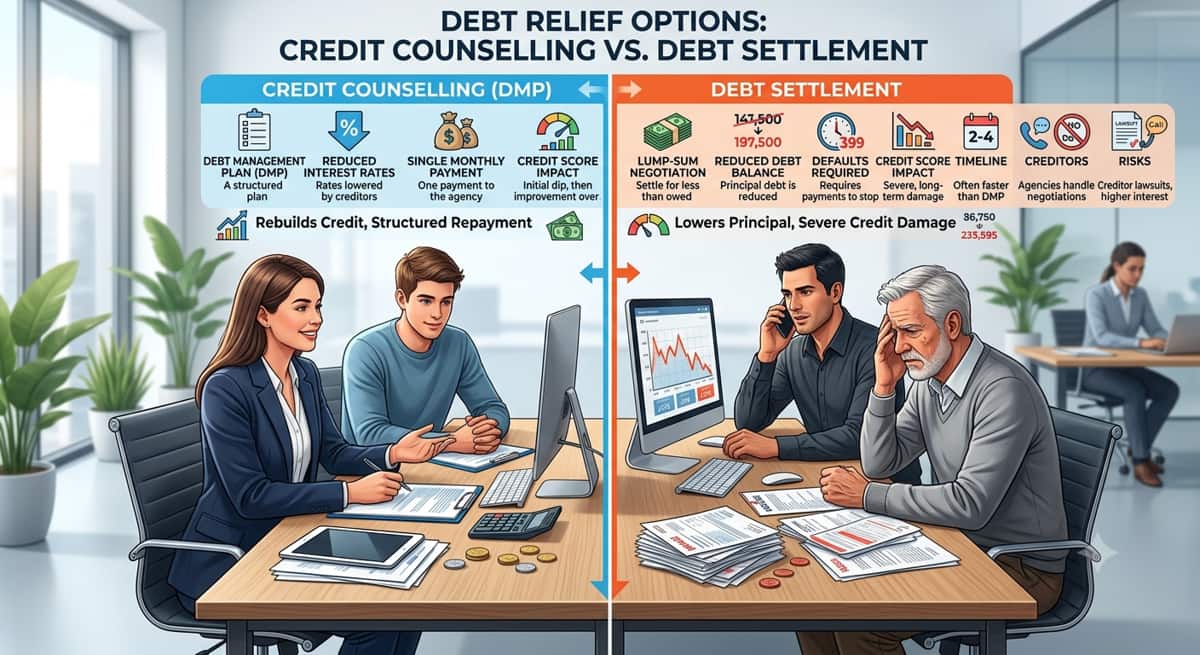

Debt Settlement — May be an option if you are facing hardship with unsecured debt like credit cards. It may affect your credit, and results are not guaranteed.

Credit Counseling — May help if you need structured repayment guidance and support, usually through a nonprofit repayment plan.

Bankruptcy — May be considered if debt is severe and other options may not be workable. Requires legal guidance and has significant credit impact.

Not sure which option fits your situation? See how OORAA works

Your Paycheck Is Not the Problem — The Debt Cycle May Be

If your paycheck disappears every month, it does not mean you failed. It may mean your debt structure is working against you. High-interest balances, minimum payments, late fees, and stacked obligations can quietly consume income even when someone is doing everything else right.

The first step is not shame. It is clarity. Understanding where your money is going — and what options may be available — is how most people begin to find a way forward.

Your first step is clarity, not shame. Explore your debt relief options at your debt-options

Frequently Asked Questions

Why does my paycheck disappear so fast?

Your paycheck may disappear quickly because of rent, utilities, groceries, subscriptions, loan payments, credit card minimums, interest charges, and automatic payments. If debt payments take up too much income, you may feel financially squeezed shortly after payday.

Why am I still broke even though I have a job?

Having income does not always mean financial flexibility. If much of your paycheck is already committed to old debt, interest, and fixed bills, you may still feel stuck — even with a steady income.

What is the minimum payment trap?

The minimum payment trap happens when you only pay the minimum amount due on credit cards. This can keep the account active, but interest continues building, making the balance harder to reduce over time.

How do I know if I am in a debt cycle?

You may be in a debt cycle if you rely on credit cards right after payday, pay one debt with another, only make minimum payments, delay bills, or feel like your balances never go down despite regular payments.

Can debt consolidation help if my paycheck disappears quickly?

Debt consolidation may help some people combine multiple debts into one payment, especially if they qualify for better terms. However, it may not be right for everyone — particularly if the new loan does not meaningfully reduce the monthly pressure or total interest paid.

When should I consider debt relief options?

You may want to review debt relief options if your unsecured debt feels unmanageable, you are falling behind, your balances are not reducing, or you are regularly using new credit to cover old payments.

Will debt relief hurt my credit?

Some debt relief options can affect your credit score. The impact depends on your current account status, payment history, chosen option, and how creditors report your accounts. Speaking with a qualified provider can help clarify what to expect.

How can OORAA help?

OORAA helps people understand their debt situation, explore possible debt relief options, and connect with third-party providers who can explain available next steps. Results are not guaranteed and will vary by individual situation.

This blog is for educational purposes only. OORAA does not provide legal or financial advice. Results are not guaranteed. Some debt relief options may affect your credit. Please consult a qualified professional before making decisions about your debt.

Ready to Get Started?

Get a free consultation with a certified debt consultant to see if debt settlement is right for you.

Get Free ConsultationAbout the Author

Ooraa Team

Our team of certified debt consultants has over 10 years of experience helping families become debt-free. We specialize in debt settlement strategies and financial education.

Related Articles

How Can You Settle Credit Card Debt Without Bankruptcy?

12 min read

Credit Counselling vs. Debt Settlement: Which One Is Right for You?

12 min read

Do Debt Relief Programs Work?

11 min read

Debt Settlement- The Best Way To Avoid A Lawsuit

10 min read

Things To Keep In Mind If You are Looking To Consolidate Debt

9 min read

Veteran Debt Relief | Effective Military Debt Solutions

12 min read

Get Your Free Consultation

Speak with a certified debt consultant to explore your options.

Start NowNo obligation • Free consultation